The Lloyds Banking Group (LSE:LLOY) share price has gone from 55.04p to 97p in 2025. But the next question for investors is how much further it can run in 2026.

A similar move again next year would see the stock reach £1.30. Interest rates might be set to come down, but there are still reasons for investors to be optimistic.

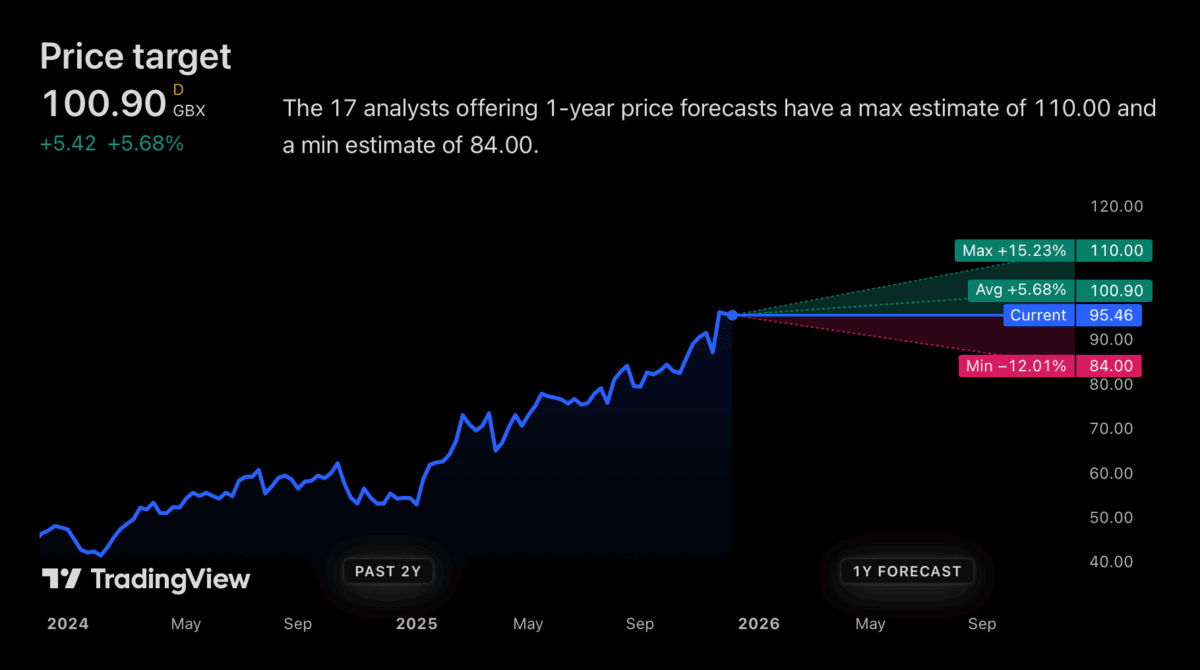

Price targets

From what I can see, the analyst community isn’t expecting a repeat performance from Lloyds in 2026. The highest price target is around £1.10 – 16% above the current level.

Source: TradingView

That wouldn’t be a bad result at all – it’s well above the FTSE 100 average. But the less optimistic forecasts are projecting a share price decline of as much as 12%.

There are good reasons for thinking that 2026 won’t be such a strong year for the stock. The most obvious is the chance of lower interest rates, which would be likely to affect lending margins.

Despite this, though, there are also reasons for optimism. With a bank the size of Lloyds, it’s not as straightforward as the company’s profits falling if interest rates get cut.

Structural hedge

Like a number of banks, Lloyds uses what’s known as a structural hedge. This is essentially a combination of fixed-rate assets (such as bonds) with long durations and interest rate swaps.

These help protect the bank in the short term if interest rates fall. In other words, interest rate cuts in 2026 shouldn’t mean the firm’s income falls away immediately.

In fact, lower rates might mean better margins in 2026. If the bank can reduce the interest on its savings instantly while mortgage rates remain fixed, this could give lending profits a boost.

Higher rates are likely to benefit Lloyds over the medium term. But I don’t think investors should take the view that cuts in 2026 will immediately send the firm’s income into reverse.

Regulations

Looking beyond 2026, there are also more reasons for Lloyds shareholders to be positive. One is the potential for looser regulation giving the bank more scope to lend.

For the first time in 10 years, the Bank of England has decided to lower the amount of Tier 1 capital UK banks are required to hold. This is set to come in from January 2027.

That should leave the likes of Lloyds with excess capital that can be used to grow loan books. But it’s worth noting that this will apply to all banks, so competition might increase.

While banks generally maintain capital ratios well above their legal requirements, a lower standard means more scope for lending. And this could help grow profits beyond 2026.

Don’t be too hasty

Lloyds has been one of the best FTSE 100 stocks to own in recent years. And while cyclical forces have been part of this, investors shouldn’t be too quick to write this one off in 2026.

Falling interest rates are likely to present a challenge. But this is the kind of thing the bank should be in a position to deal with – and its structural hedge suggests it is.

Looking further ahead there are reasons to think the stock could be a good investment beyond 2026. But it’s not my top opportunity as the New Year approaches.