Marks & Spencer’s (LSE:MKS) recent makeover has boosted both the perception of its brand and its shares. Over the past few years, the British icon has managed to shed its reputation for catering only for older customers and being a bit, well, middle-of-the-road.

Victoria Wood, the British comedian, once joked: “I know I’m different sizes in different shops, 16 in some, 18 in others. In Marks and Spencer’s, I’m only a size three because they don’t want to upset anybody.”

Then and now

Although those who bought the retailer’s shares in April 2021 might not be laughing all the way to the bank, they’re probably patting themselves on the back.

A £5,000 investment at the time would have bought 3,185 shares. Today (15 April), they’re worth (excluding dividends) an impressive £11,498. As an illustration of how well investors have done, the same investment now would get them 1,800 fewer shares.

But does a 130% rise in the retailer’s share price mean it’s too late to consider the stock? Let’s see.

Growth opportunity

Although the group is probably more talked about for its clothing, it’s the food side of the business that most interests me.

Over the past three financial years, fashion, home, and beauty customer numbers have remained flat. Last year, they were overtaken by grocery shoppers for the first time. Food customers have increased 9% over the period and, significantly, they’re making an average of 2.9 more visits a year to the group’s shops.

Indeed, the company has set itself the target of doubling the size of its grocery business over the long term. To achieve this, it’s aiming to increase its number of food-only stores from 328 to 420.

Sometimes it’s forgotten that, since September 2020, the group’s had a joint venture with Ocado. During the 12 weeks to 22 March, it recorded a 2.2% share of the British grocery market. It’s never been higher.

Some challenges

Undoubtedly, there was a loss of investor confidence following last year’s cyberattack. This cost a lot to put right but, more significantly, led to some loyal customers shopping elsewhere.

Despite this, they came back and the group’s reputation with consumers appears unharmed. According to polling by YouGov, based on a combination of perception, quality, value, reputation, and satisfaction, it remains the nation’s best brand.

Of course, operating a chain of shops is logistically challenging. And the fashion industry is notoriously difficult to get right with consumer tastes changing quickly. That’s another reason why I believe the emphasis on its less-cyclical food business is the right strategy.

Final thoughts

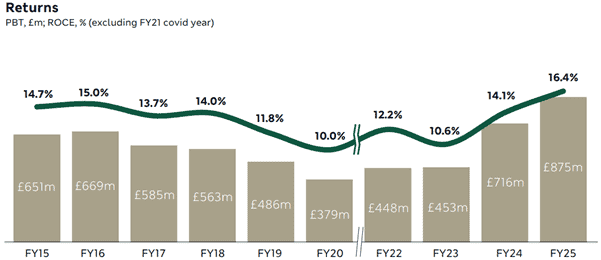

Personally, I think the group’s made great strides over the past 10 years or so, with progress only interrupted by the pandemic. Both its profit before tax and return on capital employed are going in the right direction.

And despite changing shopping habits, it remains an important part of Britain’s high streets and retail parks.

I like what I see. That’s why I think it’s a stock to consider.