Experian (LSE: EXPN) is the kind of stock that’s easily overlooked. After all, its business isn’t particularly exciting: data collection processing and generating credit ratings are probably not the things that you go to bed dreaming of, are they? Despite that, I think Experian is one of the best shares for me to buy today.

Sometimes being boring can be a good thing

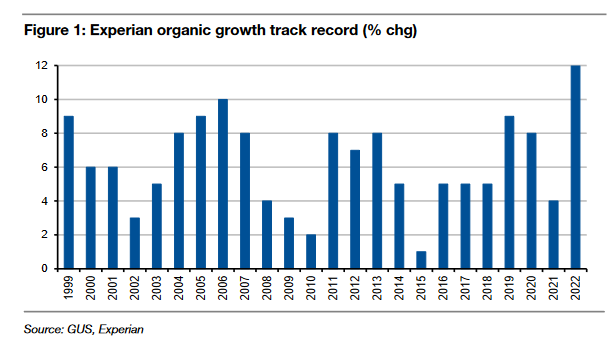

Experian is a £26bn company that generates over £6bn in revenue, which — as of the end of June — was growing that revenue at an impressive 8%.

I say impressive because that growth was generated organically rather than being made through acquisitions, an important distinction.

Experian has a track record of performing well when the economy dips. For example, during the aftermath of the global financial crisis in 2008, Experian’s worst performance was a growth rate of 2%, posted in 2010. Its worst-ever year was 2015 when it still grew by 1%.

Though it’s London-listed, Experian is a global business with operations in North and Latin America, Europe, Africa, the Middle East, the UK and Asia Pacific.

Latin American economies such as Brazil, where the financial services markets are being liberalised, present exciting growth opportunities for Experian.

Investment bank Liberum forecasts that Latin American revenues at the company will grow by 15% in 2023, which would add two percentage points to the group’s organic growth tally.

What’s more, the company has several new products that should launch and scale over the next year.

These include credit card and loan verification tools, and a cloud-based B2B platform that will provide customers with flexible, user-friendly and real-time data access.

Increased use of big data will provide better market intelligence and allow for the creation of new products at Experian. For example, the companies Boost initiative in the US already collects permissioned data from 10m American consumers.

Positive outlook

In its most recent trading update, posted on 14 July, the company forecast full-year growth of between 7% and 9% and said that organic growth in Latin America was running at 18%, and though they were seeing a slowdown in the US mortgage market, this represents just 4% of annual revenues.

However, that slowdown is being offset by strong growth in consumer marketplace products, whilst income from US consumer subscription services remains stable.

In terms of valuation, Experian is trading at around 21 times its 2023 earnings forecasts, with a dividend yield just below 2%, a discount to its US peers, for example, major US rival Equifax currently trades on 24 times earnings with a dividend yield of just 0.78%

Possible risks

Experian’s track record suggests that it should perform well in any future recession.

However, should the rise in energy prices and wider inflation continue unabated for an extended period, then that could damage consumer credit markets and the demand for Experian’s services.

Experian is firmly on my watchlist for my next investment because of its defensive nature, its track record of growth and the opportunity for expansion in the fast-growing Latin American markets.

The share price is down by 23.5% year to date, versus a fall of just 3.4% for the FTSE 100, and that looks unwarranted to me.