UK share investors are currently spoilt for choice when searching for passive income stocks to buy. Following recent stock market volatility, a lot of quality stocks are trading at rock-bottom prices, lifting their yields to sky-high levels.

Standard Life‘s (LSE:SDLF) one dividend hero I think has been oversold in the panic. Down 5% over the last month, a £5,000 investment here today will give buyers 709 shares. With an 8.1% dividend yield, it means share pickers could make a £405 second income this year alone if broker predictions are accurate.

And if I’m right, I think it could be an excellent dividend payer for years to come.

Giant dividend yields

It’s important to remember when investing for income that dividends are never, ever guaranteed. In the current climate, with interest rates rising following the Iran war and economic growth cooling, stock investors need to take particular care.

However, Standard Life has a strong track record of paying large dividends, even during tough times. In fact, they’ve kept rising over the last decade despite challenges like Brexit, the pandemic and soaring interest rates.

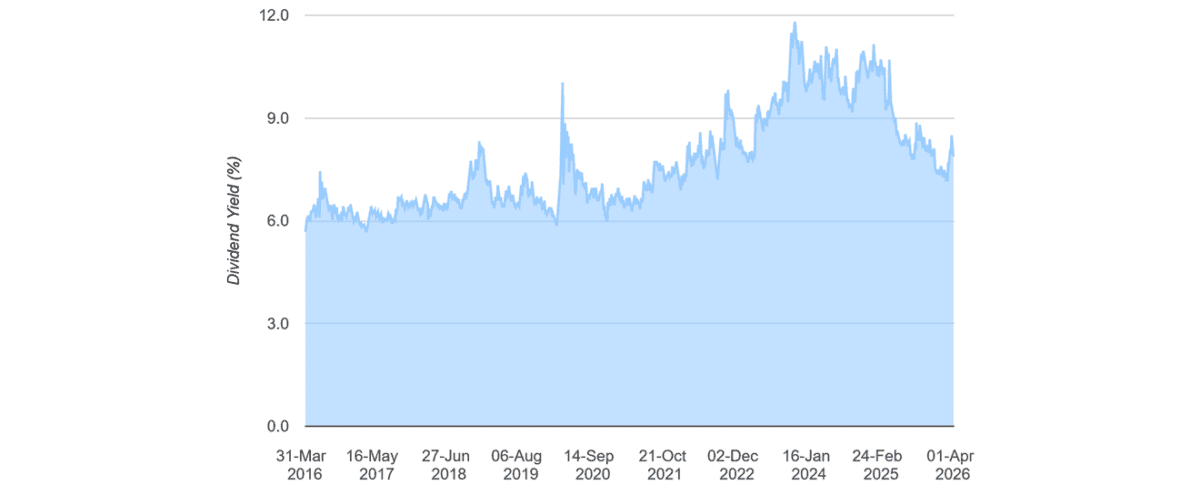

What’s more, those enormous dividend yields it offers today are no one-off. This has averaged 7.8% since April 2016, blowing the long-term FTSE 100 average of 3%-4% out of the water.

This fills me with confidence though, as I say, dividends are never nailed on.

Good omens

In this case, it’s important to stress that dividend cover falls woefully short for this year. A reading of two times or above generally provides a comfortable margin of safety in the event of earnings being blown off course.

With Standard Life, this year’s predicted dividend is 57.1p per share, and expected earnings at 73.3p. That leaves cover of 1.3 times. So for investors seeking no drama and predictable passive income, the company should be off limits, right?

The answer in my book is ‘no, not at all’. Weak (and even negative) dividend cover is a long-running theme with this particular stock. Yet a strong balance sheet has enabled it to keep offering enormous and growing yields.

Standard Life’s a cash machine, simply put. It receives a steady stream of product fees and investment returns, while its operations involve low capital intensity. So it still maintains that capital-rich balance sheet today. Its Solvency II ratio was 176% as of December, miles above the required 100%.

A growing passive income

It’s possible that the company’s balance sheet could weaken in 2026 if the war in Iran rolls on. The impact on consumer spending could put a dent in consumer demand for discretionary products, harming cash flows.

I’m optimistic that it will remain resilient in the face of these pressures as it’s been in the past. And so are City analysts — they’re tipping dividends to keep growing through to 2027, nudging the yield from 8.1% this year to 8.4% next year. It’s worth considering.