Like so many others, Lloyds Banking Group (LSE:LLOY) shares have suffered in the wake of recent events in the Middle East. However, the bank’s share price was falling before the first shots were fired.

The recent drop means the stock’s now (10 April) changing hands for 12% less than it was in early February. Is now a great opportunity to buy in to a quality company at a knock-down price? Let’s see.

Healthy forecasts

With nearly all of the bank’s earnings coming from the UK, I think the investment case largely rests on how an investor sees the domestic economy performing.

Even if it’s only able to grow modestly, this should be sufficient to avoid increasing loan defaults, an ever-present threat that Lloyds faces. And if GDP does go in the right direction, it’s likely to lead to improved business sentiment and an increase in the demand for new loans.

Looking at analysts’ forecasts, it appears as though they have great confidence in the bank and the UK economy in general.

In 2025, Lloyds reported earnings per share (EPS) of 7p. For 2028, the consensus is 12.8p. That’s a massive 83% improvement over three years. This isn’t typical of a business that’s been around since 1765.

Some of the increase is due to an expected £8.7bn of share buybacks. This will significantly reduce the number of shares in circulation. Even so, post-tax earnings are forecast to rise by an impressive 58%.

A different perspective

These City forecasts are critical because, in my opinion, they turn the bank’s valuation on its head.

At the moment, the stock trades on 14.3 times historic earnings. This means it’s the most expensive of the FTSE 100’s five banks. But if the 2028 predictions prove correct, this drops to a much more attractive 7.8, albeit not a bargain. A price-to-earnings ratio of nine is roughly where the world’s retail banks sit.

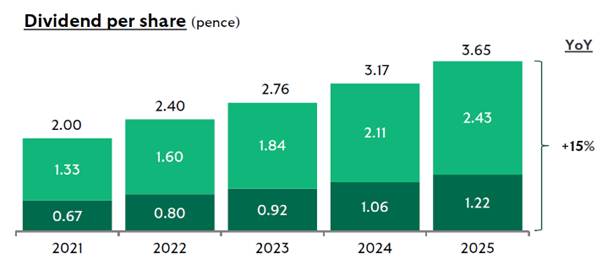

The stock also has an excellent reputation for increasing its dividend. For 2025, its declared payout was 83% higher than in 2021. Analysts are expecting a 58% increase over the next three years to 5.77p. This implies an above-average forward yield of 5.8%.

In summary, what’s not to like about Lloyds?

Not for me

Well, if I thought these forecasts were going to be met I would agree that the bank’s shares offer good value. But these predictions feel a little optimistic to me.

The EPS growth assumes a big improvement in the net interest margin. This is despite banking becoming an increasingly competitive industry. Also, an 11.4 percentage point reduction in Lloyds’ cost-to-income ratio is predicted. I’m sure artificial intelligence will lead to some efficiencies but such a big drop seems like a bit of a stretch to me.

Fears have also been raised about possible contagion in the mainstream banking sector from a deterioration in private credit markets. According to the International Monetary Fund, more than 40% of companies borrowing from private lenders have negative free operating cash flow.

In my opinion, investors have already priced in much of the anticipated earnings improvement long before there’s evidence that it can be realised. For this reason, I think there are better opportunities to consider elsewhere in the sector and beyond.