Let’s be honest — 2025 hasn’t been the most exciting year for Tesco (LSE: TSCO) shares. The stock’s only up around 23% this year, which hardly sets the market alight. But zoom out to a three-year view and it’s a different story altogether.

Including dividends, Tesco’s delivered a total return of roughly 140% since 2022. That means a £5,000 investment back then would now be worth around £12,000. A £7,000 return in just three years is a decent chunk of passive income by anyone’s standards.

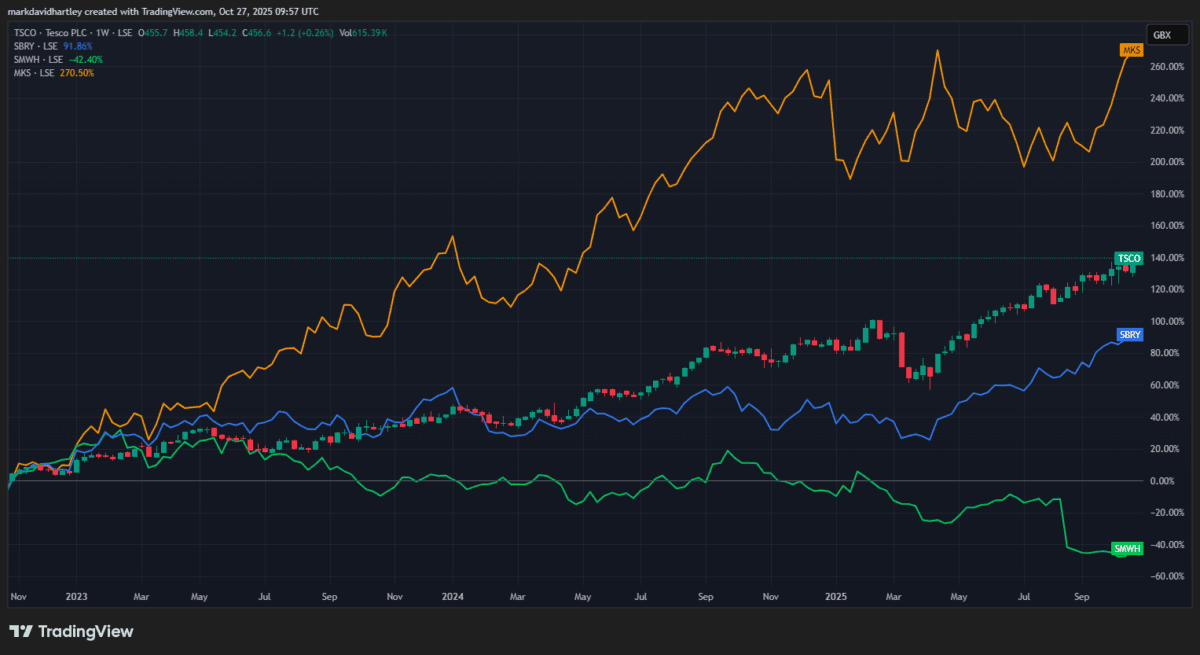

But is the performance above average when compared to other similar shares?

Let’s take a closer look.

Competitors’ performance

When compared to rivals, Tesco’s performance still looks fairly impressive. Its closest competitor, Sainsbury’s, has delivered a total return of only 92% in the past three years. Meanwhile, WH Smith — while not solely a grocer — has suffered a loss of 42%.

But the standout winner in UK retail is Marks and Spencer, returning an eye-watering 270% since October 2022. A £5,000 investment back then would be worth £18,500 today — an almost four-fold return. Of course, the retail giant benefits from a broader selection of products, deriving significant revenue from its clothing, beauty, and home products

Other competitors, such as Asda and Morrisons, are harder to evaluate as they’re owned by private equity firms.So that begs the question — what can investors expect from Tesco shares in the next three years?

The three-year outlook

Looking ahead, analysts expect Tesco’s dividend to rise steadily to around 17.2p per share by 2028, implying a 3.8% yield. Earnings per share (EPS) are forecast to climb to 37p in the same period, while revenue could hit £77.85bn — roughly 10% higher than current levels.

However, despite the steady growth outlook, the average 12-month price target from 16 analysts sits at just 471p. That’s only about 3.3% higher than the current price. Most analysts still give the stock a Buy rating but expectations are clearly modest.

There are a few risks to consider too. Food inflation continues to pressure margins, while low-cost rivals like Aldi and Lidl are capturing more of the budget-conscious shopper segment. Meanwhile, with a forward price-to-earnings (P/E) ratio of around 17, Tesco could already be fully priced for perfection. The dividend yield’s decent, but it’s not especially high compared to other FTSE 100 shares.

That said, the true value of Tesco – and the reason I hold the stock – lies in its defensive strength. The company dominates UK grocery retail, operates on reliable cash flow and serves as a stable hedge against market volatility.

Long story short: people need to eat, regardless of whether the economy’s booming or contracting.

My verdict

Tesco’s growth prospects over the next three years appear modest, and its yield won’t excite income hunters. But it’s still worth considering as part of a diversified portfolio, offering a layer of defensive stability that’s hard to find elsewhere.

For me, it’s not a stock that’ll make anyone rich overnight — but it’s one that helps me sleep well knowing my portfolio has a solid defensive foundation.