It didn’t last long, did it? The recent rally in the Diageo (LSE:DGE) share price was an indication that many investors saw it as a value stock ready to bounce back. That was until Wednesday (25 February), when the drinks giant released its results for the six months ended 31 December 2025 (H1 FY26). Its shares closed the day 12.7% lower.

But does this mean it’s now a bit of a bargain? Let’s take a closer look.

A false dawn

From 7 January to 24 February, Diageo’s share price increased 18.8%. After a long period in the doldrums, investors seemed to be warming to the stock once more.

Perhaps they were enthused by the appointment of Sir Dave Lewis, previously of Unilever and Tesco, who has earned a reputation for being a bit of a turnaround specialist? ‘Drastic Dave’ took up his position as chief executive at the start of the year, so he’s not responsible for what happened in 2025.

Even so, investors seemed disappointed by the 2.5% drop in adjusted earnings per share compared to H1 FY25. And the 50.6% cut in the interim dividend “to a more appropriate level to accelerate the strengthening of the balance sheet and create more financial flexibility” probably didn’t help their mood.

What’s going on?

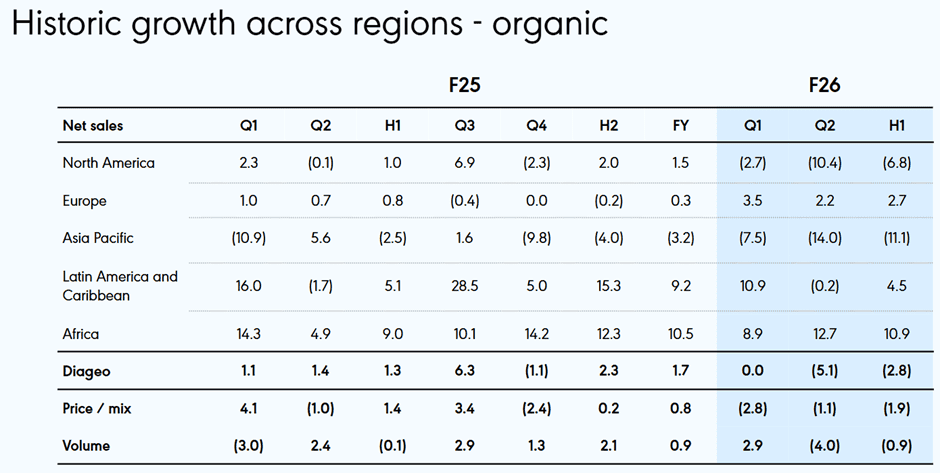

Delve deeper and the results paint a confused picture.

Looking at the change in organic net sales shows no discernible pattern other than Africa continuing to do well. Those hoping for the green shoots of a recovery are likely to be disappointed.

However, based on adjusted earnings per share over the 12 months to 31 December 2025 (119.3p at current exchange rates), the stock’s now (27 February), trading on an earnings multiple of just 13.3.

Compared to recent history and others in the sector, this is incredibly cheap. For context, as the world emerged from the pandemic, Diageo had a price-to-earnings (P/E) ratio of well over 30.

| Financial year | Share price (pence) | Earnings per share (pence) | Price-to-earnings ratio |

|---|---|---|---|

| 30.6.21 | 3,461 | 117.3 | 29.5 |

| 30.6.22 | 3,531 | 149.2 | 23.7 |

| 30.6.23 | 3,379 | 145.2 | 23.3 |

| 30.6.24 | 2,489 | 132.7 | 18.8 |

| 30.6.25 | 1,828 | 121.3 | 15.1 |

But the business was growing back then. Now, it’s shrinking. And unless it can reverse this trend, the P/E ratio is irrelevant.

A challenging market

Diageo’s struggling to cope with squeezed consumer incomes and uncertainty over US tariffs. More fundamentally, younger people are drinking less. They are also engaging in ‘zebra striping’, which involves alternating between alcoholic and non-alcoholic drinks on a night out. Weight-loss drugs and legal cannabis products are a minor concern for the group.

At the start of the year, I was confident that the business would soon start to recover. Although I didn’t subscribe to the ‘too big to fail’ theory, I thought its size would give it the financial firepower to turn things around. The group owns some of the biggest brands in the business, most notably Guinness, and it has all price points covered in its key markets.

However, it now looks as though it’s going to take longer to bounce back than I originally thought. Diageo’s turnaround strategy was in play long before its new boss arrived on the scene. But it’s going to take Sir Dave to focus minds and cut out the dead wood. I think he has the skills to succeed. That’s why I haven’t changed my mind and I still think Diageo’s a long-term recovery stock to consider buying.