A Self-Invested Personal Pension (SIPP) is a flexible investment vehicle for those wanting to boost their retirement income. And with many experts suggesting that the State Pension isn’t sufficient to provide for a comfortable old age, it’s probably a good idea for most of us to start investing more.

Indeed, those currently (3 May) receiving the full UK State Pension of £12,548 might look abroad with envy. Many European countries pay more. The most generous is Iceland where pensioners can receive up to £30,251 per annum!

However, with its attractive tax advantages I think a SIPP could help those who don’t want to move overseas. Let me explain.

Please note that tax treatment depends on the individual circumstances of each client and may be subject to change in future. The content in this article is provided for information purposes only. It is not intended to be, neither does it constitute, any form of tax advice. Readers are responsible for carrying out their own due diligence and for obtaining professional advice before making any investment decisions.

How do the numbers stack up?

One popular retirement strategy is to invest regularly in a SIPP and buy some growth shares. In theory, these are more likely to beat the returns of the wider market.

The average annual return of the FTSE 100 from 2006-2026 was 6.4%. This assumes all dividends were reinvested buying more shares.

However, by adopting a successful stock-picking strategy, I believe it’s possible to do better. Of course, with the benefit of hindsight it’s easy to find stocks that have out-performed the Footsie over various periods. But I don’t know anyone clever enough to always pick the best.

Instead, to be more realistic, let’s look at the stock ranked 50th in the league table of FTSE 100 performers over the past five years. How did it do?

Who?

Well, RELX (LSE:REL), the global provider of information-based analytics and decision tools, has delivered an average annual return of 8.9%. Again, this assumes all payouts were used to buy more shares.

Someone investing £425 a month in a SIPP returning 8.9% will see it grow to £468,617 after 25 years. If this is then used to buy a portfolio of dividend shares paying 6.6%, the average of the top 10 FTSE 100 yielders at the moment, it would produce an annual income of £30,928, a little more than Iceland’s full State Pension.

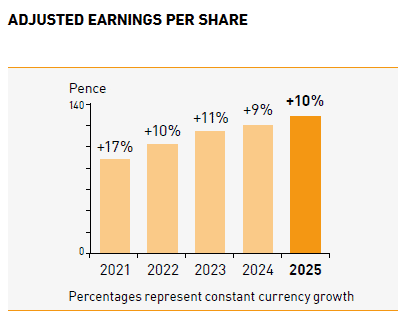

I think it’s fair to say that RELX isn’t a household name. But it’s delivered impressive earnings per share (EPS) growth in recent years.

Looking back over its 2021-2025 financial performance:

- Revenue’s increased 32%.

- EPS’s now 47% higher.

- Adjusted operating margin’s improved 4.3 percentage points.

However, its share price has taken a bit of a knock lately. There are fears that artificial intelligence (AI) could disrupt its business model, making it easier for cheaper alternatives to gain market share.

It also remains vulnerable to a cyber attack.

My view

But the group sees AI as an opportunity rather than a threat. The continued evolution of artificial intelligence is enabling us to add more value to our customers, as we embed additional functionality in our products, and to develop and launch products at a faster pace, while continuing to manage cost growth below revenue growth

And with its blue-chip customer base and huge global presence, it has enormous pricing power. Also, its shares are trading well below their five-year earnings multiple.

That’s why I reckon investors looking for a reliable performer to tuck away in a SIPP (and those not wanting to move to Iceland) could consider RELX as part of a diversified portfolio.