Defence stocks have recorded stunning share price gains since Russia’s invasion of Ukraine almost four years ago. BAE Systems’ (LSE:BA.) share price is up a whopping 200% since then. And it’s showing no signs of slowing.

At £18.04 per share, the FTSE 100 weapons builder has risen 56% so far in 2025. If City brokers are correct, BAE shares will continue to soar during the next year.

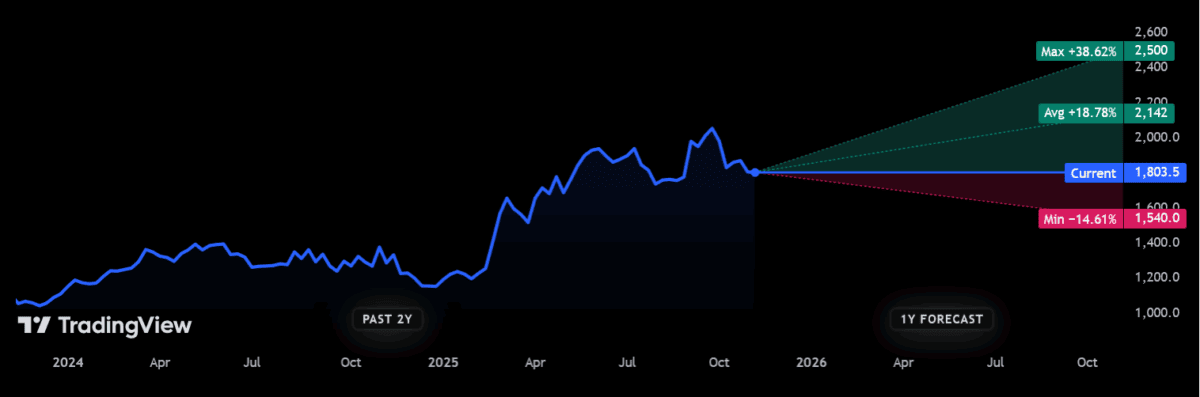

£21 target

Today, 12 analysts have ratings on the defence giant, providing a good range of opinions. The consensus among them is that its shares will rise by double-digit percentages over the next year:

The 12-month price target on BAE shares is £21.42, representing an 18.8% premium from current levels. If broker estimates for dividends are also accurate, investors can expect a total return a shade below 21% over the next year.

But of course share price and dividend forecasts are never guaranteed. As you can also see from the graph, there are also some significantly different viewpoints from City analysts concerning BAE’s share price.

Can the company really hit the heights that brokers anticipate?

Strong numbers

If fresh trading news on Wednesday (12 November) is any guide, the answer could well be yes.

BAE said that it continues to enjoy “positive momentum in order intake,” racking up £27bn worth of contracts in the year to date. It commented that further agreements are anticipated before the end of 2025.

The weapons maker added that “our order backlog, pipeline of work on incumbent positions and expanding opportunities for new work provide good visibility for long-term growth“.

The company said it’s on course to hit its full-year targets that were upgraded in July. The business has tipped sales growth of 8%-10%, and underlying EBIT growth of 9%-11%.

Great reception

BAE’s update — perhaps unsurprisingly — drew positive reactions from City brokers.

Garry White, analyst at Charles Stanley, said BAE’s update “reinforced its status as one of the FTSE 100’s standout performers, with strong revenue growth and a bulging order book underscoring the global surge in defence spending.”

He noted that “BAE’s challenge is not demand, it is delivery [while] management needs to keep costs under control and deliver on time.”

Yet White added that, despite these execution risks, the company’s third-quarter update “reinforces the positive investment case surrounding its shares.”

Is BAE a buy?

BAE’s update underlines the strong momentum the defence share continues to experience going into 2026. As White describes, supply chain and cost issues remain problems it needs to keep a tight leish on. The company also faces significant competition on contracts, particularly from US peers.

But on balance, I believe BAE looks in great shape to record further price gains, making it worth serious consideration.

As a critical supplier to armed forces in the West, it’s in the box seat to enjoy sustained demand growth through the next decade. NATO members have pledged to steadily raise core defence spending to 3.5% of their GDPs by 2035, up from 2% today. This suggests hundreds of billions more pounds flooding into the industry.

BAE’s share price looks expensive by historical standards. The firm’s forward price-to-earnings (P/E) ratio is now 24.1 times, above the 10-year average of 14 times. However, I think this rating fairly reflects the FTSE firm’s generational earnings opportunities right now.