Analyst price targets for Lloyds Banking Group (LSE:LLOY) shares aren’t especially ambitious at the moment. But there are some clear ways things could turn out better than expected.

Interest rates, an ongoing legal case (yes, really), and a healthy dividend are all positive signs for the bank. So is there a buying opportunity for investors?

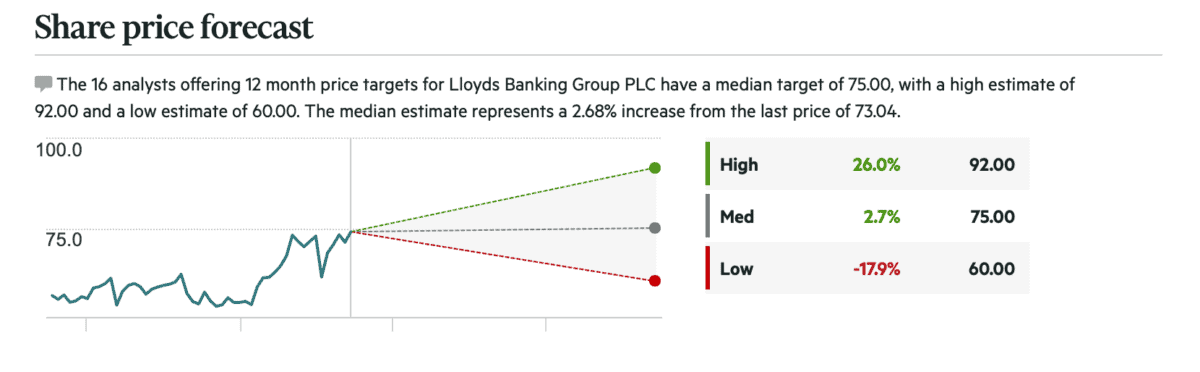

Price targets

It’s fair to say analysts are pretty divided on the outlook for Lloyds Banking Group shares. The median price target is 75p – about 3% higher than the level the stock currently trades at.

Source: Financial Times

There is, however, quite a big range. The highest estimate is 26% higher than the current share price and the lowest implies a drop of 18%.

Investors should note, though, that the dividend yield is around 4.5%. If that continues, it could provide a return in line with a 10-year government bond even if the stock goes nowhere.

The company also has an ongoing share buyback programme, which should help boost the value of the stock. And I think there are more reasons for optimism going forward.

Interest rates

I always see it as a bit of risk when a company’s profitability depends on something beyond its control. And that’s the case with Lloyds and what the Bank of England does with interest rates.

The UK’s central bank decided to bring rates down earlier this month and that is likely to be bad for lending margins. But I think investors have a couple of reasons for optimism.

One is that the Bank of England has indicated it intends to be cautious with future decisions. So it’s far from automatic that interest rates are going to fall further in the near future.

Another is that cuts have more impact when rates are already low – 1% to 0.75% is more significant than 3% to 2.75%. So a reduction from 4.5% to 4.25% might not be a big problem.

Motor loans

The other major ongoing issue is the legal case concerning motor loans. Lenders including – but not limited to – Lloyds are appealing the verdict from the Court of Appeal in October 2024.

A verdict is expected on this in the next few months. And this could have a big impact on the company’s share price one way or another.

Lloyds has set aside around £1.2bn to cover potential liabilities. That’s around 66% of what the company distributed in dividends in 2024.

Analysts estimate that the worst-case scenario for the bank could be liabilities of around four times this level. But if things go well, shareholders could be in line for a strong return.

A stock to consider buying?

The average analyst price target for Lloyds shares is close to the current level. But there’s a big range and this reflects a lot of uncertainty at the moment.

No company ever has total control over its profits. In the case of Lloyds, though, an unusually large amount of its future returns comes down to things it can’t do anything about.

At the right price, that’s a risk I think investors could justifiably consider taking. But I think there are more attractive opportunities in UK stocks at the moment.