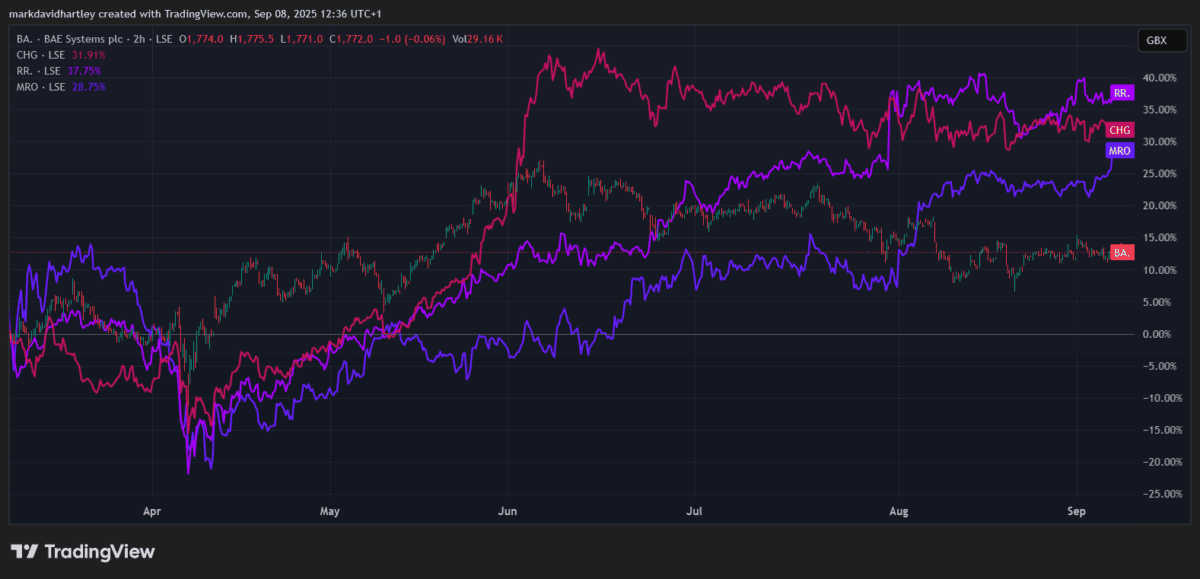

The BAE Systems (LSE: BA.) share price is up an impressive 54% this year. Yet despite that stellar growth, it’s still lagging several of its main competitors.

The past six months have been particularly underwhelming with only 12% growth. That’s significantly less than Rolls-Royce, Melrose Industries and Chemring Group, which have all posted stronger price performances.

Market-cap growth over the past year has also trailed rivals, suggesting that investor enthusiasm hasn’t fully translated into the BAE share price.

What makes this puzzling is that the company continues to secure lucrative partnerships and long-term contracts. So why has investor interest been subdued?

Positive developments

One of the more eye-catching moves this year was the announcement of a partnership with GM Defense and NP Aerospace to form Team LionStrike. This group’s competing for the UK Land Mobility Program, which aims to replace ageing military vehicles with modern, flexible alternatives. The move highlights a renewed focus on ground mobility solutions — a segment where demand looks set to grow.

On top of that, BAE recently secured a $1.74bn contract with the US Navy to supply an advanced laser-guided defence system. This deal not only strengthens its American footprint but also demonstrates that its technology remains cutting edge.

Looking at the fundamentals, the business has a long-term earnings growth rate of 14.4%, with 2025 sales expected to rise 63.4% compared with 2024. Those kinds of projections hardly suggest a struggling company.

Analyst ratings

Despite decent returns, BAE’s still trailed the industry benchmark. As of 3 September, the shares had risen 37% year to date, against industry growth of 39.2%. That may not sound like a huge gap, but it illustrates how competitors have captured a bigger slice of investor attention.

Analysts remain fairly positive. The average 12-month price target from 20 analysts is 2,118p — around 19.5% higher than where the stock trades today. More than half of those analysts rate the shares a Buy or Strong Buy, while seven see them as a Hold or Sell.

Backing that up, Morgan Stanley placed an Overweight rating on BAE on 5 September, signalling that it expects the company to outperform the broader market in the near future.

My opinion

While BAE benefits from steady contracts, there’s an ever-present risk of government defence spending cuts, supply chain disruptions and geopolitical shifts. Heavy reliance on long procurement cycles also makes revenue growth vulnerable to delays.

Still, while the BAE share price may be underperforming the wider industry, the business itself looks healthy. With strong cash flow, a solid balance sheet and a pipeline of long-term defence contracts, the fundamentals remain robust.

That raises an intriguing question. Are investors undervaluing BAE — meaning the shares could catch up to peers — or are there deeper concerns about its ability to keep pace?

For my part, I see no evidence of deeper, systemic issues. With a combination of reliable earnings, a strong order book and supportive analyst sentiment, I think it’s still a stock to consider for those seeking long-term defence exposure.