It stands to reason that those looking to earn passive income should buy stocks paying generous dividends, right? Not necessarily. Sometimes, a share with a high yield can be a bit of a value trap. In other words, something’s too good to be true.

But I’ve found one where I don’t think this is the case. In fact, I believe there’s a good chance it will be able to increase its dividend further. Let’s take a closer look.

Pole position

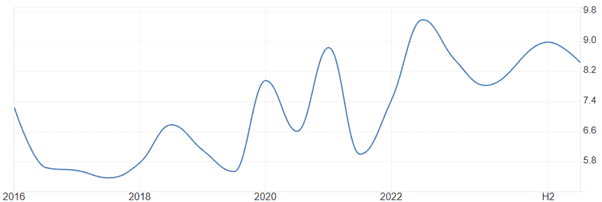

With a yield of 8%, Legal & General‘s (LSE:LGEN) currently (13 February) offering the best return on the FTSE 100. Admittedly, some of this can be attributed to a falling share price, a classic sign of a value trap. However, as the graph below shows, for the past decade, the stock’s always offered an above-average yield.

And I think it’s likely to be maintained. My optimism is based on strong fundamentals in each of the three markets that it operates.

Right place, right time

Its Institutional Retirement division takes on the management of third-party pension schemes. Higher interest rates have helped many defined contribution schemes move from deficit into surplus. Trustees are now taking advantage of the improved financial position by offloading these (de-risking) to big pension providers.

The group’s Asset Management business is one of Europe’s largest with over £1.1trn of funds. And with more people looking to utilise their spare cash better, there’s plenty of scope for further expansion.

Finally, its Retail arm, which provides savings, protection, mortgage, and retirement products, has over 14m customers and is the UK’s leading provider of annuities. With an ageing population and the state pension age set to rise further, I reckon more people are going to take an active interest in managing their own retirement planning.

And this potential is underpinned by a strong balance sheet. At 30 June 2025, Legal & General had a solvency II ratio of 217%, comfortably above the 100% minimum.

Remember the risks

However, the group still faces some challenges. Competition’s fierce with new entrants offering incentives for customers to switch providers.

And like the rest of us who invest in the stock market, the group’s vulnerable to a correction or, worse, a full-blown crash. At 30 June 2025, it owned nearly £210bn of equities and needs this portfolio to help meet its obligations to customers.

A positive outlook

Earlier this month, the group announced the sale of its US insurance business for £2.3bn. From these proceeds, £1bn will be used to repurchase the group’s shares in 2026. This is equivalent to just under 7% of Legal & General’s current market-cap.

And although there are no guarantees when it comes to payouts, the group’s directors have pledged to increase the dividend by 2% a year from 2025-2027.

In my opinion, Legal & General’s in excellent financial shape, which puts the group in a good position to further increase its above-average dividend. But I suspect the group’s amazing yield might not be on offer for much longer, not because of a threat to its payout but, rather, due to its share price starting to recover after a few years in the doldrums.

One of the best? Well, that’s very subjective. But I reckon Legal & General’s a stock to consider.