A penny stock trading at 58.5p with deep exposure to the global defence boom isn’t the kind of thing that stays hidden for long. It’s has, unsurprisingly given the recent context, been performing rather well. The stock’s up around 40% over the past six months.

But could it go further? Let’s explore.

Who is it?

MTI Wireless Edge (LSE:MWE) has the hallmarks of a quality stock. It’s an Israel-based specialist in military antennas, 5G backhaul, and water solutions — and a confluence of catalysts may be aligning in its favour.

The company just posted record full-year results for 2025. Revenue rose 13% to $51.5m with profit from operations up 29% and earnings per share climbing 18% to 5.83 cents.

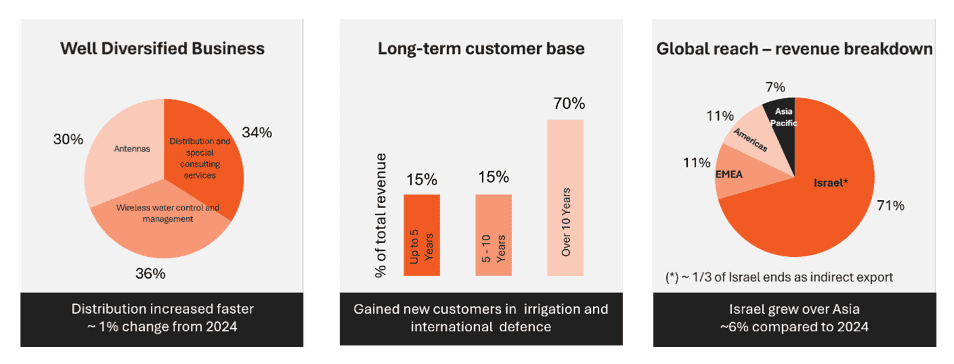

All three divisions — antennas, distribution and consulting, and water solutions — delivered double-digit revenue growth, with the antenna division leading at 23%, driven by surging demand for military-grade hardware and 5G infrastructure.

It also appears well diversified and benefits from long-term contract lock-ins.

What’s more, the balance sheet’s clean. MTI sits on $9.55m in cash with no meaningful debt, giving it a net cash position. Return on capital is 17.1%, return on equity 17%, and the stock trades on a forward price-to-earnings of just 13.3 with a forecast dividend yield of 4.66%.

More wins

This week, the company announced multiple new defence contract wins worth around $6m. That’s more more than 10% of its entire 2025 revenue. The deal includes a $2.2m communications infrastructure contract for the Israeli Ministry of Defence (MoD) and $1.9m in military antenna orders from an international defence contractor.

All orders are scheduled for delivery across 2026 and 2027.

2 bullish analysts and positive signs

When it comes to penny stocks, there isn’t much institutional coverage. In other words, there aren’t many analysts covering the stock. However, the two that do cover MTI are very bullish. Collectively, their price target’s 62% above the current share price.

Moreover, consensus forecasts point to net profit of $5m in 2026 and $5.21m in 2027. Notably, the Beer family — substantial shareholders — bought 600,000 shares at 53.5p as recently as 26 March, a vote of confidence from insiders.

Then there’s the geopolitical backdrop. The Iran-US ceasefire agreement reached on 7 April could materially re-rate Israeli equities. Throughout the conflict, Israeli-listed and Israel-based stocks traded at a persistent-risk discount.

A sustained ceasefire — and the permanent reopening of the Strait of Hormuz — may unlock institutional capital that has been sitting on the sidelines.

The bottom line

That said, there are risks to bear in mind. MTI’s a tiny company and the free float (51%) is limited. What’s more, liquidity may be limited and the the bid-ask spread sits at 513 basis points.

And while the business is diversified across segments, the company’s reliance on Israeli MoD contracts introduces concentration risk.

However, for investors willing to accept that risk, it may be worth considering.