For many investors, the ISA isn’t just a tax shelter. It’s the pot they hope will one day buy flexibility – fewer working hours, less reliance on pensions, or simply more control over how and when they earn.

Please note that tax treatment depends on the individual circumstances of each client and may be subject to change in future. The content in this article is provided for information purposes only. It is not intended to be, neither does it constitute, any form of tax advice. Readers are responsible for carrying out their own due diligence and for obtaining professional advice before making any investment decisions.

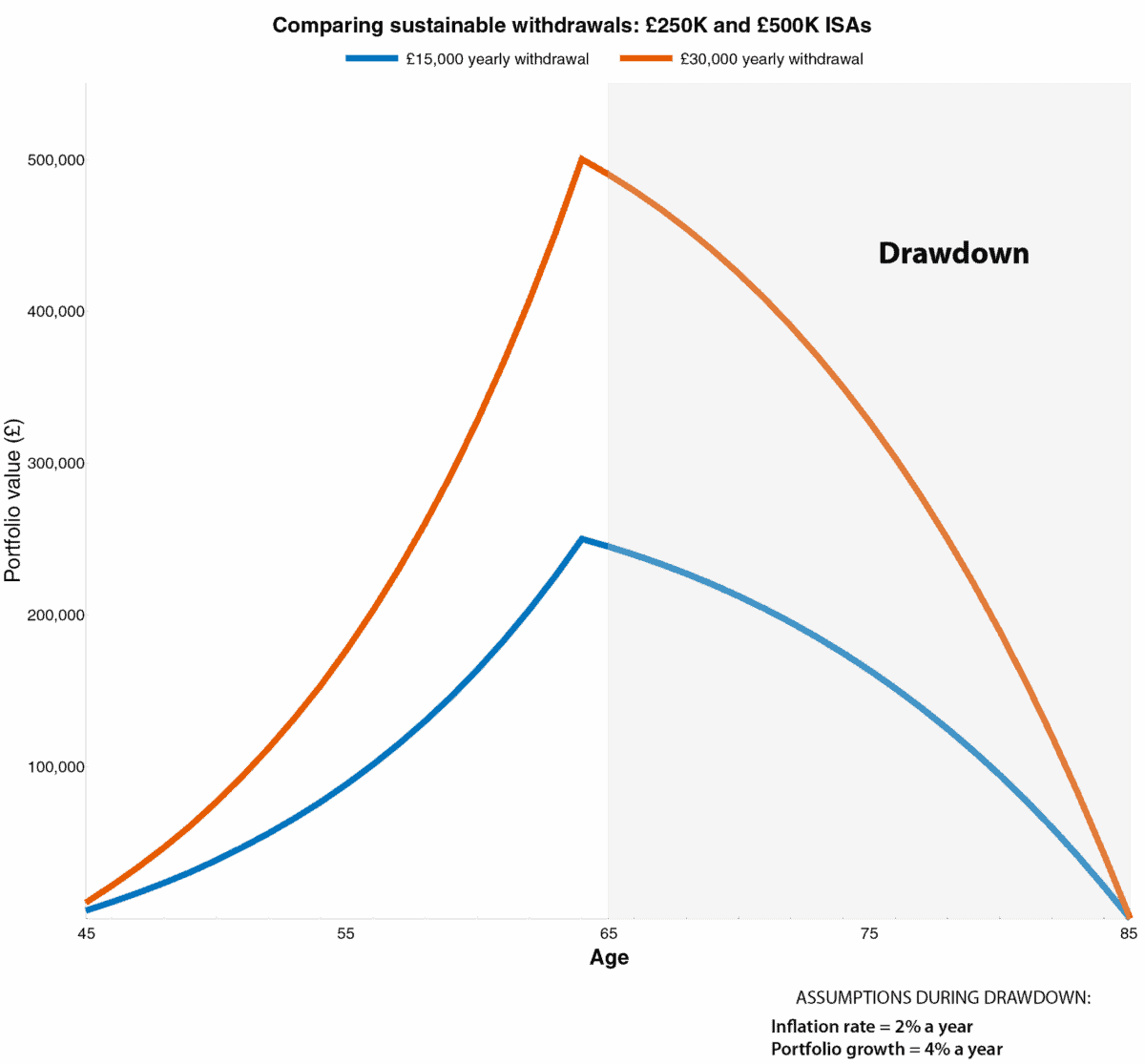

What this chart really shows

The chart below isn’t a retirement countdown. It’s a spending-power test. What matters is how much income an ISA can provide once it starts working for you.

With cautious assumptions, a £500,000 ISA could generate roughly £30,000 a year in passive income. On paper, this is simply double the income of a £250,000 ISA, but in practice, it can feel like a very different proposition.

Looking beyond the ‘line’

At £250,000, most investors are still locked into the line. The income helps, but it rarely reshapes life choices. Work continues to do the heavy lifting.

At £500,000, the line starts to bend. The income is no longer marginal. It can cover a large share of essential spending, introducing optionality well before full retirement. That might mean reducing hours, changing roles, taking breaks, or easing financial pressure even before withdrawals begin.

That’s why the chart matters less than it looks. It’s not a rigid plan to follow, but proof of concept – showing when an ISA stops being a supplement and starts providing genuine financial freedom.

Growth mindset

There are two realistic ways an investor reaches a £500,000 ISA. Either capital does more of the work, through growth-oriented investments. Or time does, by starting earlier and allowing compounding to do the heavy lifting.

If you’re relying on capital, the question becomes: which stocks can help your ISA grow steadily over the years? That’s where companies like Prudential (LSE: PRU) come into play – businesses with structural growth potential and a proven track record, positioned to support long-term ISA growth.

The Asian insurer isn’t a flashy tech growth story, but its opportunities are tangible. Investors are beginning to take notice, with the stock up 75% over the past year.

Across Asia, the total addressable market for life insurance premiums is expected to double to $1.6trn by 2033. With insurance penetration still in low single digits in key markets like China and India, and a rapidly expanding middle class, the potential for growth is enormous.

Of course, no investment is risk-free. The insurer faces challenges, including exposure to China’s recent property bubble collapse, interest rate fluctuations, and regulatory uncertainty, which could affect growth and returns. A slowdown in these markets could impact profits, and geopolitical tensions or policy changes also need to be carefully considered.

Bottom line

The business is in the midst of a multi-year transformation, showing clear momentum in earnings and cash generation. While dividends remain modest, the real appeal for a growth-focused ISA is the compounding potential of retained profits as Prudential captures this massive market opportunity.

I recently added to my holdings. Its combination of structural growth potential, deep expertise in Asian markets, and universal brand recognition were the key drivers behind my decision.

No single stock will carry an ISA to £500,000 on its own, but Prudential is a company worth considering for investors looking to let capital do some of the heavy lifting.