Since its launch in January 1984, the FTSE 100 index has delivered a return that comfortably beats anything on offer from a high-interest savings account.

But for an inexperienced investor with some cash to spare, the stock market can be a daunting place. Fortunately, the outlook for UK shares is promising and there’s some speculation that the Footsie could reach 11,000 this year. Let’s see what’s going on.

What next?

As home to plenty of miners and banking stocks, the FTSE 100’s benefitted from rising precious metals prices and renewed confidence in financial services.

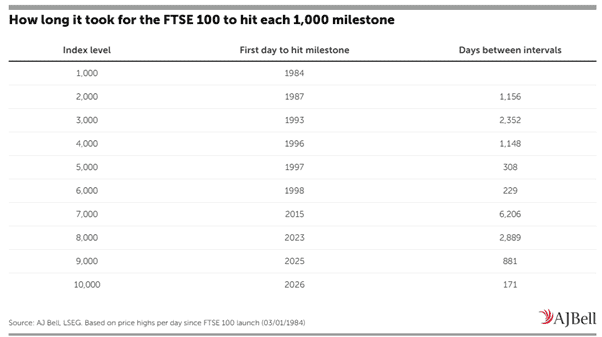

In January, the index reached 10,000 for the first time, just 171 days after hitting 9,000. As the table below shows, this was the shortest time taken to record an increment of 1,000 points.

And it’s now (9 February) at 10,370. Given current global economic uncertainty, the 11,000 mark might be a bit of a stretch this year. But I’m confident the index will get there in the not-too-distant future.

It pays to shop around

However, I still think there are some bargains to be found.

For example, JD Sports Fashion, easyJet, and International Consolidated Airlines, are currently trading at historically low earnings multiples.

Looking at its balance sheet, Barclays has a price-to-book ratio of less than one.

And income investors are likely to be interested in the attractive yields currently on offer from, among others, Legal & General (8.1%), Phoenix Group Holdings (7.3%), and M&G (6.6%).

Okay, I need to do a bit more research before deciding whether these are worth considering. However, these valuation measures suggest that despite the Footsie’s amazing performance over the past year or so, there are still plenty of opportunities out there.

Out of favour

One stock with a vested interest in the FTSE 100 is London Stock Exchange Group (LSE:LSEG), the business that — in addition to providing specialist data and risk management services — oversees the index.

It attracted my attention on 3 February when its share price fell 12.8%. It was caught in the sell-off of software and data stocks following news that Anthropic had launched an artificial intelligence (AI) tool that could threaten the dominance of some of the more established players in the market.

Fears about the emergence of possible challengers appear to be behind the 37% decline in LSEG’s share price since February 2025.

Personally, I think investors are over-reacting. To be effective, AI needs data and LSEG has huge volumes of it. Of course, I could be wrong. Nobody knows for sure how AI’s going to change the world. But I see the group as being one of the net beneficiaries. Although, like all companies in the sector, I think a cyberattack remains a real possibility.

Analysts appear to agree with my assessment of last week’s events. UBS described the share price fall as “overblown”. It has a 12-month target that’s over 50% higher than today’s price. The City consensus is that the stock’s 58% undervalued, although to be fair, these targets were set before Anthropic’s announcement.

But I think the stock’s cheap. It trades on a historically-attractive forward (2027) price-to-earnings ratio of just 14.5.

On balance, I think LSEG’s shares are worth considering. However, it’s just one of a number of undervalued stocks on the index that I think deserve further investigation by value investors.