With its attractive tax breaks and flexibility over the types of investments that can be held, a Self-Invested Personal Pension (SIPP) is a great way to save for retirement.

With this in mind, I think it’s possible to build a pension pot worth a cool £175,000 using a handful of dividend shares. Let me explain.

Please note that tax treatment depends on the individual circumstances of each client and may be subject to change in future. The content in this article is provided for information purposes only. It is not intended to be, neither does it constitute, any form of tax advice. Readers are responsible for carrying out their own due diligence and for obtaining professional advice before making any investment decisions.

Crunching the numbers

At an annual growth rate of 5%, someone investing £300 a month for 25 years could build a retirement pot worth £176,436. Obviously, investing more for longer is likely to yield a better return.

However, if someone was able to supplement their monthly investment with an initial lump sum of £20,000, the end result would be even more impressive. In this scenario, it would be possible to build a SIPP valued at £244,163 after 25 years. Again, this assumes a 5% return each year.

| Monthly investment (£) | SIPP value with no lump sum (£) | SIPP value with £20,000 lump sum (£) |

|---|---|---|

| 100 | 58,812 | 126,539 |

| 200 | 117,624 | 185,351 |

| 300 | 176,436 | 244,163 |

| 400 | 235,248 | 302,975 |

| 500 | 294,060 | 361,787 |

Whether an individual achieves a 5% return from growth shares — or reinvests the dividends from income stocks paying 5% — the end result will be the same.

And there are plenty of dividend-paying shares offering a similar return at the moment (19 April). The table below includes five from the FTSE 100, the UK’s premier index of listed companies.

| Stock | Sector | Yield (%) |

|---|---|---|

| Imperial Brands | Tobacco | 5.5 |

| NatWest Group | Banking | 5.2 |

| Persimmon (LSE:PSN) | Construction | 5.2 |

| Admiral Group | Insurance | 4.8 |

| BP | Energy | 4.3 |

| Average | 5.0 |

I would have to do more research before deciding whether all of them are worth considering but, remember, this list of high-yielding shares isn’t exhaustive. There are plenty of others available at the moment.

The biggest and best?

In theory, FTSE 100 stocks are the most likely to deliver reliable earnings growth. In turn, this means their dividends are probably going to be more sustainable and predictable. Of course, there are never any guarantees when it comes to investing in the stock market. However, history suggests that the UK’s largest companies are among the world’s most reliable when it comes to dividends.

One stock in the table — and a company that has a long history of returning a large proportion of its earnings to shareholders — is Persimmon, the FTSE 100 housebuilder.

As a result of the pandemic and partly due to the impact that post-Covid construction cost inflation had on its margin, it had to cut its dividend. But based on amounts paid over the past 12 months, new investors could enjoy a yield of 5.2%.

Green shoots

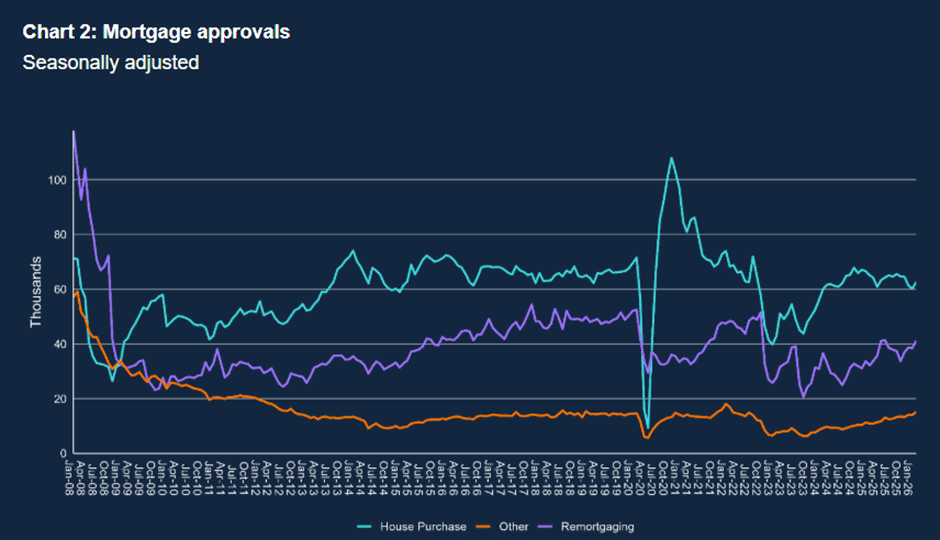

Although the UK housing market has been in the doldrums lately, there are signs things are slowly recovering. The latest analysis from the Bank of England shows a steady improvement in mortgage approvals.

And until Iran was attacked, most economists were expecting the next movement in interest rates to be a downwards one. Assuming the current ceasefire in the Middle East holds, the market should continue its recovery, albeit after– perhaps — a temporary setback.

Presently, there’s a shortage of housing in the UK and recent changes to planning law should make it easier to address this under-supply. And with its houses being cheaper than most of its peers, Persimmon could be one of the biggest winners.

This should help the group expand once more and enable it to raise its dividend again. Its debt-free balance sheet also means it can use more of its operating cash to reward shareholders.

Personally, I think Persimmon’s worth considering as part of a diversified portfolio. In fact, I hold it in my own.