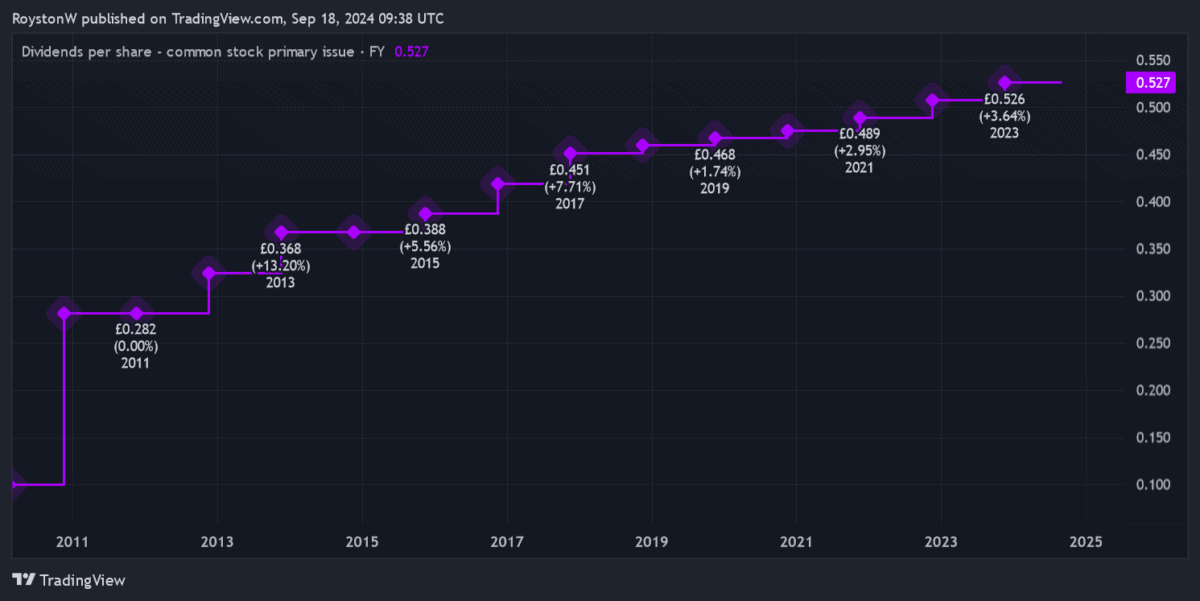

Phoenix Group (LSE:PHNX) has proven to be one of the FTSE 100‘s best dividend shares during the past decade. It even continued to raise shareholder payouts during the Covid-19 crisis when other blue-chip shares were cutting, cancelling and postponing dividends.

The Footsie’s home to many great dividend growth shares. Sage Group, Ashtead Group and Halma are just a few blue-chip stocks with long records of unbroken payout growth.

However, these companies don’t offer the market-mashing dividend yields of Phoenix shares. These eventually rise through 10% over the medium term, as the table below shows.

| Year | Dividend per share | Dividend growth | Dividend yield |

|---|---|---|---|

| 2024 | 54p | 3% | 9.9% |

| 2025 | 55.7p | 3% | 10.2% |

| 2026 | 57.3p | 3% | 10.5% |

The prospect of making a FTSE 100-beating dividend income over the period is tantalising to me. The average forward yield for Footsie share sits way back at 3.5%.

But dividends are never guaranteed, and I need to consider how realistic these forecasts are. I must also consider other factors that impact Phoenix’s investment case. Big dividends might count for nothing if the company’s share price plummets.

Here’s my view of the financial services mammoth.

Bad omen

To be honest, my first take on Phoenix’s dividend prospects isn’t an encouraging one. I’m looking at dividend cover, which indicates how well predicted payouts are covered by expected earnings.

Like dividend forecasts, profits estimates can also miss their mark. So a reading of 2 times and above provides investors with solid protection.

In the case of Phoenix, predicted earnings of 44.9p per share for 2024 are actually lower than the expected dividend per share of 54p.

The relationship switches from next year, but dividend cover of 1 times and 1.1 times for 2025 and 2026, respectively, is far from robust.

Good omen

That said, I wouldn’t say Phoenix’s poor dividend cover is a dealbreaker. Earnings per share have regularly surpassed dividends in recent years, but this hasn’t hampered the company’s ability to pay a huge and growing dividend.

Past performance isn’t a reliable guide of the future. But a glance at Phoenix’s balance sheet fills me with optimism.

As of June, its Solvency II capital ratio was 168%. This was well inside the company’s target of 140% to 180%.

Phoenix is a cash-generating machine. And as a potential investor I’m encouraged by its ability to regularly meet — or even beat — its cash creation targets.

Strong cash generation in the first half, for instance, led the firm to claim “we are confident of delivering at the top-end of our £1.4bn to £1.5bn target range in 2024.”

A top dividend share

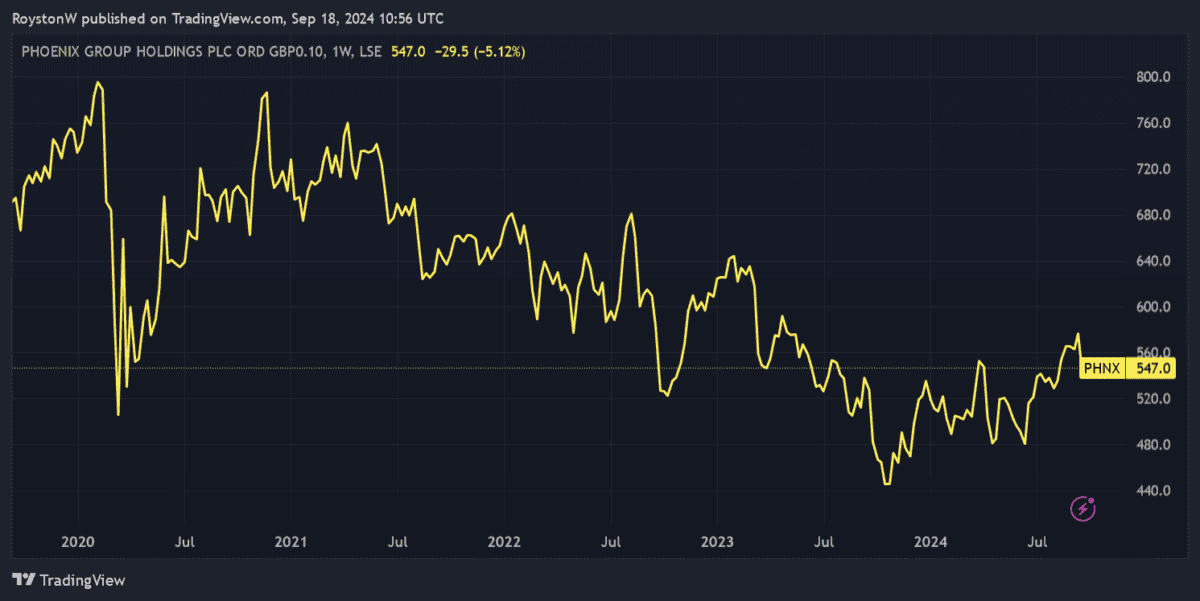

As a consequence, I’m quite upbeat on Phoenix’s dividend forecasts for the next few years. My main concern is whether its share price could struggle through to 2026. Tough economic conditions and the ever-present threat of market volatility could adversely impact the business.

However, as a long-term investor this isn’t a dealbreaker for me. I believe that Phoenix’s share price will rise steadily over time as demographic changes drive demand for retirement products. I actually think it could rise in value as interest rates fall.

And in the meantime, I could look forward to more juicy dividends. This is a share I’ll seriously consider when I next have cash spare to invest.