A SIPP (Self-Invested Personal Pension) might sound like something only seasoned investors think about. But that should not be the case. It’s for everyone and it may help people stop worrying about their retirement plans.

Building a £1m pension is often less about earning a huge salary and more about starting early, contributing regularly, and staying invested through market cycles.

Even modest monthly contributions can grow substantially over time thanks to compounding. Returns generate gains, those gains produce further returns, and the effect builds momentum over decades. Add tax relief on contributions and the long-term benefits become even more compelling.

Of course, consistency is key. Markets rise and fall, sometimes sharply, but long-term growth has historically rewarded those who remain patient. Missing just a handful of strong recovery periods can significantly reduce overall returns.

However, for many people, the real breakthrough comes from simply getting started and increasing contributions gradually as earnings grow. Over time, steady habits often make the biggest difference.

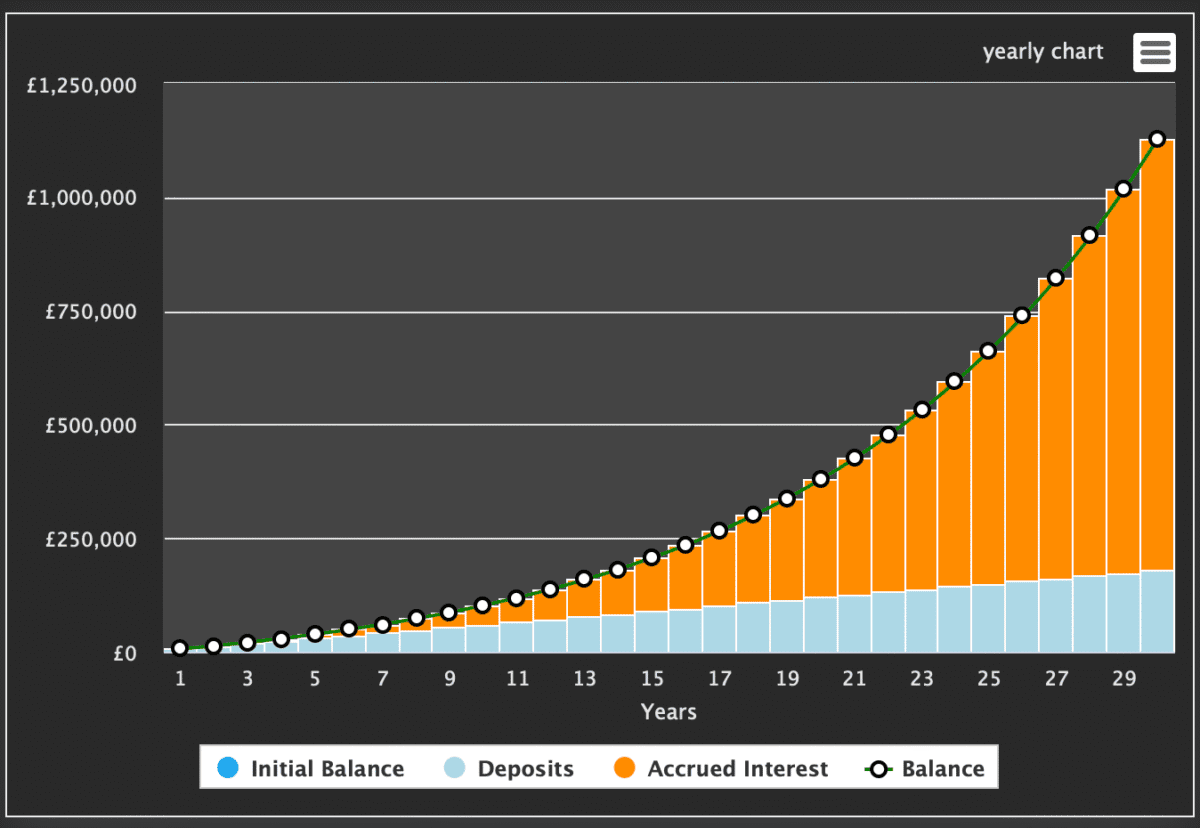

Compounding to glory

The great thing about a SIPP is that, if started early enough, there’s plenty of time for compounding. The below shows what would happen if someone placed £500 per month into a SIPP (including the state tax relief) and saw annualised growth of 10% a year — that might sound hefty but it’s just above the average ISA return in recent years.

As we can see, the £1m mark is passed in 29 years!

State tax relief is a big part of the equation too. To net £500 in monthly contributions you’d only need to add £400 yourself. The rest would come from tax relief — major investment platforms source this automatically. Higher-rate tax payers can receive more.

Please note that tax treatment depends on the individual circumstances of each client and may be subject to change in future. The content in this article is provided for information purposes only. It is not intended to be, neither does it constitute, any form of tax advice. Readers are responsible for carrying out their own due diligence and for obtaining professional advice before making any investment decisions.

Where to invest?

The big question is where to invest. If taking a passive approach (not buying and selling investments every month), then an investment trust might be a good idea.

One option I regularly tout is Scottish Mortgage Investment Trust (LSE:SMT). The investment trust has a great record of picking the next big winners.

Its portfolio includes high-growth names such as Space Exploration Technologies, Taiwan Semiconductor Manufacturing Company, Amazon, and Nvidia — companies shaping major technological trends.

SpaceX is now 15.1% of the portfolio and this figure could rise as its private market valuation surges. I do see this as being a major driver for the trust over the next year and beyond. I believe the largest company in the world in 2035 will be SpaceX, and I want a piece of that pie.

However, investors should understand the risks. The trust uses leverage (borrowed money) to enhance returns, which may magnify losses when markets fall. Its focus on fast-growing firms can also make performance more volatile than the broader market over shorter periods.

Personally, I believe it’s absolutely worth considering. It’s one of the few parts of my portfolio I don’t feel the need to check regularly.