The BT (LSE:BT-A) share price has risen an impressive 26% in the year to date. At 184.8p per share, its rise has eclipsed that of the broader FTSE 100, which is up 16%.

However, BT’s rally has hit a stumbling block more recently, its shares dropping by double-digit percentages over the last month. What can we expect the Footsie company to do next?

Broadly positive

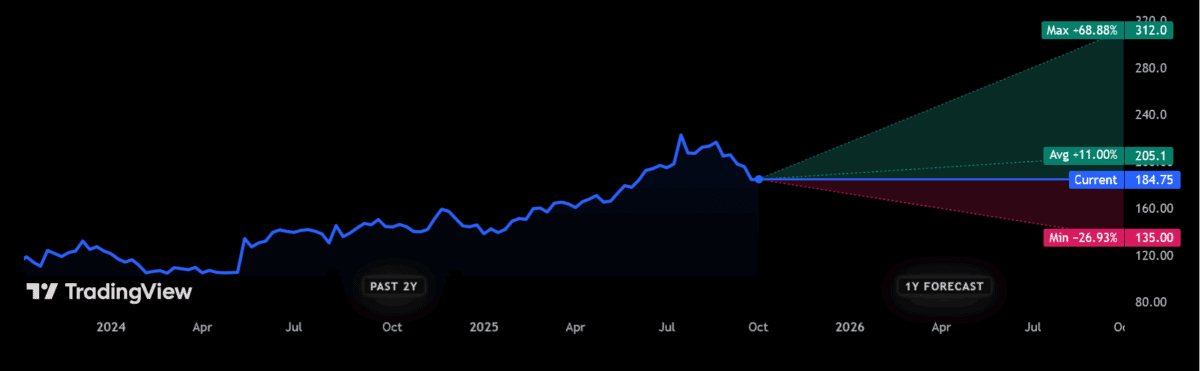

It’s largely good news for shareholders, if City analysts are a reliable guide. They think BT’s shares will continue rising strongly over the next year.

The telecoms titan has a 12-month price target of 205.1p per share, representing an 11% increase from current levels.

That’s lower than the 27% share price rise it’s enjoyed during the past year. But it suggests investors today could still enjoy a tasty return of around 15%.

This factors in the FTSE company’s forward dividend yields of 4.6% and 4.8% for financial 2026 and 2027 respectively.

Yet there are a couple of important things to remember. The first is that share price projections often miss their forecasts, to the upside as well as the downside.

Secondly, you’ll see that City experts are far from unanimous in their bullishness for BT’s share price. The most positive broker among the 18 offering ratings reckons it will rise 69% over the next year. But at the other end of the scale, BT’s tipped to slump by more than a quarter by an especially pessimistic forecaster.

The case for BT

Those bullish on BT are confident that work to streamline operations and cut costs — major drivers for the company’s recent share price jump — will continue apace.

Moving customers onto 5G and fibre broadband services from legacy plans is giving margins and cash flows a big boost. In May, chief executive Allison Kirkby announced the business had hit its “£3bn cost and service transformation programme a year ahead of schedule“.

With BT past peak capital expenditure for its fibre broadband rollout, too, the company looks in better shape than it has in recent years.

The case against BT

But are the firm’s successful self-help measures enough to justify its rising share price and deliver further gains? I’m not so sure.

Following July’s trading update, it seems the market is cooling on the idea as well. Back then, the company revealed ongoing top line pressure as it battles tough competition and a stagnating UK economy.

Adjusted revenues dropped 3% between April and June, with drops of 3% and 6% at Consumer and Business, respectively, offsetting a 1% rise at Openreach. With pressures rising, I can’t see turnover springing higher any time soon.

BT’s inability to get sales firing again is all the more worrying given its enormous net debt. This was £19.8bn as of March, up £300m year on year. While news of lower capex for broadband rollout going forwards is good news, a huge pension deficit and large day-to-day running costs still cast a shadow over the balance sheet.

This could significantly hamper the firm’s growth plans, and also raises questions over future dividends.

What next?

It’s possible that the BT share price will continue rising over the next 12 months. But I think the risks to investors in the short-term and beyond are severe. Personally, I’m looking for other UK shares to buy.