No savings at 40? Just £5 a day in an ISA could deliver a £16k second retirement income

I’m investing in a Stocks and Shares ISA to make a second income for retirement. The UK is facing a double-whammy of a soaring elderly population and surging public debts. In this climate, I’m not taking any chances and betting on the State Pension alone to fund my lifestyle.The good news is the stock market’s been delivering excellent returns for decades.

Over the long term, a share investor can expect an average annual return of roughly 9%. That’s based on capital gains of 6% and dividend income of 3%. At this rate, even those in middle age with £0 put aside can generate enough cash to fund a comfortable retirement.

Want to know how? Read on.

Targeting a £16k income

I love the idea of dividend investing. Right now, I invest any cash payouts in my Stocks and Shares ISA back into the market, speeding up my portfolio’s growth. When I retire, I plan to use those dividends supplement my State Pension and hit my financial goals.

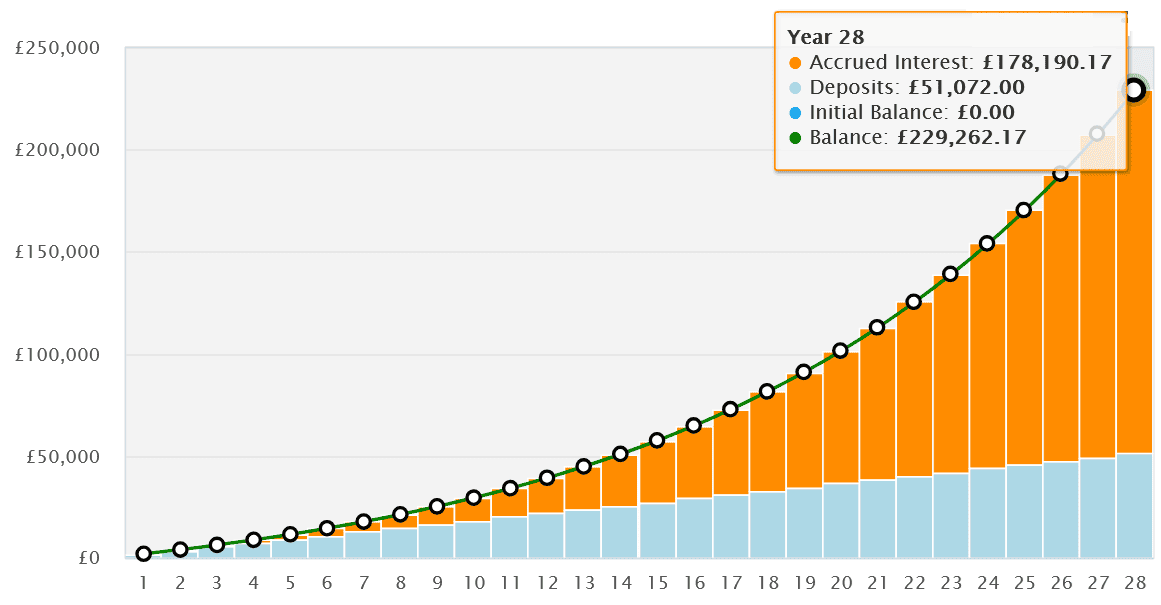

Now imagine we have a 40-year-old investor following the same strategy. How much would they need to invest for a large passive income stream by the time they hit 68?

They certainly wouldn’t need to set aside huge sums of money. Let’s say our investor puts £5 a day into their ISA, which works out at £152 a month. That isn’t the largest amount, so they choose an account with zero trading fees and low running costs to protect their investing power.

If they can hit a 9% average annual return, they would — after 28 years, and with dividends reinvested — have a nest egg of £229,262. If they then switched their ISA portfolio into 7%-yielding dividend shares, they’d have a healthy £16,048 income stream to fund their retirement, tax free.

Please note that tax treatment depends on the individual circumstances of each client and may be subject to change in future. The content in this article is provided for information purposes only. It is not intended to be, neither does it constitute, any form of tax advice. Readers are responsible for carrying out their own due diligence and for obtaining professional advice before making any investment decisions.

A top dividend share

Dividends are never guaranteed. But the UK’s stock market has a deep pool of quality, high-yield income shares investors can choose from. With a diversified portfolio of these, retirees have a brilliant chance of earning a substantial second income.

Primary Health Properties (LSE:PHP) could be a perfect share to consider for a strong dividend portfolio. You might not have heard of it, but you may have been in one of its buildings. It operates 1,142 healthcare centres across the UK and Ireland such as GP surgeries.

What makes the firm a dividend winner is its focus on a defensive industry that’s immune to economic downturns. It’s grown annual dividends consistently since the late 1990s, and is tipped by City analysts to keep doing so. This leaves an enormous 8% dividend yield for 2026.

So what are the risks of buying Primary Health shares? Well if interest rates rise as expected, its net asset values and borrowing costs will be negatively affected. In this climate, its share price might decline.

On the plus side, the firm will almost certainly continue paying a large and growing dividend in the near term. And as Britain’s booming population drives healthcare services demand, I expect both the share price and dividends to grow over time.