The UK might not be top of mind when looking for growth stocks to buy. After all, barnstorming tech shares such as Nvidia and Palantir are listed across the pond. They’re up 627% and 1,665% respectively in just three years!

However, the UKs home to some cracking, lesser-known growth companies. Here are two I think deserve a closer look today.

Wise

Let’s start with the largest, Wise (LSE:WISE). The international money transfer specialist has a £10.8bn market-cap, but rather than try join the FTSE 100, it’s moving its primary listing to the US.

However, it will keep a secondary listing in London, where each share currently costs 1,050p. This puts the stock on a forward price-to-earnings (P/E) ratio of 26.5.

I don’t think that’s outrageous for a company that did the following last year:

- Grew underlying income 19% on a constant currency basis to £1,619m.

- Increased cross-border volume 25% to £181.7bn.

- Grew customers 21% to 18.9m.

- Guided for pre-tax profit margin to be towards 16%.

Looking ahead, the growth engine still seems very strong to me. As well as people, more businesses are signing up to use Wise, whose infrastructure makes cross-border transactions cheaper and faster. Some 75% of transfers are now instant.

Plus, Wise is lowering the take rate as it scales. While some investors might not like this because it’s sacrificing short-term profitability, it should place Wise in a much stronger competitive position over the long run.

And as a long-term investor, that’s what I’m interested in.

However, in the near term, the situation in the Middle East represents a risk to growth. If soaring inflation and energy costs tip the global economy into a downturn, then it’s possible less people and businesses will move money around.

Despite this risk, I’m happy to have Wise as a top-10 position in my portfolio. The stock’s up 21.5% year to date, but I still think it’s worth considering anywhere near £10.

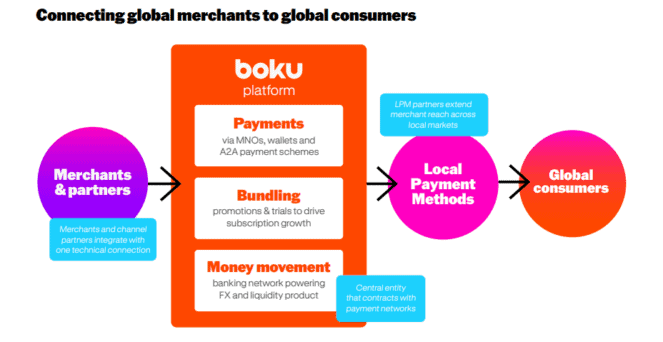

Boku

Turning to Boku (LSE:BOKU) now, this is a much smaller company, with a £525m market-cap. Despite its modest size, Boku works with the world’s largest merchants, helping them drive sales in more than 60 countries through local payment methods (LPMs).

For example, let’s say someone in Thailand wants to subscribe to Netflix. They select their digital wallet as the payment method, and Boku provides the backend piping that connects Netflix with that specific local wallet. Its network now reaches 200+ LPMs, and is growing every year.

Last year, revenue jumped 30% to £129m, up from £62m in 2021. By 2028, analysts expect that to reach more than £210m, with LPMs expected to account for 60% of the $11trn global e-commerce market.

However, Boku isn’t a loss-making fintech. Its profits are growing alongside strong top-line expansion, and management’s confident margins will improve in future years.

The good news is that this earnings growth doesn’t look priced in, with the stock trading at just 18 times next year’s forecast earnings. That’s cheap for a scalable platform that expects to continue growing at 20% over the medium term.

Again, a global economic downturn is a risk, as is competition in the payments space. But I reckon this under-the-radar stock’s worth considering buying for the next five years.