Aston Martin Lagonda‘s (LSE:AML) share price continues to crash and, at 69.7p per share, is down 36.1% since the start of 2025.

This takes total losses over the last year to just shy of 60%. Someone who parked £10k in the FTSE 250 company would now have just £4,308 sitting in their account.

Weak sales to China, supply chain disruptions, and high debts have left Aston’s shares floundering. To add to the automaker’s woes, new tariffs of 25% on US car imports threaten to cripple sales in a critical market.

Yet none of this seems to faze City analysts. Forecasters are unanimous that James Bond’s favourite car manufacturer will rise in value over the next 12 months.

So how realistic are Aston Martin’s share price estimates? And should investors consider buying this beaten-down share for their portfolios?

Good value on paper

The most bullish broker believes Aston Martin shares will rise 151% over the next year, to £1.75. This is significantly higher than the least optimistic estimate of 79p, though this is still up 13.5% from current levels.

The average price target among eight brokers who study the share is £1.18 per share. That’s up 69.3% from today’s levels.

As I’ve mentioned, Aston has a lot of obstacles to try and overcome. However, the motormaker’s fans may argue that this is more than baked into the current valuation, leaving room for a price rebound if performance stabilises or even improves.

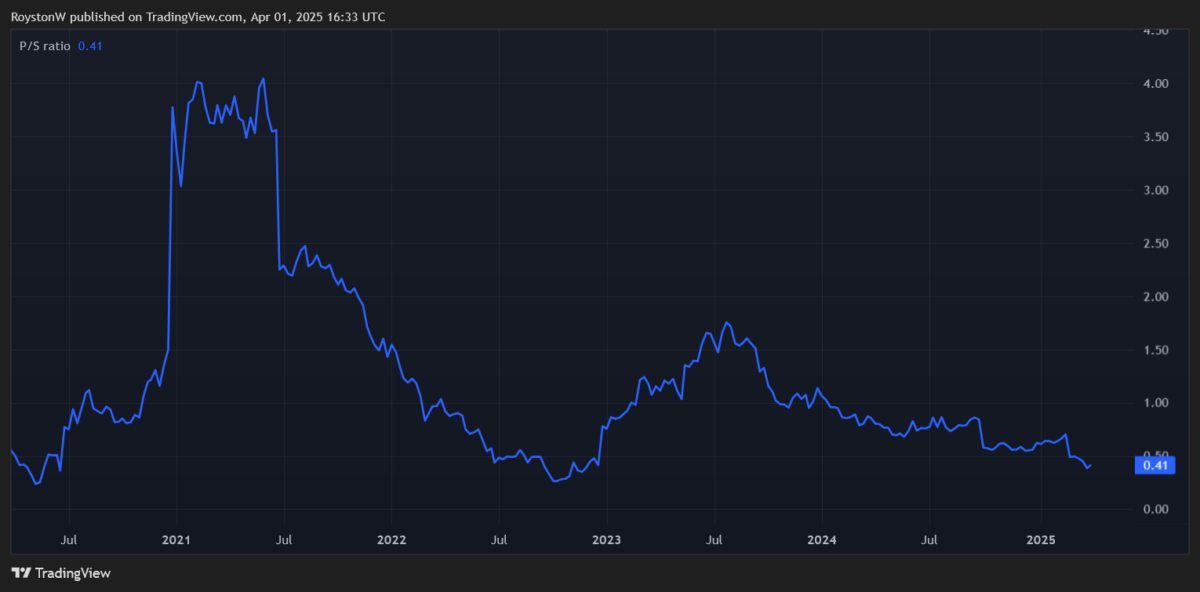

The business is expected to remain loss-making though to 2026, so let’s use the price-to-sales (P/S) ratio instead of price-to-earnings (P/E) to ascertain its value.

With a sub-1 score of 0.4, Aston shares score extremely well on this value metric.

Let’s also consider the company’s price-to-book (P/B) ratio to work out how cheap it is. This is based on Aston’s book value, which is equal to its assets minus its liabilities.

Again, this comes in at below 1.

Are Aston shares a potential Buy then?

Yet while the City’s extremely chipper over Aston Martin’s share price prospects, I’m not so optimistic. Not even those low P/S and P/B ratios are enough to win me over.

As a car enthusiast, I love the Warwickshire company’s luxury products. To me, Aston symbolises speed, elegance, and exclusivity. The trouble is that these aren’t qualities that set it apart from the competition. It has to go wheel to wheel against other famous marques like Ferrari, Porsche, Bentley and Lamborghini to win market share.

Tough economic conditions in its key US and Chinese markets — which could be made considerably worse by the rollout of global trade tariffs — make Aston’s task of growing sales even more challenging.

All this is especially concerning given the huge debts Aston has. Net debt was a gigantic £1.2bn at the end of December.

The company will be hoping new product launches light a fire under sales numbers. Chief executive Adrian Hallmark has said its Valhalla hybrid scheduled for launch this year “will help us reposition Aston Martin again.”

But I’m not so sure. On balance, I think Aston’s share price could remain locked in reverse, so I’d rather buy other UK shares.