Earning passive income through a FTSE 100 ETF has become a hugely popular strategy. So I decided to dig into the dividend yields of two leading tracker funds to see how much an investor would actually need to reach £1,000 a month in passive income.

Tracker funds

First up, the iShares UK Dividend UCITS ETF offers a 4.9% yield, while the Vanguard FTSE U.K. Equity Income Index Fund yields 4.2%.

The iShares fund is relatively concentrated, holding just 51 stocks. Vanguard spreads its exposure over 104 holdings.

Despite the difference in breadth, both are dominated by FTSE 100 heavyweights such as BP, Rio Tinto, Legal & General, HSBC, and Shell. A handful of FTSE 250 names also appear, but with much smaller weightings.

Calculations

I do hold the Vanguard fund myself, but I don’t solely rely on it to build passive income. One reason is that several of its biggest holdings aren’t high-yield names, so the income stream is naturally limited.

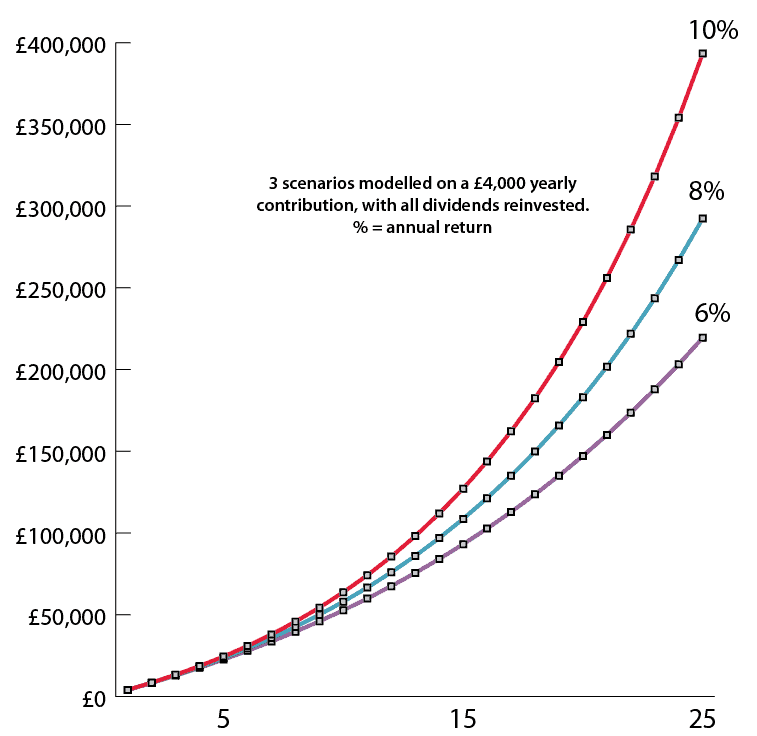

If the goal is £1,000 a month (£12,000 a year), the 4% rule gives us a simple target: you’d need roughly £300,000 in your pot.

And this is where things get interesting.

As the chart shows, using fixed yearly contributions of £4,000 and straightforward compounding at today’s yields, neither ETF gets close to that £300,000 target over 25 years. The income levels just aren’t high enough for the pot to grow at the pace required.

Chart generated by author

That’s why I prefer pairing a tracker fund with individual dividend shares that offer higher, more meaningful yields.

Income and growth

One big FTSE 100 name missing from both ETFs’ top 10 lists is Aviva (LSE: AV.). Its share price has jumped 32% in a year, which naturally pushed the dividend yield down from 8% to 5.5%.

But here’s the key difference with owning individual shares: when you reinvest dividends into a strong company, your holding grows much faster than the slow, spread-out growth you get from an ETF.

Refreshed targets

In its latest update, Aviva laid out three bold targets for 2028: grow operating earnings per share at an 11% compound annual rate, deliver an IFRS return on equity above 20%, and generate more than £7bn in cumulative cash remittances.

To hit these ambitious goals, the company is doubling down on its shift to a capital-light model. Within a few years, it expects over 75% of operating profit to come from areas like General Insurance and Wealth, which require far less capital to grow.

If it can smoothly integrate Direct Line, boost flows through Succession Wealth, and continue scaling via major partnerships such as Nationwide, then these targets start to look genuinely achievable.

No investment is risk-free. For Aviva, falling insurance premiums, regulatory changes, or interest-rate swings could pressure profits and dividends. Unexpected claims or slower growth in capital-light divisions could also limit cash generation, which is key for sustaining payouts.

Bottom line

For me, it’s all about building a reliable stream of passive income. Reinvesting dividends from strong, cash-generating shares has quietly built a growing income stream in my ISA over the years. While the FTSE 100 spreads risk broadly, I’ve found that carefully tracking a few high-yield names can turn steady payouts into a powerful compounding engine. And there are plenty of other high-income stocks to choose from.