For my money, the best way to source a long-term second income is to invest in dividend-paying assets. I own a variety of stocks, investment trusts and exchange-traded funds (ETFs) that have a history of paying a large and growing income over time.

Here are two that have caught my attention this month. I’ll consider adding them to my Stocks and Shares ISA when I next have spare cash to invest.

Growth and income potential

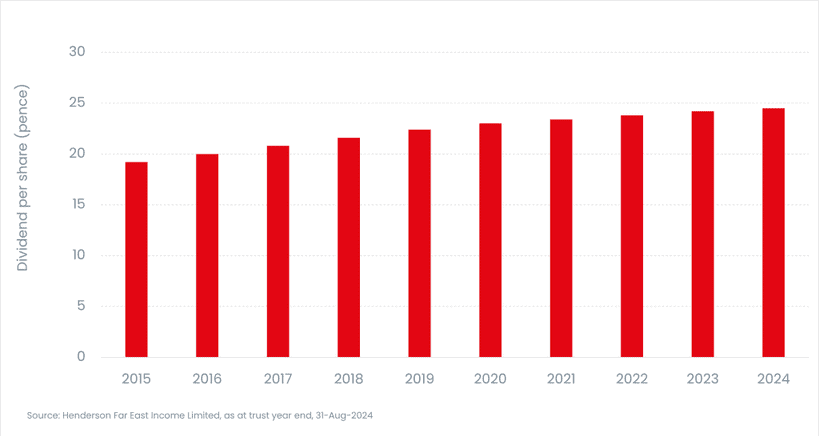

At 11%, Henderson Far East Income (LSE:HFEL) has one of the highest forward dividend yields on the London stock market. This reflects in large part significant share price weakness in recent years that’s inflated the yield.

As its name implies, it provides significant exposure to China and the surrounding regions. Around 27% of its capital is tied up in Chinese equities alone. So amid signs of severe economic cooling there, it’s no shock to see it fall in value.

The trust’s regained much ground in 2025, thanks to signs of improvement in China’s economy. Yet with trade tensions simmering, it’s possible the share price could turn lower again.

However, I still think Henderson Far East Income is an attractive trust to consider. Its investment across a spectrum of Asian powerhouse economies (including Hong Kong, India and South Korea) provides abundant opportunities for shareholders to tap into. With continental wealth levels and population sizes booming, I think it provides excellent growth and income potential.

The make-up of its portfolio also allows it to weather individual dividend shocks and pay a large and growing dividend. As well as providing excellent geographical diversification, the 70-plus companies it holds are spread across multiple sectors including financial services, consumer goods, real estate and technology.

As you can see, annual dividends have kept steadily rising, even in spite of troubles in the key Chinese market. In fact, they’ve grown for 17 years on the bounce.

Another top trust

TR Property Investment Trust (LSE:TRY) doesn’t have such a knockout near-term dividend yield. For 2025, it sits at a still-market-beating (but not double-digit) figure of 5%.

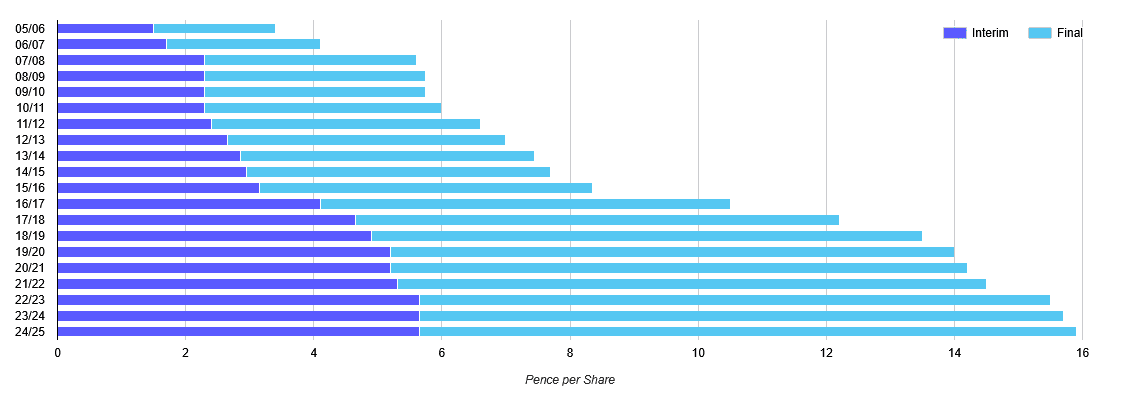

What it does have however, is a similarly excellent record of unbroken dividend growth. Shareholder rewards have risen almost each year for around 20 years.

TR invests in real estate investment trusts (REITs) across Europe, including the UK. This makes it a reliable source of income as, under sector rules, these trusts must pay at least 90% of annual rental earnings out in dividends. That’s in exchange for the tax breaks they receive.

Many of these trusts focus on cyclical sectors like retail, leisure and industrials. And so rental collection and building occupancy are highly sensitive to economic conditions.

But strong diversification across sectors helps limit such damage on overall returns. Healthcare, residential and food retail are also among the industries it has exposure to through the 48 REITs it holds.

Today, the trust trades an a near-8% discount to its net asset value (NAV) per share of 352p. Combined with that large dividend yield, I think it’s a great value investment trust to consider.