UK stocks make up a lot of my portfolio. And that’s why I’m not listening to the old stock market wisdom of selling in May and going away.

There is some truth to the thought that share prices do better in some months than others. But there are far more important things to think about.

Why May?

The summer can be a relatively quiet time for the stock market. One reason for the selling ideas is that people are less interested in share prices when they’re on holiday.

In a year like this one, though, I’m not convinced that makes much difference. There’s a lot more going on that’s moving share prices around.

The most obvious example is the conflict in Iran. I’m expecting any major development there to have a big impact, regardless of people’s travel plans.

That’s unique to this year. But I think there’s nearly always something going on that’s worth paying attention to between May and October.

I think the fundamentals of what I own give me a better guide about what to do than the calendar. And there’s a big reason I’m not selling my UK stocks.

Valuations

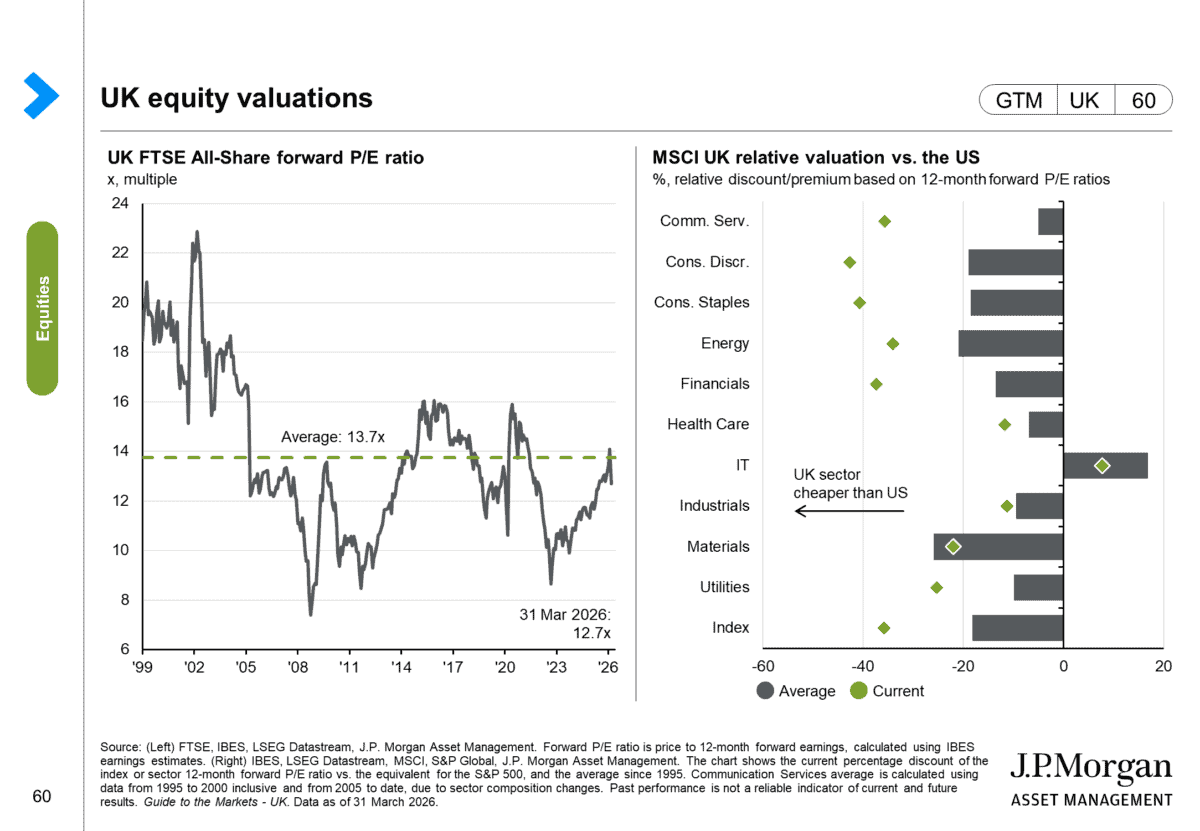

Put simply, UK stocks are cheap at the moment. The FTSE 100 is currently trading at an unusually low forward price-to-earnings (P/E) ratio.

On top of this, UK equities are also cheaper than their US counterparts. This isn’t unusual, but the extent of the current difference is.

Source: JP Morgan Guide to the UK Markets Q2 2026

Comparing price-to-earnings (P/E) ratios doesn’t account for differences between individual businesses. But the general picture is pretty clear.

The only sector where FTSE 100 shares are trading above their average discount is materials. And I don’t own any stocks in that sector.

Given this, why would I want to sell my UK stocks? They’re unusually cheap and the point of investing isn’t to give someone else a bargain.

An example

One FTSE 100 stock in my portfolio is Rentokil Initial (LSE:RTO). It’s up 42.66% in the last 12 months, but I’ve no intention of selling.

It’s a great example of a UK stock that’s trading at a relative discount. Its nearest US competitor is Rollins – a member of the S&P 500.

In 2025, the FTSE 100 company recorded higher sales and generated higher free cash flows. But the firm’s market value is around 37% lower.

| Rentokil | Rollins | |

|---|---|---|

| Market cap | $16.84bn | $26.84bn |

| Revenue (12 months) | $6.9bn | $3.85bn |

| Free cash flow (12 months) | $764m | $621m |

Now, Rentokil has much higher long-term debt – $4.1bn compared to $487m – after a big acquisition in 2022. And this is a genuine risk for investors.

Even adding the debt on top of the market cap, however, Rentokil is still significantly cheaper than Rollins. I think that’s the UK discount in action.

Why I’m not selling

Could the shares fall in the next few months? Absolutely – a lot might depend on things that have nothing intrinsically to do with the business.

Over the long term, though, I’m much more positive. I expect demand to be strong and I think the firm has a strong position in a growing market.

Right now, there are other opportunities that I find even more compelling. But I’m not even thinking of selling my Rentokil shares in May.