Market panic typically sees quality passive income stocks plummet alongside more vulnerable dividend shares. This is certainly the case with Primary Health Properties (LSE:PHP), whose share price has slumped 11% in just one month.

In my view, this represents one of the stock market’s best dip buying opportunities to consider. A £5,000 lump sum invested today buys 5,411 shares in the FTSE 250 company. With recent price weakness boosting the dividend yield to 8%, income investors could secure a £400 second income this year alone.

I expect it to remain an excellent dividend provider for decades to come.

Please note that tax treatment depends on the individual circumstances of each client and may be subject to change in future. The content in this article is provided for information purposes only. It is not intended to be, neither does it constitute, any form of tax advice. Readers are responsible for carrying out their own due diligence and for obtaining professional advice before making any investment decisions.

Huge dividend yields

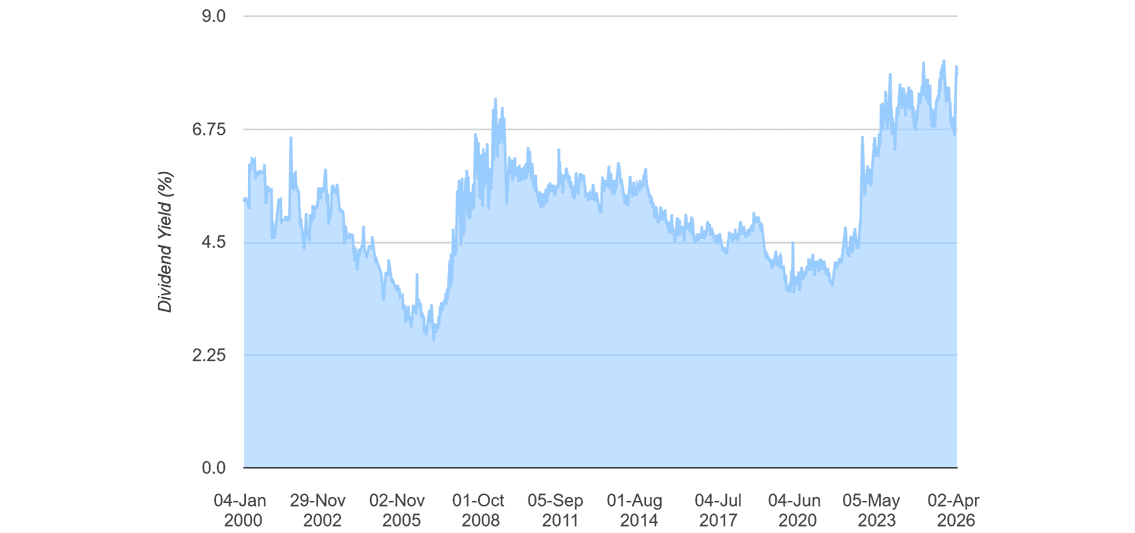

You see, Primary Health Properties’ dividends have risen every year since the mid-1990s. Furthermore, they’ve grown by an impressive 8% on average over the period, meaning dividend yields have averaged 5.1%.

That’s above the FTSE 100 long-term average of 3% to 4%. This in part reflects the defensive nature of its operations — doctors remain in consistently high demand, eliminating problems such as poor rent collection and properties lying empty.

Yet past performance isn’t always a reliable indicator of future returns. So why am I confident the real estate investment trust (REIT) can keep delivering growing dividends?

One major reason is the enormous structural opportunity it enjoys. In a nutshell, demand for healthcare services is rising sharply as the UK population booms. Not only that, but the number of elderly people in particular is growing at breakneck pace, a demographic whose medical needs are naturally high.

Against this backcloth, spending on new GP surgeries, diagnostic centres, and the like, along with updating existing facilities, is tipped to rise strongly. Last year, the government launched its first national capital fund for primary care estates since 2020, underlining the urgent need for investment, with the number of over-65s tipped to rise 20% during the next decade.

What’s the catch?

So if Primary Health Properties is so robust, why has its share price slumped, you ask? It comes down to interest rate expectations. Following recent conflict in Iran, expectations of rate cuts by the Bank of England are in tatters. Markets are now pricing in two rate hikes in 2026, in fact.

This creates a problem for REITs, by depressing asset values and driving up borrowing costs. This is troubling for the firm, whose debt pile has grown following its August acquisition of rival Assura. But it’s weathered similar challenges before and should get this under control over time, helped by asset sales and cost cutting.

In the meantime, investors can likely expect further large and growing dividends, supported by REIT rules on shareholder payouts. These state at least 90% of annual rental profits must be paid out.