By lunchtime today (6 January), the JD Sports Fashion (LSE:JD.) share price was nearly 7% lower after the Bank of America downgraded the stock. In November, Shore Capital was also downbeat about the retailer’s shares. It said the group’s third quarter (the 13 weeks to 1 November 2025) trading update “underscored the depth of the current trading headwinds“.

Admittedly, the retailer’s latest press release wasn’t very positive. The group said pre-tax profits would be at the lower end of the consensus of estimates (£853m-£888m). And, worryingly, compared to a year earlier, like-for-like (LFL) sales were down 1.7%, with Asia-Pacific being the only region to grow.

Shore Capital was concerned that the group was unable to pass on rising labour and operating costs to customers due to a falling top line.

However, despite this apparent doom and gloom, I remain optimistic about the prospects for JD Sports. Here’s why.

Cheap as chips

At the moment, I reckon the group’s shares are attractively priced. In fact, they look to be in bargain territory.

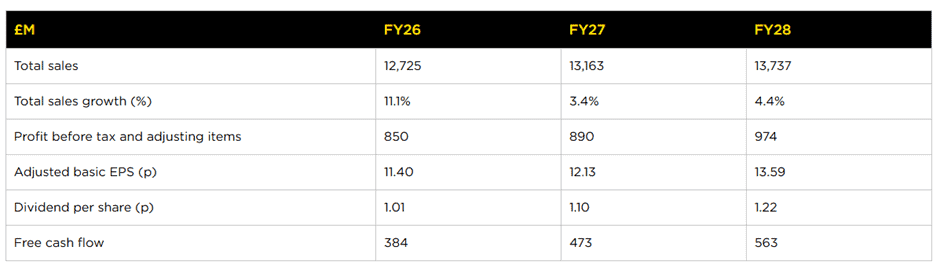

Analysts are expecting adjusted basic earnings per share of 11.4p for its current financial year ending in February 2026 (FY26). This means the stock trades on just 7.3 times expected earnings. Looking ahead to FY28, the multiple drops to 6.1. This is incredibly cheap for any business, especially one that’s on the FTSE 100.

And with relatively little borrowing on its balance sheet – it reported net debt (excluding leases) of £125m at 2 August 2025 — it remains impressively cash generative. This is important because it gives it the headroom to spend more on either revamping existing stores or buying additional ones. Alternatively, it could return further cash to shareholders.

Overseas focus

Following a major acquisition in 2024, North America’s now the group’s biggest market. I reckon this is significant because, unlike in Europe, the US economy appears to be growing rapidly at the moment.

I’m sure this summer’s FIFA World Cup in the region will also help boost sales. But it’s also a reminder of how the group’s share price has struggled in recent years. Since the last competition in Qatar in December 2022, it’s fallen by around 30%.

Importantly, although Nike, the struggling US sportswear giant, is believed to account for around half of the group’s sales, JD Sports is brand-agnostic. The British retailer has a reputation for responding rapidly to changing consumer trends. A look at its website shows 108 different brands/manufacturers listed.

Final thoughts

I acknowledge that JD Sports appears to have fallen out of favour at the moment. The group’s revenue is growing because it’s expanding both organically and through acquisition, and not by boosting LFL sales. To regain investor confidence, I think it’s going to have to address this concern.

But the problems facing the group appear to be sector-wide rather than anything specific to JD Sports. Indeed, the company itself retains a strong brand and a solid balance sheet. I suspect the current downturn in the historically resilient athleisure/sports market is a temporary blip.

Shareholders have probably marked 21 January on their calendars. That’s when the company’s due to give its next trading update, which will include crucial Christmas period sales. Of course, it could announce more bad news. However, for the reasons outlined above, I reckon JD Sports is a stock to consider.