FTSE 100 share prices have been all over the place of late. And that can create opportunities for investors who can find them.

One stock in particular stands out right now and may be worth a look. It’s down 38% in the last 12 months, but analysts think it could climb 76% from its current level.

The stock

The stock in question is Barratt Redrow (LSE:BTRW), the UK’s largest housebuilder by volume and revenue.

There are several reasons the stock’s been falling. Excess inventory, combined with increased costs and higher interest rates are industry-wide issues.

The company however, also has challenges of its own. Its interim update in February warned that profits might fall short of expectations. On top of this, the firm’s announced a change of leadership with the CEO stepping down. That creates additional uncertainty.

All of this makes Barratt Redrow look like the wrong stock at the wrong time. But that’s exactly why it might be an opportunity.

Cyclicality

Housebuilding is an inherently cyclical industry and Barratt Redrow isn’t the only company seeing recent challenges. The UK currently has both an excess of housing and a major affordability problem. That’s just about the worst situation for builders.

Fortunately though, it’s unlikely to last forever. There’s a structural shortage of housing and some of the challenges look temporary.

The conflict in Iran is a major source of inflation. That’s pushing up build costs and threatening to keep interest rates high. When will that end? I’m not sure, but I don’t think it’s going to last forever – and housebuilders stand to benefit when it finishes.

Long-term strength

In a situation like this, there’s one thing I think can give a business a big long-term advantage. And Barratt Redrow has it. It’s a cost advantage. Having lower costs allows a company to shift excess inventory by cutting prices while still remaining profitable.

There are a few ways for a firm to achieve this, but the most common is scale. This makes for better negotiating power with suppliers. That’s exactly what Barratt Redrow has. It accounts for around 10% of homes built in the UK — the largest by some distance.

What we have then, is a firm with a key strength in an industry that’s in a cyclical downturn. It’s easy to see why analysts are interested.

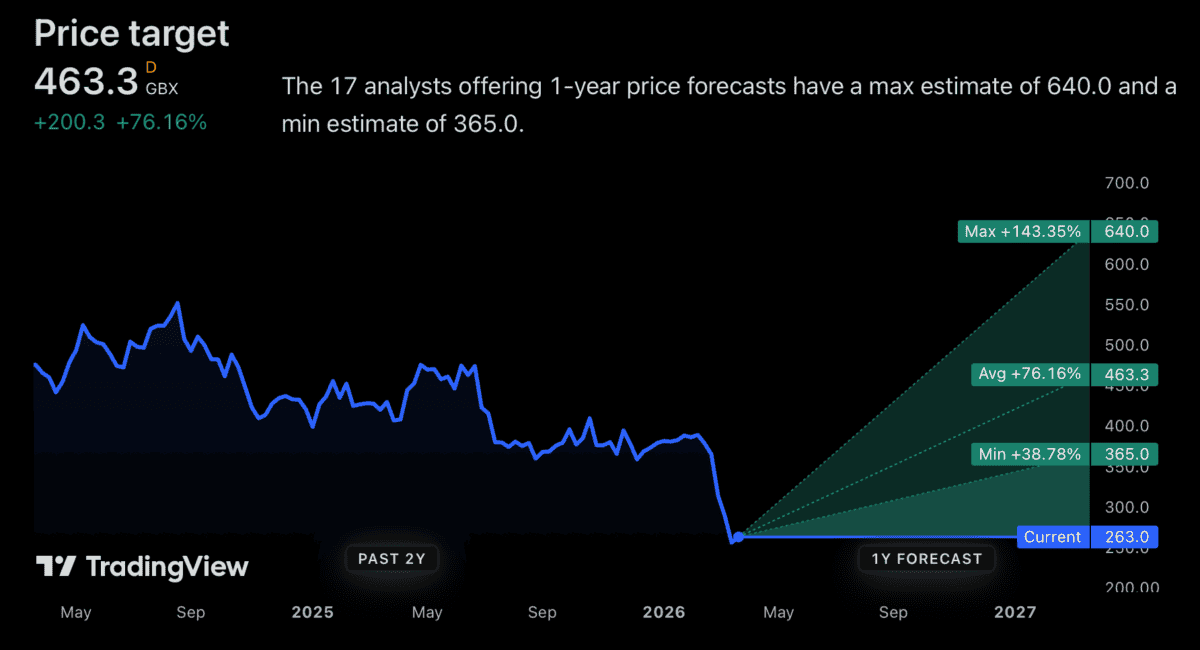

The analyst view

Right now, the average analyst price target for Barratt Redrow is £4.63. That’s 76% above the level the stock’s trading at right now.

Source: TradingView

No FTSE 100 stock has a bigger gap from its current level to its average price target. So it’s fair to say the company is the analyst favourite.

The stock’s ability to get to that level depends on some of the wider economic pressures easing. And the company can’t do much about that. Over the long term though, Barratt Redrow’s scale gives it a clear advantage. And it’s hard to overstate how important that might be.

In terms of my own portfolio, I haven’t been buying the stock. But that’s only because there’s another housebuilder I like even more.