The Helium One Global (LSE:HE1) share price is on fire at the moment. At the time of writing (20 February), the stock’s changing hands for over 40% more than it was a month ago.

What’s causing this sudden interest in the relatively unknown gas explorer? Let’s take a closer look.

A finger in two pies

Helium One has two projects on the go.

The most advanced is its Galactica-Pegasus joint venture in Colorado. And this appears to be the catalyst for much of the £19m increase in the group’s market cap over the past four weeks or so.

The company recently said that “integrated plant operations” have been scheduled for the end of the month as it gears up for production later in the year. Significantly, it also said: “Arrangements have been made for spot sales of helium and discussions in respect of long-term contracts with both helium and CO2 off-takers are progressing.”

But this is a relatively small operation. In March 2025, the group said it expects “an average of approximately US$2m per annum will accrue to the company over a period of five years.” This is a revenue figure, not profit. For context, during the year ended 30 June 2025, the group’s total administrative expenses were $4.1m.

However, the estimate excludes any benefit from the sale of carbon dioxide (CO2). And there could be further undiscovered deposits of both gases.

But I suspect shareholders believe a potentially bigger prize lies elsewhere.

Miles away

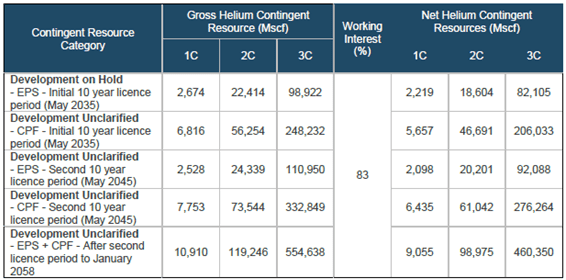

That’s because the group owns 83% of the Southern Rukwa Project in Tanzania.

Here, further testing using an electrical submersible pump has resulted in water flow rates “exceeding expectations”. This is important because the helium isn’t conventional dry gas. Instead, it’s found in water aquifers, which the group acknowledges is “unique”. And I think this casts some doubt on its recoverability.

However, if it’s able to overcome this challenge, there’s enormous potential according to an independent estimate of reserves. But given the uncertainty typical of the industry, it’s normal to quote a wide range of figures.

For context, although there isn’t a spot price for the gas, I’ve seen reports suggesting helium sells for up to $1,000 per thousand standard cubic feet depending on its grade. Due to its special characteristics, in particular its cooling properties, demand for helium is rising, which could drive prices higher.

The last time I wrote about Helium One I was contacted by an industry expert claiming that it’s not “technically or financially possible” to transport compressed helium by sea from Africa using ISO tanks. I put this to a representative of the company who agreed. But they told me that “helium can also be transported as a compressed gas in tube trailers by ship”.

No thanks!

But I don’t want to invest.

The company says around $100m will be needed to commercialise production. I suspect shareholders will, therefore, be further diluted. This isn’t a criticism. It’s a fact of life for pre-revenue companies. From June 2020 to June 2025, Helium One increased its number of shares in issue by over 6bn (3,417%).

There are loads of mining companies that are already successfully producing and, more importantly, fully funded. On this basis, I think there are less risky opportunities to consider elsewhere.