The FTSE 250 index is packed with shares offering tremendous value. For proof, we can look at some of the big differences between what City analyst teams think a stock should be worth and what it actually trades for today.

Take Hollywood Bowl (LSE:BOWL) as an excellent example. As I write, it currently costs 253p to buy one share. However, seven brokers have an average one-year price target of 395p.

In other words, there’s a 56% difference. And were this forecast to come to fruition, it could turn a £7,500 investment into £11,700 by mid-2027, with dividends on top.

Admittedly, that sounds too good to be true. What’s the catch?

A tough backdrop

Hollywood Bowl is the largest ten-pin bowling operator in the UK and Canada. Speaking personally, I think it’s a cracking family day out, as kids love it and dads like me can order an ice-cold beer directly to the lane. The centres serve hot food and also have arcades.

The catch is that the UK economy is in a fragile state at the moment, with a potential recession looming. Hopefully this doesn’t happen, as more people tend to lose their jobs during downturns. And this wouldn’t be a great backdrop for Hollywood Bowl.

Reflecting this situation, the share price has fallen roughly 27% in the past two years.

Resilient financial performance

Despite the ongoing inflationary pressures on consumers, the company is actually showing admirable resilience, in my opinion. During the six months to 31 March, group revenue rose 9.5% to £141.5m, with like-for-like growth of 1.9%.

- UK revenue increased 9.4% to £118.4m

- Canada revenue was up 12.8% at constant currency to CAD 42.9m (£23.2m)

As we can see, the UK still makes up the lion’s share of sales. However, Hollywood Bowl is applying its successful expansion blueprint to Canada, where it sees a lot of potential to consolidate the fragmented ten-pin bowling market there.

Two new UK centres and one in Canada are due to open in the current second-half period. The firm, which boasts robust margins, is targeting 130 centres by 2035, up from 93 today.

At the end of March, the firm had a net cash position of £26m, indicating there are no balance sheet issues. Reassuringly, management says 76% of the group’s total electricity needs are hedged until September 2029.

In April, CEO Stephen Burns commented: “Demand for high-quality, family leisure activities that offer great value for money also remains resilient in both territories, and our cash generative business model allows us to invest where we see opportunities and deliver profitable growth.”

Solid value

All in all, Hollywood Bowl appears very well-insulated against any potential weakening of the economy. And right now, I think the stock looks very interesting from a valuation perspective.

Because based on current forecasts, the forward price-to-earnings ratio is just 10.5. And there’s also a market-beating 5.4% dividend yield on offer.

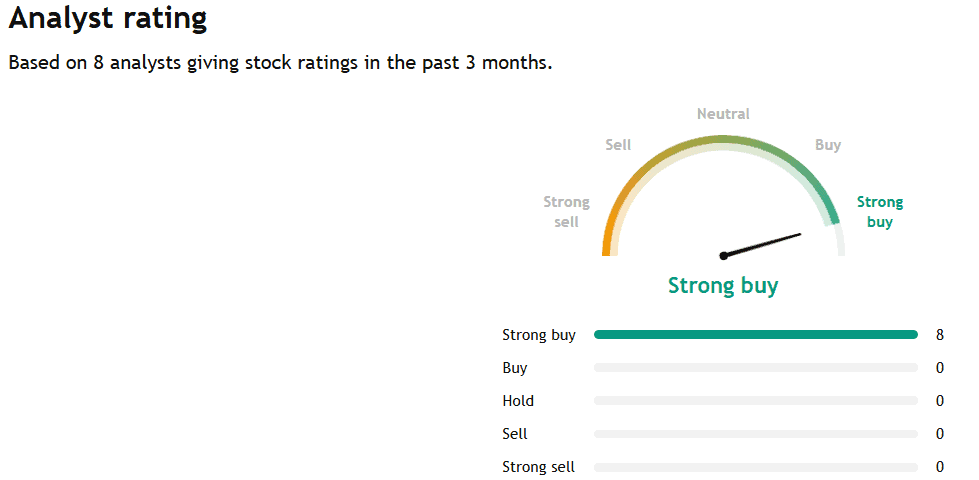

Finally, it’s worth noting that all eight City brokers covering the stock in the past three months rate it as the equivalent of a Strong Buy.

Of course, it goes without saying that these forecasts could prove wrong if inflation hammers the UK economy and consumer spending.

But for investors taking a five-year view, I reckon this cheap FTSE 250 dividend stock deserves a closer look.