Agronomics (LSE:ANIC) is a penny stock that has done well in the past year. Currently at 6p, it’s up around 50% over this period.

That’s better than many well-known UK stocks like Tesco (up 16%) and Greggs (down 23%).

But why am I comparing an obscure penny share with household names like Tesco and Greggs?

Food production innovation

It’s down to food, basically. Agronomics is a venture capital company with stakes in start-ups in the nascent cellular agriculture space. This technology can create meat and products like eggs and dairy directly from animal cells. It’s like brewing food, not farming it.

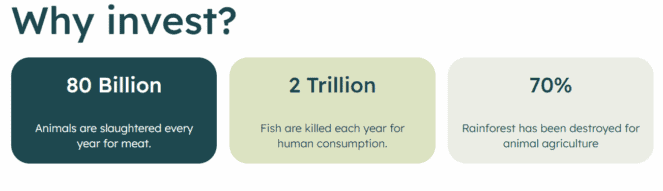

But what’s wrong with modern agriculture? Agronomics says its “dependence on complex, fragile supply chains leave the system exposed to geopolitical tensions, zoonotic diseases, and climate change, resulting in widespread instability and inefficiency“.

For example, wheat prices jumped by 40% in 2022, according to the firm. And in the 12 months to December 2024, retail egg prices surged by 65%. I know I’m paying a lot more now for a carton of eggs (when they’re even available).

Instead of raising and slaughtering livestock, cell culture technology makes it possible to grow meat quickly and cleanly, without needing imports. Agronomics is invested in firms making cell-cultivated beef, pork, chicken, and seafood, as well as one building commercial-scale fermentation facilities (where programmed microorganisms produce specific proteins).

Agronomics estimates that the cultivated meat market will see a compound annual growth rate (CAGR) of 16.5% by 2030, reaching $2.6bn. However, the precision fermentation could grow even more rapidly, reaching $34.2bn by 2031, representing a 40% CAGR.

Meaty write-off

Now, it’s very important to recognise that this is a high-risk penny stock. Not only is this technology still in the early stages of commercialisation, but there’s no guarantee that Agronomics has backed the right horses.

We saw evidence of this risk in an update from the company yesterday (9 February). It has written off its entire investment in Meatable, a Dutch cultivated meat start-up that failed to secure more funding. This stake was previously carried at a valuation of £11.9m.

There were also unrealised fair value losses on other holdings, including Solar Foods (£1.2m) and Bond Pets (loss of £0.7m). As a result, Agronomics’ calculated net asset value (NAV) per share at the end of 2025 was 13.78p, down 5.9% from 30 September.

The firm’s market cap today is £68m. This indicates that the company is trading at roughly a 54% discount to NAV (including £2.1m in cash).

Jim Mellon, Executive Chair of Agronomics, commented: “The fourth quarter of the year was a reminder that progress in clean food does not move in a straight line. While parts of the sector continue to face real pressure, we also saw evidence that the companies best positioned to scale are beginning to separate themselves.“

Challenging conditions

One share currently costs 6.3p. So a £1k investment would buy about 15,900 shares, ignoring trading commissions.

Personally, I wouldn’t invest a grand here because Mellon describes current market conditions as “challenging“. Perhaps more portfolio holdings will go bust?

While the 12-month performance has been good, Agronomics is down 65% over five years. Far worse than Tesco and Greggs.

Therefore, adventurous investors should know what they’re getting into when they consider this high-risk, high-reward penny stock.