A 2023 survey shows only 18% of UK residents invest in stocks and shares. This percentage is growing, but still seems low to me. After all, the stock market is probably the best wealth-building tool the average person has access to.

To show how powerful it can be, let me run through an example. Here, I’m going to show how £146 a month invested in UK shares can turn into a yearly second income.

So how do we get started? Well, it’s easier than ever. Gone are the days when investing in a company meant calling a broker and asking for the latest share price of Woolworths.

Nowadays, high street banks and other fintechs offer apps that make it as easy as ordering a Chinese takeaway. I buy shares through an app, it takes me 10 seconds and the fees are a few pounds. Some of the most popular UK options are Hargreaves Lansdown, Trading212, Freetrade and Vanguard.

Using one of these companies, I’d look to open a Stocks and Shares ISA. This account lets smaller investors buy shares without having to worry about HMRC taking a cut. I can deposit up to £20,000 each year, and for anything I withdraw, I get 100% of the money.

Please note that tax treatment depends on the individual circumstances of each client and may be subject to change in future. The content in this article is provided for information purposes only. It is not intended to be, neither does it constitute, any form of tax advice. Readers are responsible for carrying out their own due diligence and for obtaining professional advice before making any investment decisions.

How does it work?

Once I’m up and running, I can start adding money to my ISA from my current account. In this example, I’ll use £146 a month. That’s big enough to target substantial wealth, while small enough to show that I don’t need to be rich already to make investing work.

Next, I start buying shares. I can own them in tons of UK companies, from Greggs to Tesco to Rolls-Royce to J D Wetherspoon. I’d get money back in one of two ways. Firstly, as a dividend payment out of earnings. Secondly, if the share price goes up I can sell shares for a profit.

It’s true that stocks go down and companies cut dividends, which remains a risk. But this kind of volatility is normal. And actually, perhaps the most important tip here is to stay patient when this happens. The easiest way to lose money in stocks is by panic selling at the bottom.

The reason why that’s so bad? In every single crash, correction or recession that has ever happened, the stock market made a recovery. Historically, stocks have returned around 10% a year, and that’s through the 2008 recession, 1989’s Black Monday and even world wars and the great depression.

A £300k nest egg

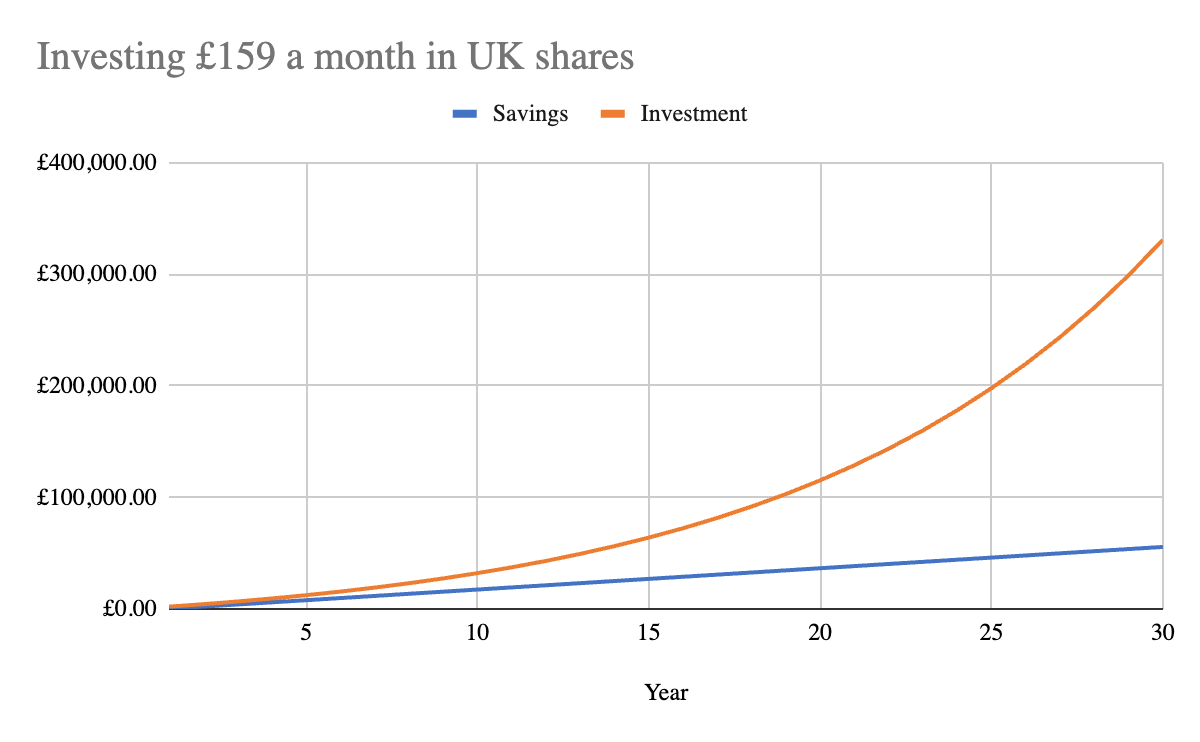

So, now I’m staying the course, buying shares and hopefully getting a 10% average return per year, which isn’t guaranteed, of course. My £146 per month, after 30 years, would grow into £301,175.

A 10% withdrawal from that gives me a second income of £30k. But I’d withdraw less to give myself more safety in keeping my nest egg intact. A 4% withdrawal returns £12k. And I have to remember that both £30k and £12k will be worth less in 2053 than in 2023.

Either way, building up to this amount of wealth sounds almost unbelievable, but it’s just how the compound interest snowballs. Here’s how it looks on a graph, compared to not investing the returns. It’s clear to see just how much of the money is made from the interest building up, and not from the savings I put in.

This is just a brief example, but hopefully shows how I use investing to make my money work for me. I’m partway through my journey to building a second income now, and I will continue investing in UK shares to grow my wealth.