The London stock market has long been a great place to find top dividend shares. We’re talking about companies with robust balance sheets, different revenue streams, and market-leading positions in mature industries.

Yet, even by their own excellent standards, UK dividend stocks have impressed in recent months. The result? Analysts now expect British companies to pay fatter dividends in 2026 that had been previously expected.

So what are UK shares now expected to pay this year? And what are the best dividend shares to consider right now?

Dividends soar 21.1%

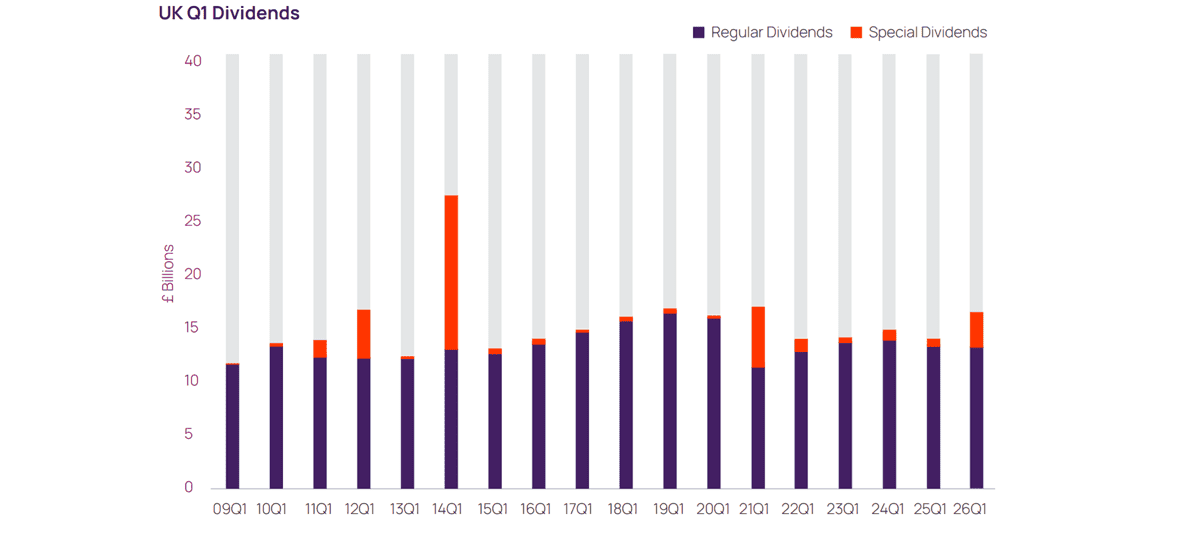

UK shares delivered blowout dividends in Q1 thanks to large special dividends. On a headline basis, payouts surged 21.1% year on year to £16.4bn. That’s according to Computershare.

Ordinary dividends, meanwhile, grew 1.1% at constant currencies to £13.2bn. Both headline and ordinary dividends in Q1 beat Computershare’s prior forecasts.

Computershare says last quarter’s dividends represented

[the] best first-quarter result since 2021. Large one-offs explain the surge, but underlying growth was also a little better than

we forecast in January and set the tone for a better second quarter.

As a result, the financial services firm is now expecting headline dividends of £91.6bn in 2026. That’s up 5.3% from last year, and an improvement from the previously expected 1.5%.

Ordinary dividends are tipped to rise 3.1% to £86.7bn at stable exchange rates. That’s higher than the prior 2% projection.

What could go wrong?

Obviously dividends are never guaranteed. And there are severe dangers to current forecasts as the Middle East crisis rolls on.

Computershare warns that “it is not straightforward to judge how events will affect dividends“, though it adds that “as the oil shock works through the economy, profits are likely to come under pressure across sectors [meaning] less cash for dividends“.

The medium-and-long-term outlooks remain strong for UK dividends. However, rising earnings threats mean those seeking reliable near-term dividends should perhaps look to cash-rich companies with competitive advantages and defensive operations. We’re talking shares such as United Utilities Group (LSE:UU.).

A FTSE dividend hero

This FTSE 100 water supplier isn’t the most exciting of shares. But as a source of dependable passive income it’s hard to beat — indeed, annual payouts have risen for 15 straight years.

United Utilities enjoys strong cash flows across the economic cycle, allowing it to pay reliable and market-beating dividends. For this financial year its dividend yield is a healthy 4%.

Not only do utilities companies provide essential services. They are monopolies in the areas in which they operate, guarding earnings (and therefore dividends) against competitive threats. United Utilities operates a huge water and wastewater network in the North West of England.

So what are the risks of holding United Utilities shares? Rising interest rates could push up borrowing costs, impacting earnings. There’s also the constant threat of regulatory changes to its bottom line. But on balance, I think it’s one of the best dividend shares to consider for a robust income portfolio.