In 2025, silver mining company Fresnillo (LSE: FRES) was the FTSE 100’s best performer (by a wide margin). Its share price jumped from 603p to 3,334p – a gain of about 450%.

Should investors consider buying this stock while it’s hot? Let’s discuss.

Why Fresnillo shares are on fire

It isn’t hard to see why Fresnillo shares soared in 2025. This company’s widely considered to be the largest silver miner in the world. And silver prices rocketed last year. After starting the year near $30 per ounce, the price of the precious metal surged as high as $84 per ounce late in the year.

When precious metal prices jump like this, it typically leads to exponentially higher profits for producers. Because these companies tend to have relatively fixed operational costs (meaning increases in spot prices tend to fall straight to the bottom line).

Looking at forecasts, analysts expect Fresnillo to post a net profit of $1,145m for 2025, up from $141m in 2024. That would represent an increase of 712%.

Given that enormous expected profit increase, it’s no wonder the share price is up significantly.

Worth a look in 2026?

As for whether the shares are worth a look today, that really depends on an investor’s view of where silver prices are heading next.

There are a few reasons silver is in a strong uptrend at the moment. One is that gold’s rising. When it rises, silver tends to tag along for the ride. Another is that silver’s needed for a range of industrial applications including electric vehicles (EVs), solar panels, and data centres. And right now, there’s a shortage of the precious metal.

Now, looking ahead, gold could keep rising and demand for silver could remain strong. So silver prices could continue to climb (some experts are targeting $100 per ounce in 2026).

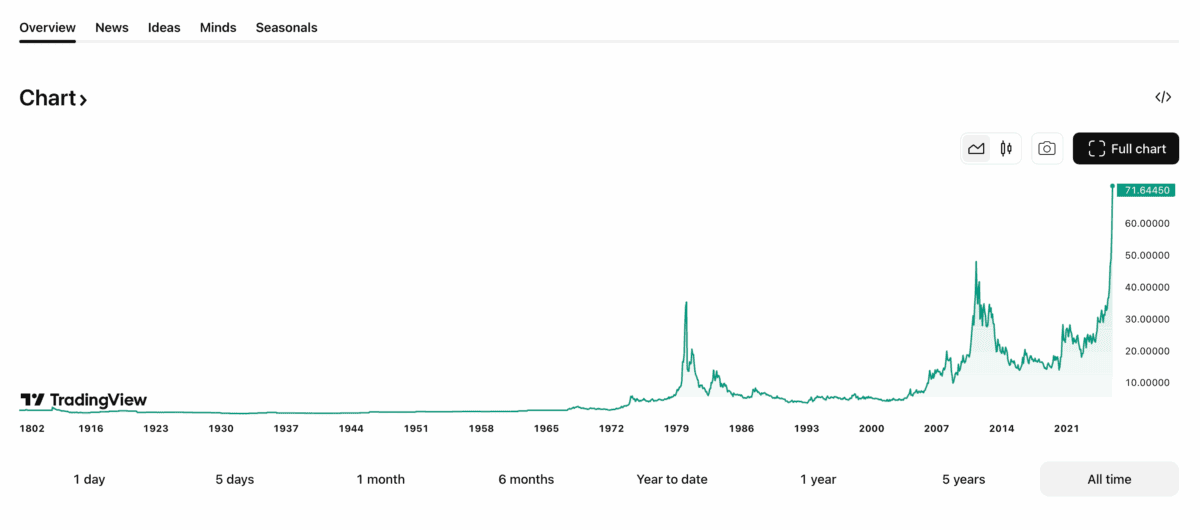

However, looking at a silver price chart, it looks a little scary to me.

Recently, the price has gone parabolic. That doesn’t look sustainable (I think there’s a bit of speculative excess in the price right now). I’ve seen that kind of chart many times before. And it almost always ends badly. Just look at how silver prices crashed in 2011. The fall was nasty.

If the price of silver was to plummet from here, investors in Fresnillo could be looking at ugly losses. That’s a scenario to consider.

High valuation

Zooming in the stock itself, it currently trades on a forward-looking price-to-earnings (P/E) ratio of around 21. That’s a relatively high multiple for a precious metals producer.

For reference, Newmont, the world’s largest gold producer, is currently trading on a P/E ratio of around 13. So Fresnillo looks expensive on a relative basis.

Note that the average price target for Fresnillo is around £24. That’s about 30% below the current share price.

Better opportunities in the market today?

Given the parabolic silver price and the high valuation here, I think caution’s warranted with Fresnillo shares right now. If an investor is really bullish on silver, the shares could be worth considering.

But weighing up the risks, I reckon there are better opportunities in the market to research as we start 2026.