Lloyds‘ (LSE:LLOY) shares have lost their momentum. Since hitting 115p in early February, they’ve fallen as low as 88p. Now, while they could rebound to £1.15 in 2026, I wouldn’t rule out a move lower.

Here’s a look at how they could potentially fall back to 70p.

High oil prices could hurt the banks

The way I see it, there are three main risks for Lloyds right now. The first is a prolonged period of high oil prices. This would almost certainly be bad for the banks, because high oil prices tend to hurt consumers and businesses and lead to a slowdown in economic growth.

For banks, a slowdown in economic growth tends to translate to lower demand for loans and/or high loan defaults. This, in turn, translates to lower profits.

It’s worth noting that a sharp increase in oil prices (like we’ve just seen) tends to be more damaging to consumers than a slow rise. A sharp spike can really mess with people’s finances (eg sudden petrol cost spikes) and impact their ability to service loans.

A new source of competition

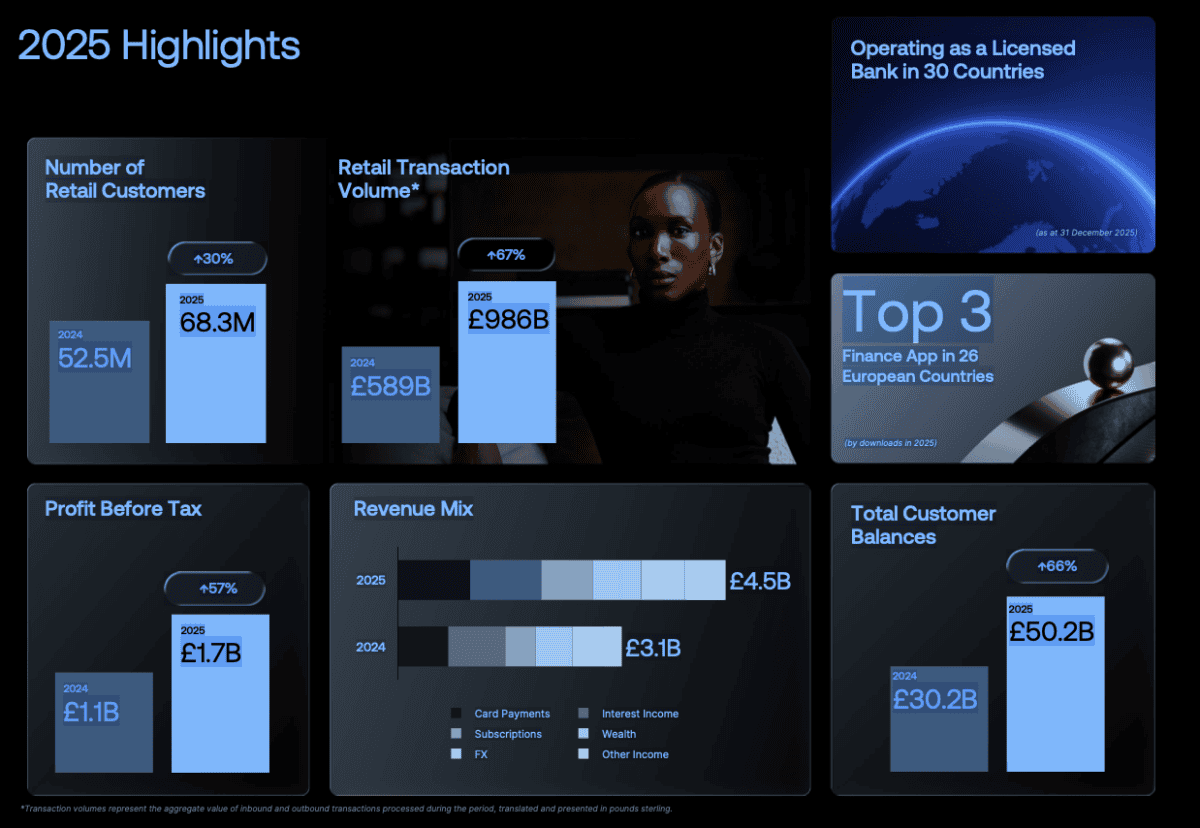

The next risk is competition from digital bank Revolut. No one’s really talking about this right now, but I don’t think we can ignore it. Revolut now has a full UK banking licence. This means that it can compete with Lloyds in areas such as savings accounts and loans.

I expect it to capture market share from the traditional banks in the years ahead. Because it has a really compelling offering.

For example, pay £14.99 a month for its Metal card and you get travel insurance, Uber One membership, access to Perplexity Pro, a Financial Times digital subscription, Class Pass vouchers, WeWork credits, NordVPN access, and more. I don’t see Lloyds offering great deals like this.

It’s worth noting that Revolut is having success both at consumer and business level right now. At the end of 2025, it had 68.3m retail customers (+57% year on year) and 767,000 business customers (+33%).

The AI risk

Finally, we have the artificial intelligence (AI) threat. If companies continue to lay off white collar employees, there’s a genuine chance we could see a spike in loan defaults. This is another risk that can’t be ignored. Businesses that have announced layoffs this year include HSBC, Block, Oracle, and Klarna.

The bull case for Lloyds

Now, of course, these risks and scenarios may not come to fruition. We could see oil prices drop, Lloyds fend off Revolut, and laid off employees move into new roles created by AI.

We could also see Lloyds use AI to its advantage and cut its costs significantly. In banking, AI can be used for identity verification, account opening, customer service, regulation scanning, and much more.

If things played out like this, we could see Lloyds shares hit £1.15 again. They could even keep rising beyond this level.

I’m just not super-confident the shares will return to £1.15 in 2026 though. They could still be worth considering below £1. However, in my view, there are better shares to consider buying today.