Want to give yourself the best chance of earning a large passive income? In my view, buying a diversified selection of top dividend shares could be the best way to go.

In theory, passive income investing is as simple as picking dividend stocks to buy and watching the cash flow in once you’ve added them. The reality is it takes some shrewd planning to make a large and lasting dividend stream that lasts years.

Want to know how to maximise your chances of retiring in comfort? Here are five key steps to setting up a robust second income plan.

1. Axe the tax

One of the most important things to think about is tax, and how cash grabs from HMRC can reduce your returns. This is why the Stocks and Shares ISA can be so important. With these accounts, investors are protected from capital gains tax and dividend tax, which can significantly boost long-term portfolio growth.

As well, any withdrawals made from an ISA are exempt from income tax, so every penny you make is yours. Self-Invested Personal Pensions (SIPPs) are also great products, though income tax is charged on drawdowns.

Please note that tax treatment depends on the individual circumstances of each client and may be subject to change in future. The content in this article is provided for information purposes only. It is not intended to be, neither does it constitute, any form of tax advice. Readers are responsible for carrying out their own due diligence and for obtaining professional advice before making any investment decisions.

2. Start building a portfolio

With your investment account opened, it’s time to think about which stocks to buy. One that I think investors should consider right now is M&G (LSE:MNG).

The financial services provider has a 6.9% dividend yield, which is the fourth highest on the FTSE 100. Since being spun out of Prudential in 2019, dividends have risen every year, leading to a yield that’s long trumped the market average.

Can M&G shares keep producing the goods, though? I’m confident they can, though the ultra competitive market the firm operates in poses obvious risks. I’m expecting profits and dividends to continue rising as demographic changes drive market growth, boosting demand for its investment and retirement products.

M&G’s strong balance sheet also gives it strength to weather earnings volatility and keep paying large dividends. Its Solvency II capital ratio was last at a robust 230%, according to latest financials.

3. Mix growth with dividends

As I mentioned, UK investors tend to favour buying dividend stocks. But the most successful strategies include a healthy blend of both growth and income shares.

Growth companies drive long-term capital appreciation, while dividend payers provide dependable cash flows and a smoother return during volatile periods. Blending the two creates a more resilient portfolio and one that delivers across the economic cycle.

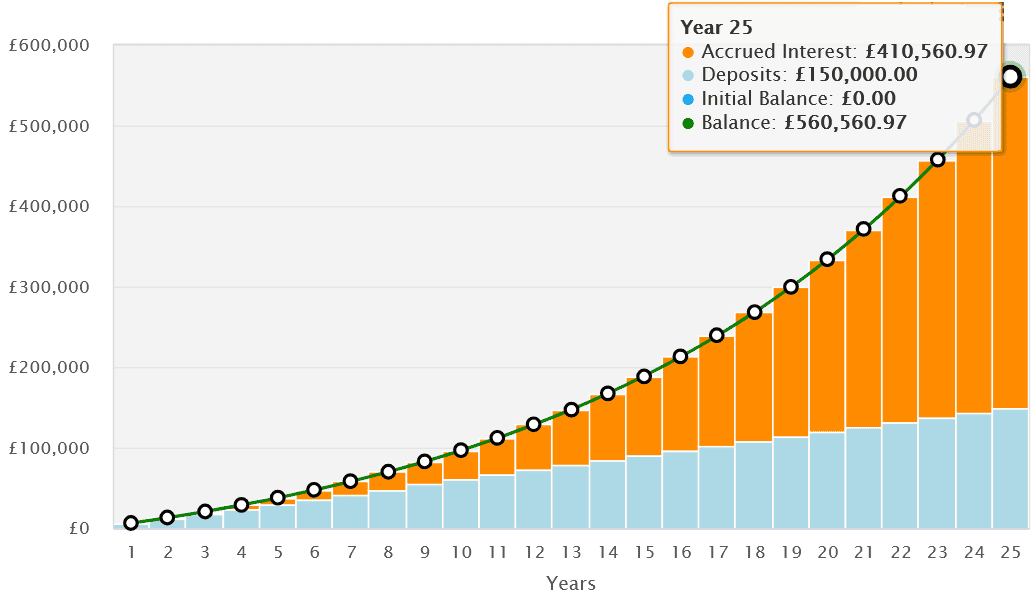

Let’s say someone can invest £500 a month in the global stock market for 25 years. Based on the average long-term return of 9% a year — comprising 6% capital growth and 3% in dividends — they could expect to turn that into £560,560.

4. Watch the income flow!

There are many ways investors can then draw down cash from their investments. My own plan is to rotate my portfolio into dividend shares, allowing room for further portfolio growth while still delivering a brilliant second income.

If I invested a £560,560 nest egg into 8%-yielding dividend shares, I could earn a regular monthly passive income of £3,737. Sounds great, right?