The State Pension currently pays just over £12,547 a year. This is well short of the £38,584 average UK salary based on the latest ONS data.

That gap is exactly why I’ve been thinking about whether an ISA could realistically bridge the difference and turn a basic retirement income into something far more comfortable.

But what would it actually take to bridge that gap in practice?

Asking the right question

Most investors aiming to replace a full salary would likely focus on bridging the £26,037 annual gap in retirement income.

But the challenge isn’t just reaching a target number — it’s understanding both sides of the equation: accumulation and drawdown.

Retirement isn’t just about preserving a pot untouched. It’s about drawing an income that keeps pace with rising costs, without running the portfolio down too quickly. That’s why portfolio construction matters across an investor’s lifetime.

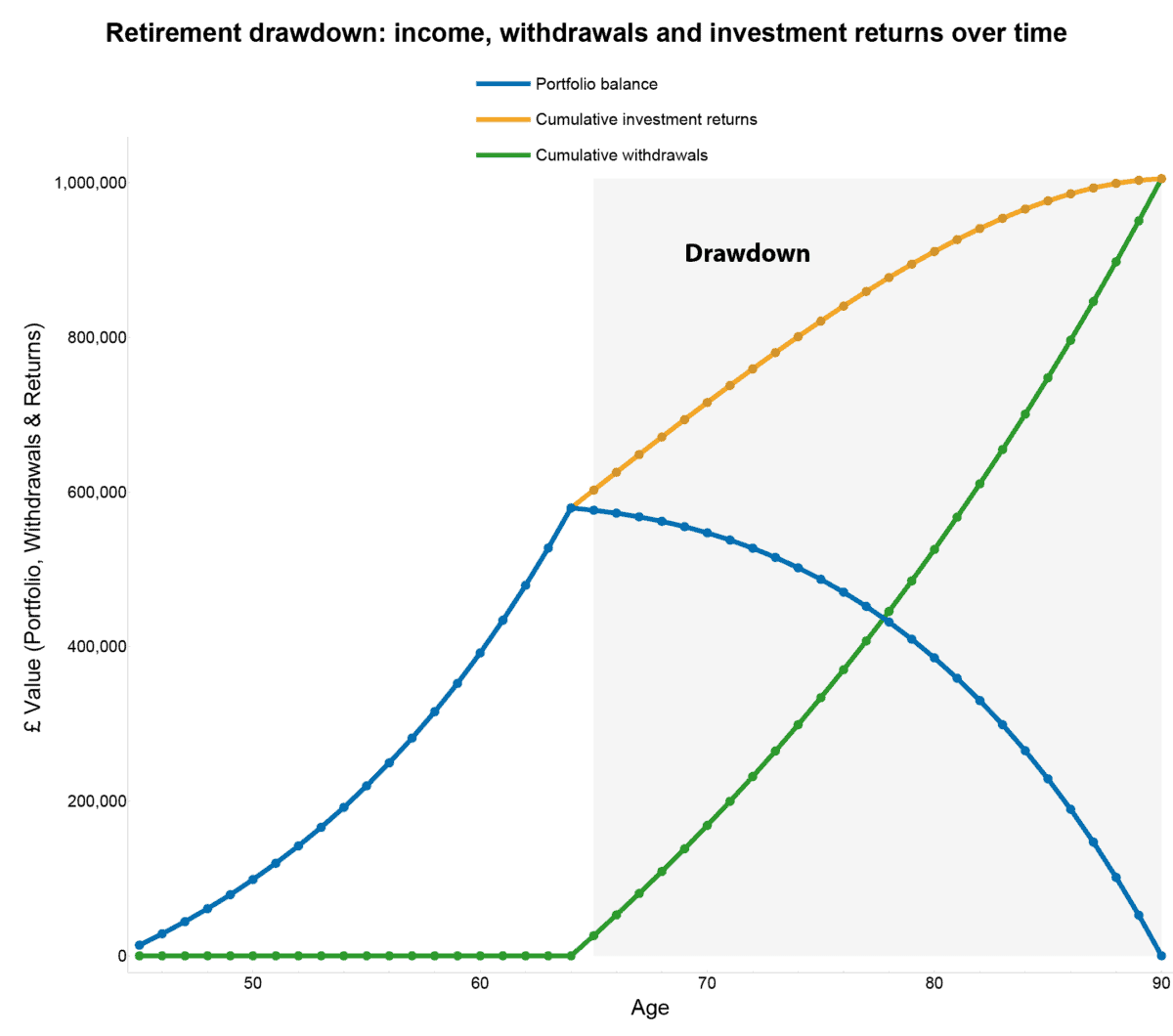

Crunching the numbers

Based on a conservative 4% annual return in retirement and 3% inflation, the model suggests the need for a portfolio of around £578,388 at age 65.

This would be sufficient to sustain withdrawals of £26,037 a year through to age 90.

That’s what the chart below is showing.

The blue line shows the portfolio value over time as withdrawals reduce the balance. In reality, outcomes would be more volatile than this smooth path suggests, as returns and inflation rarely move in straight lines.

What stands out is that even as withdrawals reduce the portfolio, it continues to generate returns throughout retirement. This is reflected in the gold line on the chart, which shows how ongoing compounding keeps the curve from flattening too quickly. It’s a reminder that maintaining a healthy portfolio in retirement matters just as much as during accumulation.

Chart generated by author

Sustainable dividend

Building on that point, Legal & General (LSE: LGEN) stands out to me not because of its headline yield, but because its business model is built around exactly this kind of long-term compounding cash generation.

The group operates across pension risk transfer, annuities, and asset management — all areas that generate recurring, relatively predictable cash flows over long time horizons. That consistency is reflected in its dividend track record. Since 2008, the dividend has only been cut once, during the Covid period.

FY25 results underlined that resilience. Core operating earnings per share rose 9%, sitting at the top end of its long-term growth target range, while the Solvency II coverage ratio remained strong at 203%. The group also returned significant capital to shareholders through buybacks alongside its dividend policy.

For investors thinking in terms of an ISA generating long-term income, this combination of earnings visibility and capital returns is more relevant than headline yield alone. It’s less about maximising income today, and more about sustaining and gradually compounding it over time.

Of course, risks remain. The group is still exposed to movements in bond markets and broader financial conditions, which can affect both asset valuations and profitability. A prolonged period of market stress could also reduce fee income and impact returns.

Even so, the appeal is straightforward: a business designed to convert long-term financial flows into steady shareholder returns. That’s why I hold it, and why I think it’s one investors could consider, regardless of where they are in their investment journey.