Passive income from stocks is often regarded as one of the most appealing aspects of investing. It offers individuals the opportunity to generate a steady stream of earnings without active involvement in day-to-day business operations.

So what’s my passive income strategy for targeting retirement at 50?

Time is key

At the age of 30, with a retirement goal set at 50, I have a significant advantage — time.

Having a 20-year investment horizon provides me with the invaluable opportunity to nurture and grow my current portfolio into something substantial.

This extended period allows me to harness the power of compounding, where my investments can potentially multiply and generate substantial returns over time.

By strategically allocating my assets and staying committed to my financial objectives, I can aim to build a portfolio that not only provides financial security but also creates a substantial passive income stream, offering me the possibility of a comfortable and fulfilling retirement.

Compounding

Compound returns might not sound like a game-changer, but it really is.

First, I need to start by investing my money in assets like stocks or bonds. Then I need to be patient and resist the urge to constantly tinker with my investments. As time goes by, my investments will generate returns, and these returns will get reinvested.

Here’s the key. I must avoid withdrawing those returns and let them stay invested alongside my original capital. This way, I’m not just earning returns on my initial investment, but I’m earning returns on the returns I’ve already earned.

Over the years, this compounding effect can snowball, significantly growing my wealth.

To make it work efficiently, I should keep adding to my investments regularly, whether it’s monthly, quarterly, or annually. This practice, known as pound-cost averaging, can amplify the benefits of compounding.

In a nutshell, compounding returns require me to invest wisely, be patient, and let time work its magic. It’s a recipe for building long-term wealth and achieving my financial goals.

Aiming for an early retirement

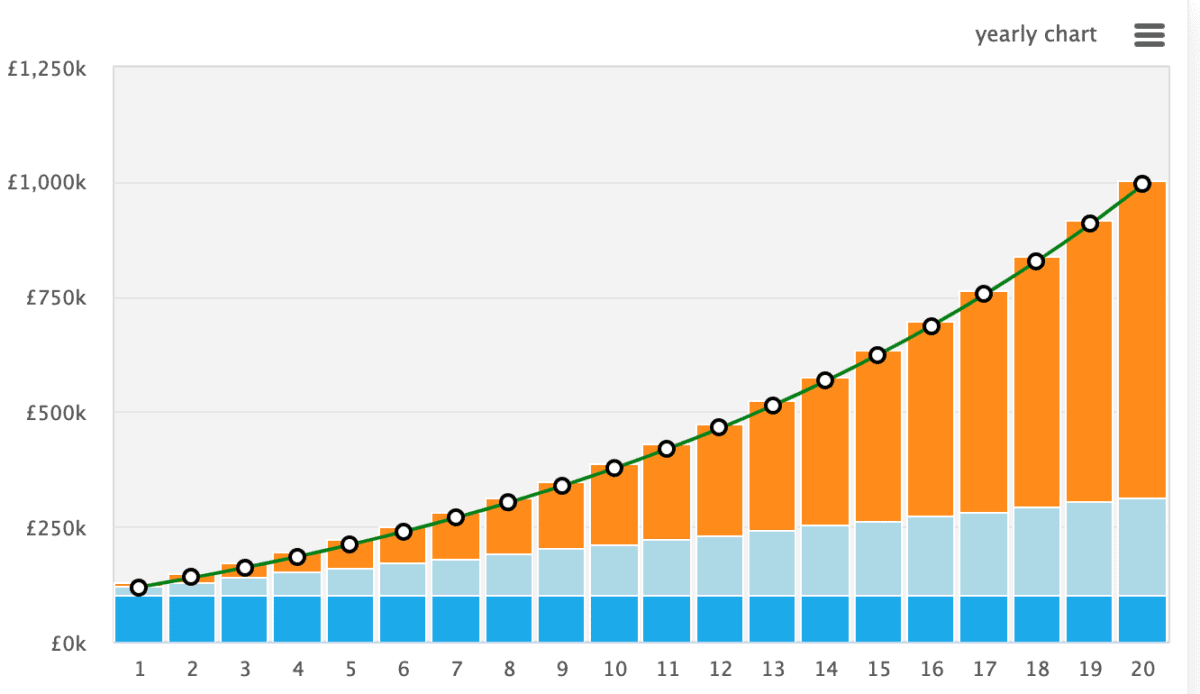

To answer my question in the title, I have to say, yes — but it’s not easy. Here’s an example of how I could grow my investments over 20 years and retire at 50.

Before anything else, I’m need to set out my financial objectives. If I’m going to retire in 20 years, I’m going to suggest I need at least £60,000 after tax. In turn, that means I need at least £1m in my account — preferably in an ISA as dividends here are shielded from tax — and an average 6% dividend yield.

Please note that tax treatment depends on the individual circumstances of each client and may be subject to change in future. The content in this article is provided for information purposes only. It is not intended to be, neither does it constitute, any form of tax advice. Readers are responsible for carrying out their own due diligence and for obtaining professional advice before making any investment decisions.

Let’s start by assuming I’ve got £100,000 invested as a starting point.

Then I’m going to need to continually invest, while reinvesting my returns each year. Using my 20-year investment horizon, I’d need to contribute nearly £10,000 a year, while achieving an annualised return of 8%.

Of course, these figures can vary. And there are lots of ways to reach £1m. This is just one route. An easier way would be to start much earlier, maybe retire a few years later and not have to invest quite so much each year.

However, either way, it’s important to remember that if I choose investments poorly, I could lose money. As such, I need to make sure I’m doing my research and taking advantage of resources like The Motley Fool.