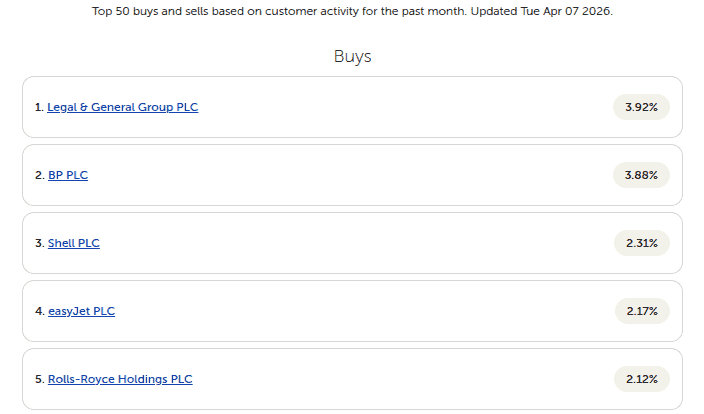

Legal and General (LSE: LGEN) remains one of the UK’s favourite FTSE 100 income picks, topping AJ Bell‘s most bought list for another month.

Making up 3.92% of buys, the shares narrowly edged ahead of BP‘s 3.88% and were almost twice that of Rolls-Royce.

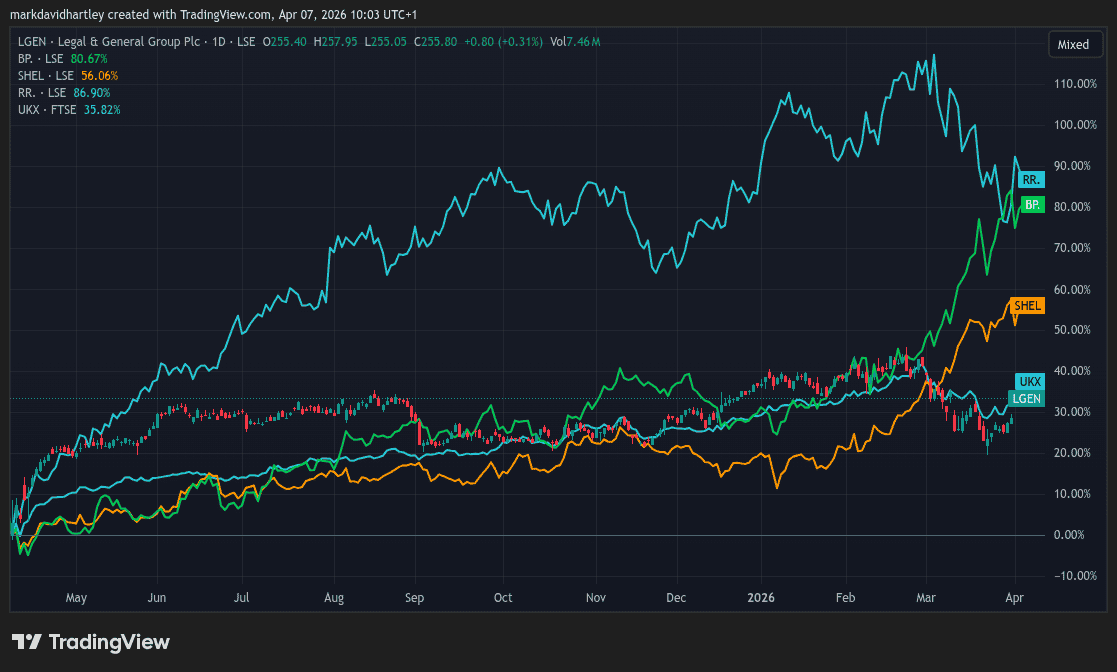

But looking at the past year’s performance, some investors may be wondering why.

Even with dividends included, the stock has barely achieved a 35% total return — less than Rolls, BP, Shell, and even the overall FTSE 100.

So why does the company continue to command such a strong following?

A household name

Part of the answer is simple familiarity. L&G has been around since the 1830s and is a household name in pensions, annuities, and life insurance. Many UK savers already see its logo on workplace pensions or annuity paperwork, so buying the shares can feel like sticking with what they know.

Aside from AJ Bell, it regularly features near the top of many ‘most‑bought’ lists. Analysts often highlight the ‘irresistible’ income appeal of its consistently high yield. That kind of constant visibility helps keep it front‑of‑mind for retail investors.

The dividend story

Dividends are the real attraction. L&G’s forward yield is about 8.5%, the very highest in the FTSE 100 and far above the index’s roughly 3% average. So for every £1,000 invested, shareholders get a bonus £85 a year just for holding the shares.

Compared to BP’s 70% price gain in the past year, that may seem a little weak. But with a 42-year track record of payments, those regular dividends are far more reliable than a one-off rally.

The payout has also grown steadily in recent years. The board has guided to 5% dividend growth for 2024 and then 2% a year from 2025 to 2027 (on top of share buybacks). For investors who want rising income in retirement, that combination of high starting yield plus modest growth is very appealing.

But is it sustainable?

Looking closer

L&G’s latest full‑year numbers showed core operating profit up about 6% and earnings per share (EPS) up 9%, with plans for a £1.2bn buyback – the largest in the group’s history.

Its Solvency II capital ratio — a key regulator‑defined strength measure — sits around 210%, giving management room to keep paying and growing the dividend if things go to plan.

Valuation is a bit trickier to unpack. Its trailing price‑to‑earnings (P/E) ratio looks high because reported profits have been distorted by market movements. But on forward estimates, the shares trade on a much lower multiple (around 11 times earnings), which is more in line with a mature but solid financial stock.

So, is it still worth a look?

Popular or not, Legal & General is by no means a risk-free stock. The fact that dividends account for so much of earnings is worrying: any small profit slip could derail payments, or hammer debt.

And considering how closely tied it is to global markets, that’s a real risk right now.

Still, it remains a compelling candidate in my book, albeit as part of a diversified portfolio rather than a single holding. Standard Life and M&G are two alternatives to consider – less established and more risky, but with a potentially higher reward.

And for the more risk-averse, I’ve also had my eye on several defensive shares lately…