The new ISA tax year is now upon us, so many people will be hunting for stocks to buy. Especially those at the beginning of their investing journeys who have shiny new Stocks and Shares ISA accounts waiting to be filled up.

At The Motley Fool, we’re big believers in diversification (essentially a fancy term for not putting all your eggs in one basket). In terms of investing, it means spreading your money across different companies, sectors (tech, banking, property, etc), and geographies.

With this in mind, here’s a stock that I think offers something different in terms of growth potential and geographic diversification.

Digital banking powerhouse

Nu Holdings (NYSE:NU) is the company behind Nubank, the largest digital banking platform in Latin America. While founded in Brazil, (still its largest market by far), Nu has expanded to Mexico and Colombia.

Currently a smidgeon over $15, the stock is down 18% since reaching an all-time high of $19 at the end of January.

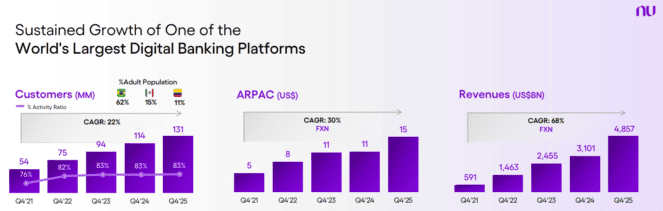

There are a few reasons why I’m bullish on this neobank (and I’m a shareholder). The first is just how quickly it has been able to capture large amounts of customers, with 113m users in Brazil, representing 62% of the adult population. And it now serves over 15% of Mexico’s population!

Clearly then, its product offering is far more compelling than the region’s legacy banks, many of which have long been notorious for high fees and poor customer service. Nubank has a consistently high NPS (Net Promoter Score), displaying customer satisfaction with its service.

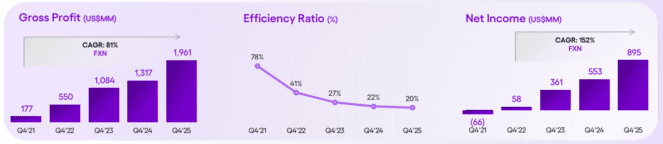

Last year, revenue soared 45% to $16.3bn, with record net profit of $2.9bn. And as the company scales, it’s generating more revenue per client, while keeping customer acquisition costs low (many new customers come via word of mouth). The lender’s credit portfolio expanded 40% to $32.7bn.

Global expansion

While still laser-focused on growing in Brazil, Mexico and Colombia, Nu has firmly set its eyes on international expansion. For example, it has started laying the foundations for US operations.

However, there’s no guarantee that it will have success in the ultra-competitive US market. After all, legacy lenders like Bank of America are hardly slouches when it comes to digital banking.

And there are established fintech players there like Chime, SoFi, and Revolut. Therefore, I do see potential risk if Nu spreads itself too thinly.

Then again, there are almost 70m Latinos in America, so the long-term growth opportunity could be substantial. Management has proven itself highly capable of identifying such growth opportunities, so I’m happy to give the benefit of the doubt.

Valuation?

Turning to valuation, Nu is trading at 3.5 times forward sales and 21.5 times forward earnings. To me, these don’t look like high multiples for a world-class growth company scaling profits rapidly.

The price/earnings-to-growth (PEG) ratio is just under 0.5. Remember, anything below one is often considered potentially undervalued.

Final thoughts

Summing up then, Nu has top-class management, excellent profitability, and big future growth potential. It’s also very innovative, constantly rolling out new products and services, and is deepening adoption of AI.

In a few years’ time, I think Nu stock could look like a steal at $15. As such, this is one I’m looking to add to in the coming weeks.