Investing a regular amount in a Stocks and Shares ISA is one way of aiming to boost an individual’s income in retirement. According to government figures, the average pension for a single person is £14,664 a year. This includes pensions paid by both the state and privately. Unfortunately, this will only provide for a basic standard of living.

For added financial security, more is needed. With this in mind, let’s see how someone could aim to earn an identical sum from an ISA.

How do the numbers look?

Investing £257 a month at 8% would grow to £244,400 after 25 years.

Historical returns from the UK stock market suggest that 8% is achievable. But by picking some high-performing growth shares, I believe it’s possible to do better.

A 10% return would reduce the required monthly investment to £194. At 12%, it falls to £142.

Once an ISA has reached target, a portfolio of dividend shares could be bought. With a yield of 6%, this would be sufficient to provide an annual passive income of £14,664, or £1,222 a month.

Is this realistic? Well, the average yield of the top 10 on the FTSE 100 is currently 6.6%.

Something to consider

One company that helps people save for retirement is Legal & General (LSE:LGEN). But with its generous dividend – the stock’s currently (2 May) yielding 8.6% — it could also help boost someone’s income in a different way.

For example, to earn £14,664 in dividends, £170,512 of the group’s shares would be needed.

Given that dividends can be erratic, it pays to be wary of high-yielding shares. Indeed, Legal & General’s is the highest on the FTSE 100 at the moment.

But in this case, I think the payout looks secure for now. My opinion is partly based on the stock’s history – it last cut its dividend during the global financial crisis in 2009 – but also its future prospects.

The UK retirement and savings market is expected to double in size over the next 10 years. Of course, this could also pose a threat leading to increased competition for some of the more established players like Legal & General.

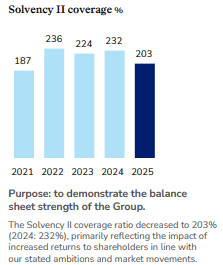

One area to keep an eye on is the group’s Solvency II ratio. It fell sharply during the course of 2025. However, given that it remains over twice the regulatory minimum and higher than many of its rivals, I don’t think it’s much of a red flag at this stage.

Indeed, the company’s growing strongly at the moment. Highlights from its 2025 results include:

- A core operating profit of £1.62bn, 6% higher than in 2024.

- A 9% year-on-year increase in core operating earnings per share.

- An estimated store of future profit of £13.3bn.

Much of this was driven by successfully converting many high-value opportunities from its pipeline of new pension schemes that it’s looking to take over and manage. The higher interest rate environment is also helping its annuities business.

What does this tell us?

In my view, Legal & General is one of many excellent high-yielding income stocks. On this basis, I think it’s one that could be considered by those looking to open up another revenue stream or supplement their pension. But only as part of a diversified portfolio.

Also, growth investors are likely to find other opportunities more attractive.