Since it was spun off from Prudential in 2019, M&G‘s (LSE:MNG) shares have been an exceptional source of passive income for investors.

Annual dividends have risen every year since then, even during the pandemic. In 2024, cash rewards were lifted 2% to 20.1p per share, beating payout growth across the broader FTSE 100.

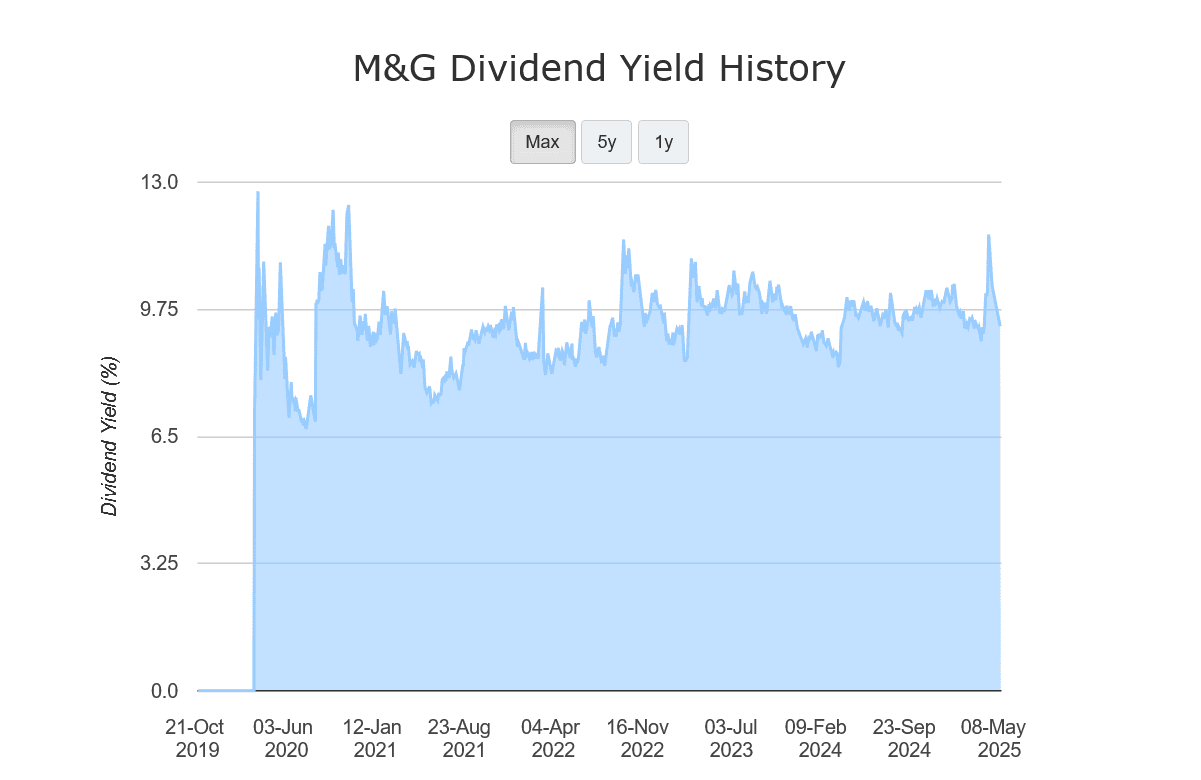

Not only this, but dividend yields for the financial services giant have also comfortably beaten the Footsie’s long-term average (of 3% to 4%) since 2019:

But past performance isn’t always a reliable guide to future returns. And with the global economy softening as trade tariffs bite, M&G’s proud dividend record could experience some squeeze if profits slump.

Here, I’m looking at the City’s dividend forecasts through to 2027. I’m also wondering whether M&G is, on balance, a top FTSE 100 stock to consider.

Double-digit dividend yield

Despite growing macroeconomic uncertainty, forecasters are confident that the FTSE firm will continue delivering generous dividends over the next few years.

Their estimates can be seen below:

| Year | Dividend per share | Dividend growth | Dividend yield |

|---|---|---|---|

| 2025 | 20.6p | 2.5% | 9.4% |

| 2026 | 21.2p | 2.9% | 9.7% |

| 2027 | 22p | 3.8% | 10% |

Firstly, dividend growth is tipped to outstrip the 1.5% to 2% predicted for blue-chip average in the near term. And payout increases are expected to pick up steam over the period.

Secondly, dividend yields are also expected to remain comfortably above the FTSE 100’s historical average.

Yet dividends are never guaranteed, and especially in the current climate. So it’s important to consider how robust these estimates are.

Unfortunately, things aren’t as secure as I’d ideally like, at least based on dividend cover. For the next three years, dividends are covered between 1.2 times and 1.3 times by anticipated earnings. Both figures are below the widely regarded safety benchmark of two times and above.

Should investors buy M&G shares?

Does this make M&G shares a potential dividend trap, then? ‘Not at all’ is my frank opinion.

While higher dividend cover is preferable, the FTSE company’s managed to keep paying large and growing dividends despite previously poor readings (and even periods of losses).

With a strong balance sheet, I’m confident that M&G can meet the City’s healthy dividend projections. Its Solvency II capital ratio was 223% as of December, its robust cash flow driving a 20% year-on-year improvement.

The company’s expecting cash generation to remain robust over the forecast as well. It’s targeted cumulative operating cash generation of £2.7bn through to 2027.

This should give M&G the ammunition to invest for growth alongside paying more large dividends. Given the huge growth potential across its product segments, I’m optimistic this could lead to substantial passive income and share price gains.

All things considered, I think M&G is worth serious attention, and especially at current prices. As well as having those dividend yields, its shares also trade on a low price-to-earnings (P/E) ratio of 9.1 times.