State Pension concerns are growing — and for many, it may not be enough for a comfortable retirement.

With markets volatile and the cost of living still high, relying on a single income in later life looks increasingly risky. The State Pension provides a foundation, but it was never meant to do the heavy lifting.

The real risk? Waiting too long to act.

So what can investors do now to take control of their future income? For me, it starts with putting money to work consistently — especially during volatile periods when long-term opportunities begin to emerge.

Volatility is opportunity

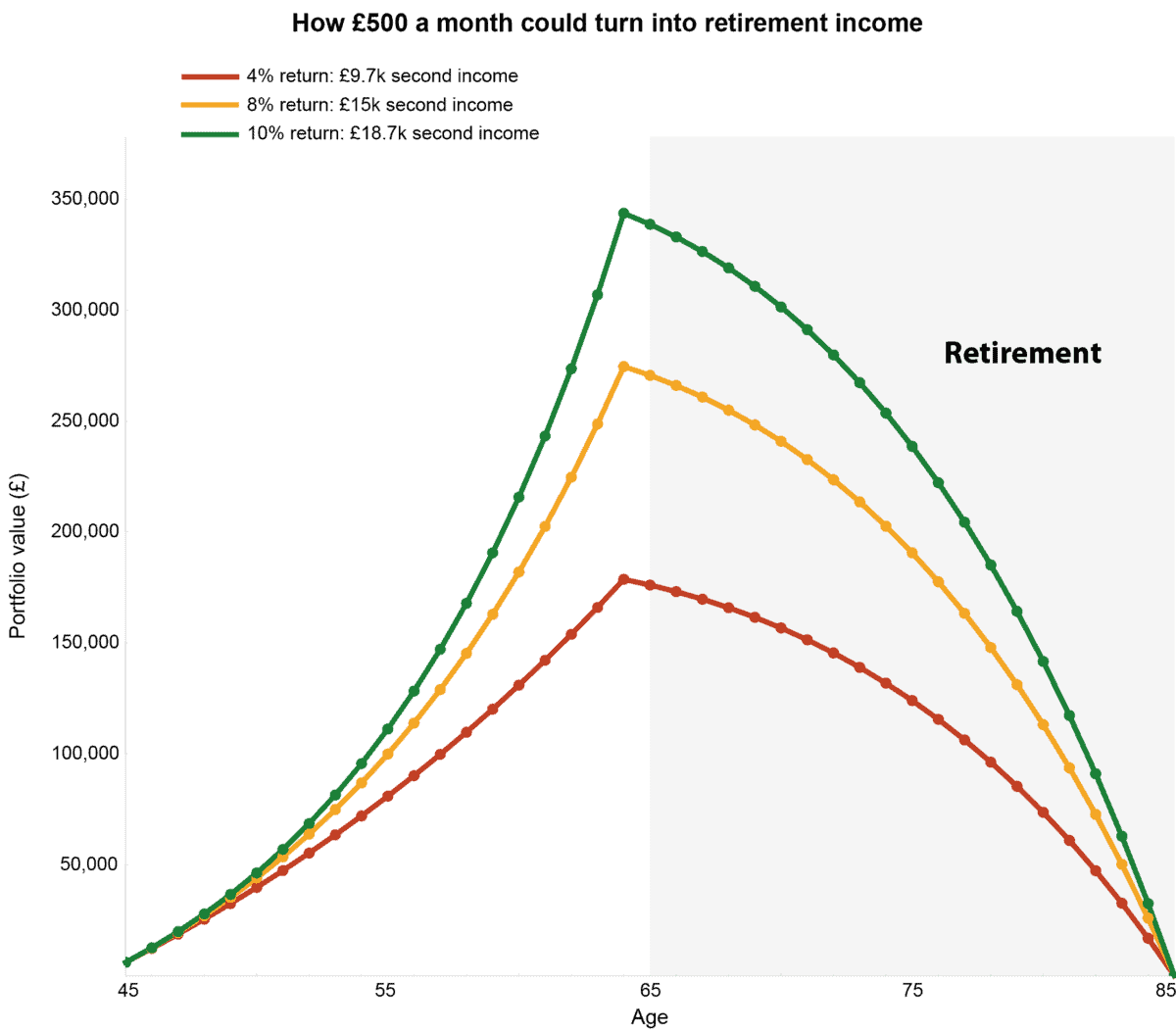

The chart below shows how a consistent £500 a month invested over 20 years could translate into very different levels of retirement income, depending on long-term market returns.

A 4% annual return translates into around £9,700 a year of second income. At 8%, this rises to nearly £15,000. And at 10%, it climbs to around £18,700.

Chart generated by author

Over a full retirement, that difference can add up to tens of thousands of pounds in extra income — or the shortfall that forces tougher financial decisions later in life.

And this is where volatility actually becomes important.

Market swings aren’t just noise — they can be opportunities to buy into stronger future returns at lower prices. For long-term investors, that can meaningfully increase the size of the retirement pot that ultimately drives income later in life.

Which is why the real risk isn’t volatility itself — it’s failing to take advantage of it while time is still on your side.

Falling stock

One stock caught up in the recent sell-off is National Grid (LSE: NG.). The share price is down around 12%, which has pushed the dividend yield up to roughly 4%. It may not look spectacular at first glance — but there’s more to this one than meets the eye.

If the State Pension is starting to look uncertain, this is one of the closest things in the UK market to a private pension-style income stream — predictable, inflation-linked, and built on essential infrastructure rather than economic cycles.

National Grid operates the electricity transmission networks that keep the UK and parts of the US running. It’s a regulated business, meaning returns are largely set by frameworks agreed with regulators. That translates into highly visible future income streams.

More important than the starting yield is how that income can grow, with dividends expected to track CPIH over time.

It’s not risk-free. Large infrastructure projects bring execution challenges, and regulatory shifts or higher interest rates can weigh on valuations — part of the reason the shares have pulled back.

But that’s where the opportunity lies. Share price volatility doesn’t necessarily reflect volatility in the underlying income stream, allowing long-term investors to build positions at more attractive levels.

Bottom line

For me, investing through market cycles is about building reliable income streams of my own, rather than relying on a State Pension that’s increasingly uncertain. And with the world rapidly electrifying — from EVs to AI-driven data centres — demand for grid infrastructure is only heading one way.

National Grid offers a way to tap into that trend while steadily compounding inflation-linked income, using market volatility to lock in better long-term returns. And it’s just one of several opportunities I’m looking to take advantage of right now.