Greencoat UK Wind (LSE:UKW) has long been one of the FTSE 250‘s most popular dividend stocks. It’s easy to see why — reliable cash flows support a consistent stream of passive income for investors. Annual payouts have, in fact, risen every year but one since its shares hit the London stock market in 2013.

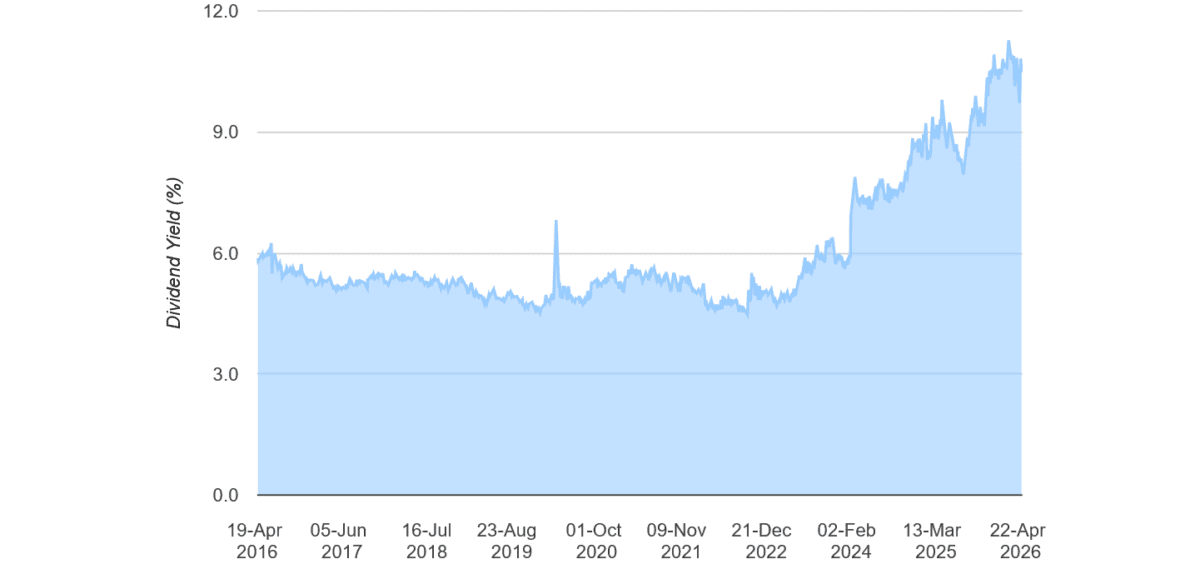

Yet that’s not the only reason it’s become a sought-after dividend share more recently. Greencoat’s share price has tumbled 25% over the past five years, which has in turn supercharged its dividend yield, as the chart below shows.

For 2026, the dividend yield is a mighty 10.9%, reflecting analyst expectations of further dividend growth. The yield marches to 11.1% for next year, too.

The thing is, are Greencoat shares likely to keep sliding? And does the possibility of more gigantic dividends make it a top stock to consider anyway?

What’s been happening?

There are critical questions to ask. The benefit of a sky-high dividend payment can be offset (if not totally eliminated by) a sinking share price that decimates total returns.

Greencoat’s price performance since late 2022 reflects a much tougher time for renewable energy stocks more broadly. Why? A backdrop of higher-than-normal interest rates has put pressure on net asset values, reducing the worth of its energy portfolio. Bank of England (BoE) rate hikes have increased the cost of Greencoat’s borrowing, hitting earnings and potentially derailing its expansion plans.

That’s not all. More recently, the firm’s been hit by changes to renewables obligation certificates (ROCs), which link revenues to inflation. The problem is these are now based on CPI rather than RPI, which tends to be lower.

Will these problems continue? It’s possible. Rising inflationary pressures mean fresh BoE rate rises could be around the corner. And given the highly regulated nature of the energy market, policy changes like amendments to ROCs are an ever-present danger.

So what now?

Does this make Greencoat a dividend stock to avoid, then? I suppose it depends on the timescale over which an investor plans to hold its shares. In the coming months, its share price could remain over pressure. But I’m expecting it to recovery strongly over the long term, making it worth consideration from patient investors.

Make no mistake: renewable energy has considerable investment potential as the world switches from fossil fuels. It’s not just environmental concerns that are sparking this sea change. Geopolitical considerations are also driving this trend, as the Iran war and its impact on oil prices demonstrates perfectly. Accordingly, demand for cleaner energy should continue rising exponentially.

I also like Greencoat because of its focus on UK assets. This is one of the most favourable places to produce green energy anywhere in the world thanks to supportive government policy. With defensive day-to-day operations and great growth possibilities, I expect it to remain a top stock for reliable dividend growth.

Greencoat UK shares don’t just offer those double-digit dividend yields. They trade on a rock-bottom price-to-earnings (P/E) ratio of 7.7 times, and at a 26% discount to their NAV per share. With this sort of value, I think dividend investors should keep this stock in mind.