A steady easing of interest rates has driven Lloyds (LSE:LLOY) shares sharply higher over the last year.

At 76.2p per share, the FTSE 100 bank has risen an impressive 36% in value. Investors have piled in on hopes that looser Bank of England (BoE) monetary policy will stimulate the UK economy, which is critical for Lloyds given its limited overseas exposure.

Hopes of sustained interest rate reductions have also fed speculation of a strong housing market recovery, another key segment for the Black Horse bank.

Price forecasts

While Lloyds’ share price gains have been impressive, City analysts believe the bank’s bull run has more fuel in the tank.

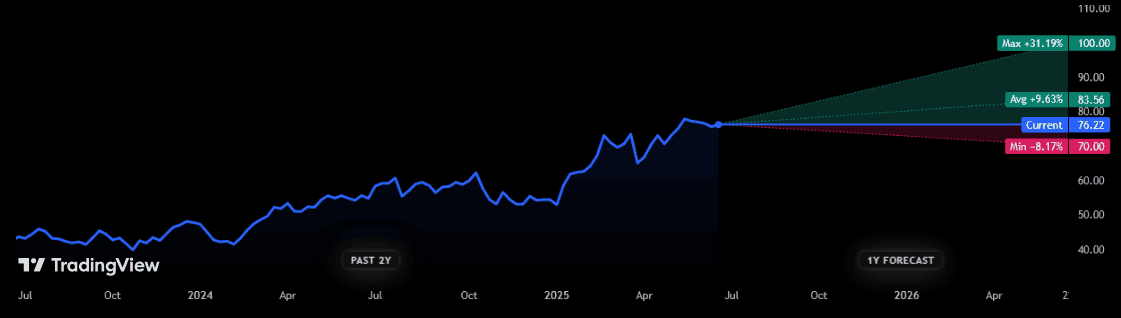

There are currently 16 brokers who have ratings on the bank’s shares. And the consensus is that they will rise by another 10% over the coming 12 months.

It’s critical to note, however, that those analysts aren’t united in their bullishness for Lloyds shares. While one believes the Footsie firm will rise to 100p, another thinks it could reverse back to 70p.

Dividend estimates

Largely speaking though, things are looking positive from the Square Mile’s point of view. Similarly, forecasters are broadly optimistic that dividends will continue growing over the short term, predicting:

- A total dividend of 3.44p per share in 2025, up 9% year on year.

- An annual payout of 4.1p next year, up 19%.

Based on these forecasts, the bank carries healthy yields of 4.5% and 5.4% for 2025 and 2026, respectively. Both figures comfortably beat the FTSE 100 average of 3.4%.

What’s more, predicted growth over the period surpasses the 1.5% to 2% increase that’s tipped for the broader blue-chip complex.

I’m not surprised by the City’s confidence given Lloyds’ balance sheet today. As of March, its common equity tier (CET) 1 ratio was 13.5%. That’s half a percentage point ahead of the bank’s target, and comfortably beats the regulatory requirement of 12%.

Underlining its financial strength, in February Lloyds announced a £1.7bn share buyback programme for the current year.

Is Lloyds a buy?

While City analysts are bullish on the company over the near term, I’m not convinced about the company’s prospects. My view is that its share price gains are overextended given broader industry conditions, leaving it vulnerable to a possible correction.

As I say, the interest rate cuts that have blown Lloyds’ shares higher may keep boosting revenues and reducing impairments. However, such BoE action also threatens to pull net interest margins (which were already thin at 3.03% in quarter one) even lower.

Besides, the UK economy may continue struggling regardless of central bank action, reflecting broader macroeconomic factors (like trade tariffs), government policies and long-running structural problems.

Lloyds faces other problems as well, like mounting competition from challenger banks, and the potential for billions of pounds in misconduct fines. The Supreme Court will rule whether the company mis-sold car finance some time in July.

I think demand for its home loans could remain robust as interest rates fall. And its exceptional brand power could help it effectively limit the impact of competitive threats. But on balance, I think this is a UK share investors should consider avoiding.