The collapse of Silicon Valley Bank (SVB) has investors running for the hills, fearing a repeat of the 2008 financial crisis. That said, there’s reason to believe that this fear may be overdone, especially with Lloyds (LSE:LLOY) shares, which have dropped almost 10% in a week.

How did SVB collapse?

SVB’s fall started when it opted to invest the bulk of its customers’ deposits into risk-weighted assets, such as long-dated government bonds. These securities are very sensitive to interest rates. Thus, they saw a massive decline in value when the Federal Reserve aggressively raised rates last year.

The lender was then forced to sell those bonds at a huge loss when the majority of its clients in the tech and crypto industry came banging on its door for cash. To put it simply, SVB faced a liquidity crisis in the middle of a bank run.

To mitigate the catastrophe, the board attempted to raise capital via equity. However, this spooked investors and led to more withdrawals. It sent the stock crashing along with many of its peers, such as Silvergate Capital and First Republic Bank, which saw drops of up to 80%.

Can the same happen to Lloyds?

It’s no surprise to see the Lloyds share price drop too as investors fear a contagion event. And while a similar scenario could play out with Lloyds, it’s highly unlikely for several reasons.

Firstly, unlike its US counterpart, the Black Horse bank discloses its liquidity coverage ratio. As of its latest earnings report, this stands at 144%. What’s more, it has a solid CET1 ratio (which compares a bank’s capital against its assets) of 15.1% — much stronger than most other banks.

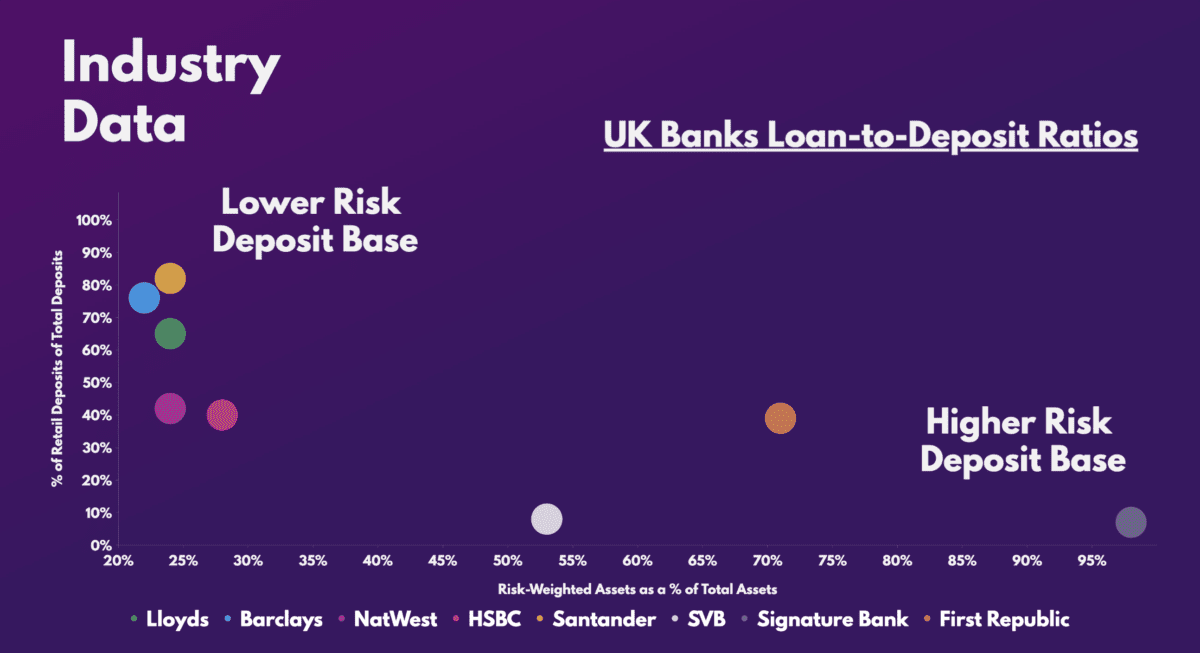

Additionally, investors may find comfort in Lloyds’ in low-risk deposit base. That’s because unlike SVB, the bulk of its clients are retail customers. This means that a bank run is unlikely to test the FTSE 100 stalwart’s liquidity as retail customers don’t tend to hold as much cash as commercial clients.

More importantly, its percentage of risk-weighted assets isn’t nearly as high as its collapsing US counterparts. Pair this with the fact that Lloyds stores a healthy pile of its cash (£9.14bn) with the Bank of England, and it reinforces its margin of safety.

Should I buy Lloyds shares?

Investing in bank stocks carry a high amount of risks. Hence, it’s important to buy shares only in banks with strong fundamentals and a low exposure to risk, especially times like these. Lloyds is one such example.

Given its strong financial footing, and less risky asset base, it seems well equipped to weather the current downturn and a potential contagion event. This sentiment is echoed by the likes of JP Morgan and Liberium, who say that the current decline presents an opportunity for investors.

And when considering its valuation multiples, it certainly seems like it. After all, Citi reiterated its ‘top pick’ rating for the stock, with Goldman Sachs and Barclays also rating the shares a ‘buy’ with an average price target of 75p. This presents a 60% upside from current levels.

| Metrics | Lloyds | Industry average |

|---|---|---|

| Price-to-book (P/B) ratio | 0.7 | 0.7 |

| Price-to-earnings (P/E) ratio | 6.6 | 9.5 |

| Forward price-to-earnings (FP/E) ratio | 6.9 | 8.0 |

So, having considered Lloyds’ financial position and weighing out the risk-reward proposition, I believe the stock’s decline presents a buying opportunity for me. Therefore, I’ll be increasing my position while capitalising on its lucrative dividend yield, which currently sits at 5.1%.