The FTSE 100’s long lagged the mighty S&P 500. Over the past decade, the US index powered ahead, fuelled by surging tech valuations, while the UK’s flagship index remained stuck under the weight of sluggish banks and oil giants.

But 2025’s delivered a surprise. So far this year, the Footsie’s returned over 7% — slightly ahead of the S&P 500’s roughly 6.5%. That’s a dramatic change compared to recent years, and a sign that UK blue-chips are finally holding their own.

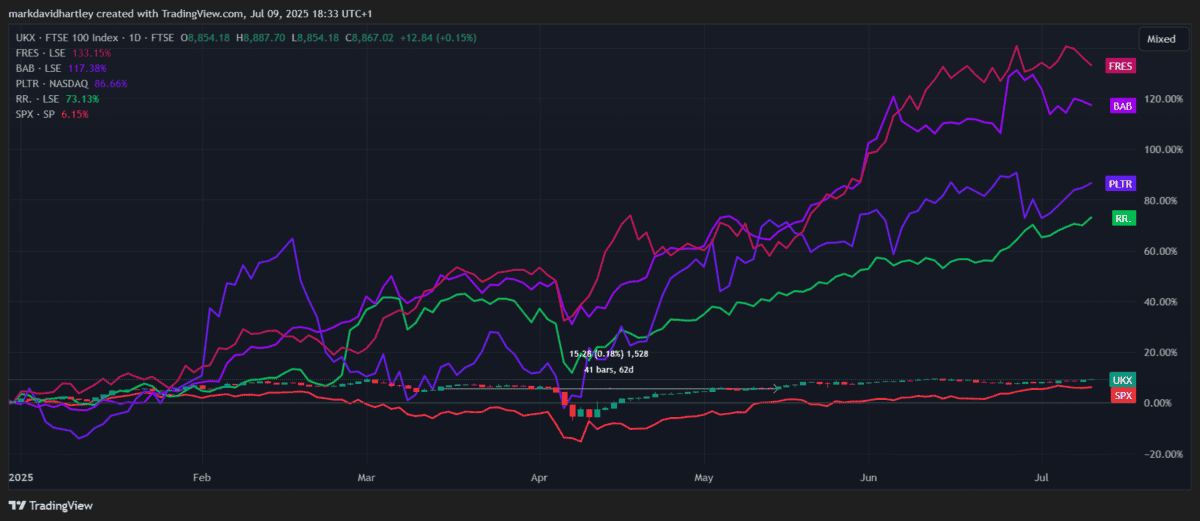

Dig a little deeper, and it’s clear what’s driving this. A handful of FTSE stocks have smashed expectations, outperforming almost every major US company.

Mexico-focused silver miner Fresnillo is up more than 130%, engineering heavyweight Babcock’s surged 116%, and Rolls-Royce continues its astonishing multi-year run, gaining another 73% in 2025 alone.

Of all companies on the S&P 500, only Palantir’s in the top three, edging slightly ahead of Rolls this year with 84%. In fifth place is NRG Energy, up 65% year to date.

What’s driving the surge?

Much of the growth comes down to specific tailwinds. Precious metals are soaring amid global uncertainty, fuelling Fresnillo. Defence budgets are booming, propping up Babcock and Rolls. Meanwhile, a recovering oil price and resilient global demand have helped shore up many FTSE stalwarts.

But some of these moves may be getting ahead of themselves. Share prices that rocket on hopes alone can easily become ‘growth traps’, where valuation disconnects from long-term fundamentals. That’s why I prefer to keep a rational outlook when markets go a bit crazy.

Strong earnings, reasonable valuations and solid balance sheets often matter more in the long run than short-term price jumps.

A more cautious FTSE 100 pick

One stock that’s acting more ‘reasonably’ right now is Beazley (LSE: BEZ). The specialist insurer has quietly delivered moderate growth this year, up 8.8% — nothing flashy, but comfortably ahead of the index’s historical averages.

More importantly, it’s supported by solid operating trends. Earnings per share are growing at 9.9% year on year, with revenue up 7.8%. That’s feeding into a healthy net margin of 18% and an impressive return on equity (ROE) of 26.3%.

Valuation also looks attractive. The shares trade on a price-to-earnings (P/E) ratio of just 6.67 and a price-to-book (P/B) multiple of 1.55, suggesting investors aren’t paying over the odds for this quality growth.

It’s not a big income play, but the dividend yield of 2.8% is well covered by a payout ratio of just 18.3%. Free cash flow is reassuring at £1.26bn, comfortably outstripping its £614m of debt. Plus, the dividend has been raised for three years running.

Risks to watch

Of course, insurance can be a volatile business. Beazley faces exposure to large-catastrophe-linked losses, which could dent profits in any given year. It’s also vulnerable to pricing cycles in speciality insurance, which can swing from lucrative to lean quickly if competition intensifies.

But overall, I think it’s the kind of solid British business that’s worth considering for sturdy reliability.

While growth stocks fluctuate wildly, it’s these steady compounders — trading on sensible valuations — that often deliver the best returns over time. When building a diversified long-term portfolio, that’s exactly what investors should be looking for.