Diageo (LSE:DGE) shares crashed in the FTSE 100 this week after H1 FY26 results. Looking at the reaction, and given it was already down 50% in four years, you would assume that this stock is doomed.

However, reading through the interim report, I see five reasons why a strong turnaround is still possible in future.

Kitchen-sinking is done

‘Kitchen-sinking’ is when new management comes in and gets the bad news out of the way at once. New CEO Dave Lewis previously did it at Tesco, earning him the nickname ‘Drastic Dave’.

The idea is to clear the decks, as it were, rather than let a drip-drip of bad news seep out over time. It normally results in an immediate negative reaction, and boy, did we get that with Diageo this week when it cratered 14%.

So, what did Lewis say? It wasn’t Tesco-level kitchen-sinking by any stretch, but the biggest announcement was a 50% cut in the dividend. Diageo’s reputation for reliable dividends is over.

However, with that out of the way, the rebased payment will create more “financial flexibility” moving forward. In other words, the short-term pain will be worth it in the end, says management.

Unmet Guinness demand opportunity

As some Guinness drinkers found out over Christmas, Diageo has sometimes struggled to keep up with surging demand.

Lewis said: “The idea that we can’t service the demand that’s there is both a source of significant regret but it’s also an opportunity.”

In H1, Guinness sales grew 15% in North America.

Mass-market growth

Lewis has stated that Diageo has an opportunity in the mass-market spirits segment, where it’s significantly under-represented at a time when drinkers are cash-strapped.

Specifically, Diageo is targeting growth in ready-to-drinks (RTDs), which is things like canned cocktails. Here, it’s gaining share with Casamigos Margaritas and Smirnoff Sunny Days.

These are popular with younger drinkers who favour moderation over the neat stuff. Diageo essentially created this category 26 years ago with Smirnoff Ice.

The trade-off here, though, could be some margin pressure, which adds a degree of risk.

Pockets of growth

One reassuring thing is that a good chunk of the business is still very strong. For example, Johnnie Walker grew by double digits in Turkey in H1, while sales at Diageo Beer Company rose approximately 7% in the US. Smirnoff is doing well.

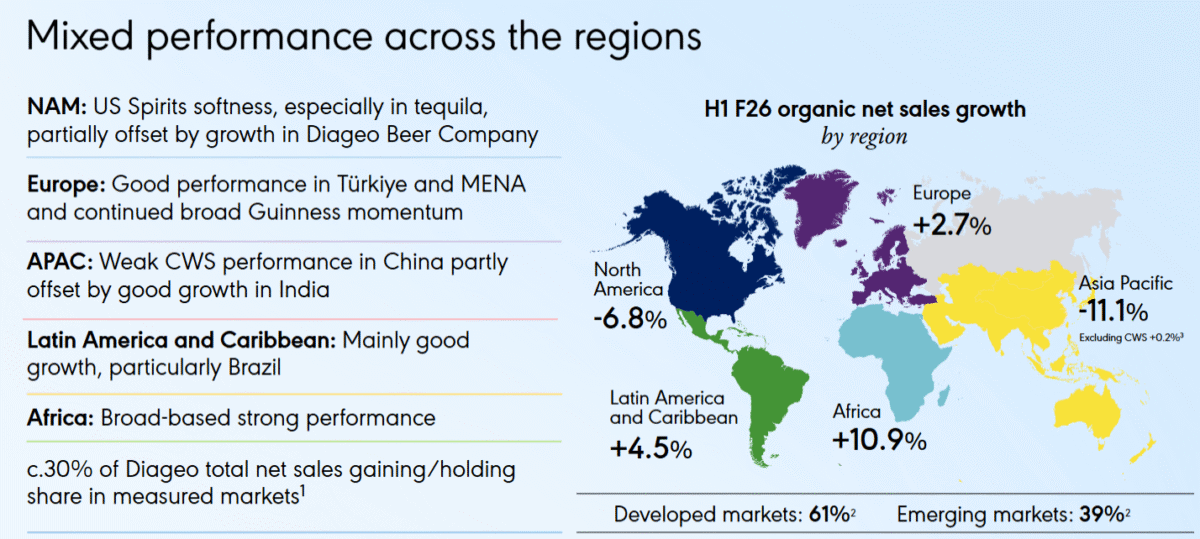

However, Chinese white spirits continues to struggle. But if we excluded this category, organic sales would have been up slightly in Asia Pacific in H1. Guinness is the powerhouse, as mentioned, but tequila fell 23%, driven by Casamigos and Don Julio.

In Latin America, Mexico and Brazil grew, despite the impact of counterfeit alcohol incidents in the latter. There was broad-based net sales growth across Africa, particularly in South Africa. But the US and China are problematic. So a real mixed bag.

Stepping back though, there are clearly enough bright spots within certain categories, brands, and markets here. Diageo should be able to lean into these strengths through targeted marketing and reprioritisation.

Stronger balance sheet

Finally, Diageo has assets to sell to improve the balance sheet, including an Indian cricket team and Chinese white spirits.

Combine this with the other points highlighted above, I think a strong future turnaround is possible, making the stock worth considering. But patience is needed.