Banco Santander (LSE:BNC) shares certainly haven’t been left out of the European bank stock rally in recent times. In just 12 months, they’ve jumped from under 500p to 935p.

Including dividends, this powerful performance would have transformed a £15,000 investment into almost £30,000.

Even more incredible is the performance since July 2022. Over this period, Santander stock has skyrocketed roughly 360% — enough to turn £15k into approximately £70k!

Why are investors so bullish on the Spanish bank stock? And might it still be worth considering today?

A high-performing bank

Santander operates in 10 core markets across Europe, the US, and Latin America. Like all banks, it has benefitted from higher interest rates. This has boosted its net interest margin (the difference between the interest earned on loans and paid out on deposits).

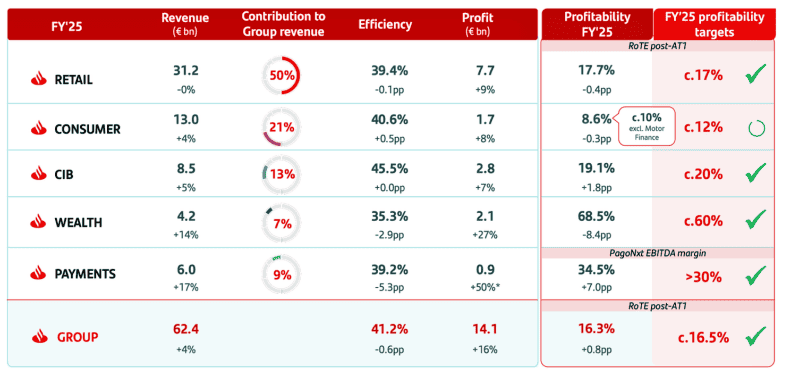

In 2025, the lender’s profit rose 12% to €14.1bn, marking the fourth consecutive year of record results. Earnings per share (EPS) jumped by an impressive 17%, boosted by Santander’s meaty share buybacks.

Since 2021, the company has repurchased around 18% of its outstanding shares. And dividend payments have been more generous than in previous years (when Santander was seen as slightly stingy).

Meanwhile, loan-loss provisions are stable, with a solid cost of risk at 1.15% last year, supported by “proactive risk management, low unemployment rates and easing monetary policies in most countries“.

The non-performing loan ratio improved to 2.91%, an historically low level. So while the volatile geopolitical backdrop adds risk, conditions have actually been pretty benign.

During the year, Santander added another 8m customers, bringing the total to 180m. It also snapped up Webster Financial in the US, where it intends to become a major player in retail banking.

Santander estimates this acquisition will nearly double its return-on-tangible-equity (RoTE) ratio, a key measure of profitability, to 18% in the US by 2028. And it will deliver about 7%-8% EPS accretion for the group.

Looking ahead, management expects higher profits in 2026 and 2027, with group RoTE expected to exceed 20% by 2028.

What about the dividend yield?

I’ve been bullish on Santander stock for some time due to its good mix of markets, both mature (US, UK, Spain) and growth (Brazil, Mexico, Chile). I see this geographic diversification as a key strength.

“The US economic outlook is stronger than expected, Europe is gaining momentum and Latin America stands out as a clear winner in terms of competitiveness in the new global context“, said Ana Botín, Santander’s executive chair.

Is Santander still worth a look? It might be for investors who are bullish on Latin America long term. The region is home to tens of millions of unbanked or underbanked people, which should support financial services growth for many years to come.

However, I note Santander’s price-to-tangible-book (P/B) ratio is 1.8. This represents the hard assets of the company, and suggests the valuation might be a tad high right now.

Plus, after the strong share price run, the forecast dividend yield is only 2.8%. From an income perspective, that doesn’t seem attractive to me when I can get Aviva and HSBC on prospective yields of 6.4% and 4.5%, respectively.

Investors can make up their own minds, of course, but I see more potentially lucrative opportunities in other financial stocks today.