It sounds implausible. A £27m Self-Invested Personal Pension (SIPP) from just a few thousand pounds a year. But with a long enough runway and the power of compounding, it becomes a mathematical possibility.

A SIPP opened at birth and topped up consistently could, in theory, accumulate a fortune over time. Using HMRC’s maximum child SIPP contribution of £3,600 a year (including tax relief), the numbers stack up compellingly if invested wisely from day one.

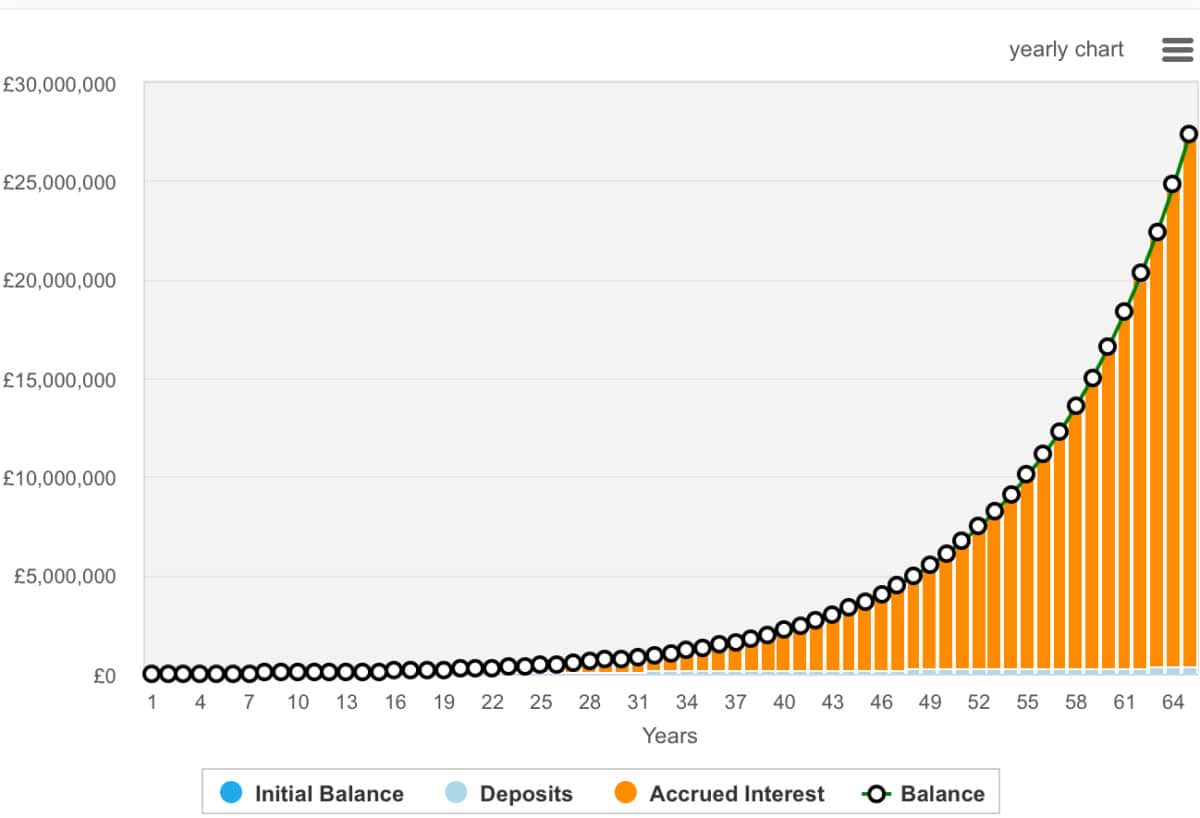

Assuming an average annual return of 10% — reflective of US market returns over the past decade — the balance grows modestly at first. By age 10, the pot might stand around £68,000. But the compounding effect gathers pace. By 25, it could top £450,000. By 40, it may pass £2m.

Keep going, and at age 65 — without increasing contributions beyond inflation — the balance could exceed £27m. The secret? Time, tax relief, and long-term exposure to growth assets like equities. This calculation also includes a 1% increase in annual contributions each year to account for potentially larger contributions in the future.

Of course, future returns aren’t guaranteed, and inflation would eat into purchasing power. UK investors may also earn more modest returns with UK-focused investments and poor investment decisions can see us lose money. But even under more conservative assumptions, a child’s SIPP could become a meaningful financial asset later in life.

Parents, grandparents, or guardians funding early SIPP contributions could give a child an extraordinary head start. And it’s not just financial, but contributes to an understanding the value of investing early and often. This calculation also involves the child going on to make contributions themselves as they start working. It requires a long-term commitment.

It’s not the flashiest strategy. It doesn’t have to involve hefty bets on tech disrupters or shorting overvalued stocks. It’s simply about starting early and letting compound returns do the heavy lifting.

Where to invest?

Anyone opening a SIPP for a child or loved one has several options when it comes to investing. A simple, hands-off approach might involve low-cost index-tracking funds or investment trusts. These offer instant diversification and a long-term growth orientation, making them ideal for compounding over decades.

Alternatively, more active investors might prefer to build a portfolio one or two stocks at a time. One company I’m watching closely right now is Synectics (LSE:SNX). It’s an AIM-listed specialist in advanced security and surveillance systems.

At just over £53m in market-cap, Synectics trades on just 12.2 times forward earnings, falling to 9.5 times by 2027. Adjusting for its net cash position of £12.1m, that gives a price-to-earnings-to-growth (PEG) ratio of 0.72. This implies the shares could be significantly undervalued based on growth forecasts.

Recent interim results showed revenue up 35%, operating profit up 48%, and earnings per share up 59%. Its growing order book, international expansion, and debt-free balance sheet are all really positive feature.

Of course, as a small-cap, it carries more risks. This including contract concentration and macroeconomic sensitivity as well as a large spread between buying and selling prices. But for long-term investors, Synectics might be worth a closer look. I’ve added it to my watchlist.